(Bloomberg Opinion) -- JPMorgan Chase & Co.’s investment bankers must be feeling a bit deflated. They just turned in all-time record quarterly revenue for advising on deals and one of the best results ever for total investment banking fees. And what do shareholders do? Sell the stock.

Truth is, this was kind of old news. JPMorgan’s investors were looking for something fresher and more upbeat on growth in lending to companies and people from the bank’s third-quarter results, which were released on Wednesday. There was no great disappointment, but the bank was probably more cautious in its outlook and expectations than many had hoped.

At first look, the third quarter more than delivered: Earnings per share were 26% ahead of expectations at $3.74. But gains came from the same sources that have driven the beats all year. JPMorgan’s shares slipped 2.5% in morning trading.

The boom in investment banking and trading held up better than expected in many areas, partly because JPMorgan took share from rivals, Chief Financial Officer Jeremy Barnum said. Also, there was an additional $1.5 billion of net releases from bad-loan provisions, which were put aside in the depths of the Covid-19 pandemic last year.

Billions of dollars in provisions are still to be released assuming the recovery continues — but that is just delayed booking of profits from previous years, plus the pace of releases is slowing. The mergers and acquisitions boom should continue awhile, too, but management recognizes investment banking and trading will normalize over the rest of this year and next.

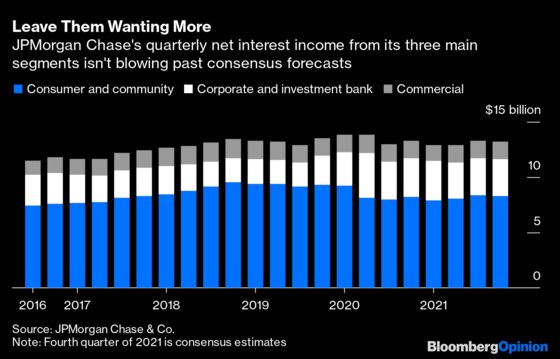

What matters is the core of banking: The income generated from the difference between funding costs and the interest generated on loans and securities held on the balance sheet. For the bank as a whole, this net interest income came in very close to but marginally below consensus forecasts. That was enough for some optimism but nothing over the top, as Alison Williams of Bloomberg Intelligence, put it.

There are a couple of problems. First, loan growth just isn’t truly picking up yet. In the consumer and community bank, total loans shrank 2% compared with those in the third quarter last year; they were down 5% in the commercial bank.

Both are being hurt by all the cash that has been pumped into the economy to get companies and consumers through the restrictions of lockdowns. Barnum said credit-card balances should begin to grow, but he expects it will be some time before they return to pre-Covid levels.

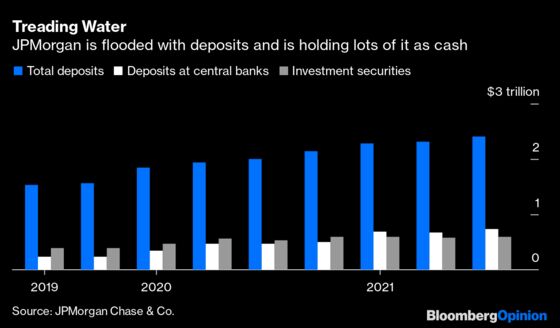

Second, JPMorgan is also being extremely conservative with the huge flood of deposits it has attracted during the pandemic. Total deposits placed with the bank have grown by $840 billion since the end of 2019 to $2.4 trillion at the end of the third quarter.

JPMorgan has put nearly $500 billion of that increase straight into deposits at central banks, which keeps them safe and accessible but means it’s earning next to no income on them. Only $197 billion extra has gone into increased holdings of investment securities.

Barnum said the bank is still wary of losing money in a volatile Treasury market threatened by inflation. On the analyst call, Barnum and Chief Executive Officer Jamie Dimon were pressed on how much of the excess cash deposits could be put into securities when yields reach a higher and more stable level. Dimon made a quick, vocal bid: “$200 billion!” he said. But Barnum swiftly returned to a theme of caution, saying that many factors were at play and decisions on where to put liquidity were always tactical and “highly situational.”

On the positive side and for the longer term, the bank could boost interest income by switching its preference away from the safety and unquestionable liquidity of central bank reserves and favoring more Treasury holdings instead. There are, however, regulatory issues to do with leverage ratios and liquidity requirements to consider as well as the volatility and value of U.S. Treasuries.

Barnum did suggest that recent rises in Treasury yields meant the bank might start to move back into the market a little bit and start buying some longer-term bonds again, but overall he was happy to remain on the sidelines.

The future of net interest income for JPMorgan and its peers is going to depend mostly on what happens with inflation, interest rates and especially consumer spending. Those are out of the bank’s control. But the quicker that its investment banking and trading activity normalizes, the sooner Barnum and Dimon might have to make some less cautious decisions about what to do with its huge pool of excess cash.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2021 Bloomberg L.P.