JPMorgan Didn’t Signal a Turning Point for the Economy

(Bloomberg Opinion) -- You could almost feel the shockwave that JPMorgan Chase & Co. sent across Wall Street on Tuesday morning with its third-quarter earnings.

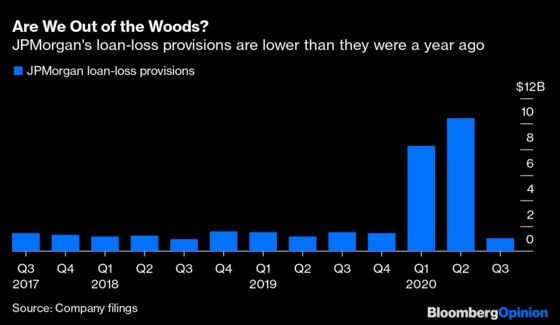

Investors have always scrutinized results from the biggest U.S. bank, which provide insights into all corners of the economy. But they’ve rarely been as critical as during the coronavirus crisis, which has put in stark relief the divide between small businesses and large corporations; between front-line workers and those in white-collar jobs; and between homeowners and those who rent. The message from JPMorgan until this point has been clear: We’re going to get through this but have reason to expect much more pain ahead. In July, the bank announced it had set aside a whopping $10.47 billion for credit losses, more than anyone predicted and up from $8.3 billion in the first quarter.

Analysts predicted that JPMorgan would earmark another $2.4 billion for potentially bad loans in the three months through September, a period defined by gridlock among Washington lawmakers over another round of fiscal aid as the Covid-19 pandemic flared up across the U.S.

Instead, it set aside just $611 million.

That figure is stunning. Not only was it far below analysts’ expectations, but it was down $903 million from a year earlier. The low provisions for credit losses make it seem “as if Covid-19 never happened,” said Octavio Marenzi, chief executive officer of consulting firm Opimas, and “strongly suggested that JPMorgan Chase had overestimated the impact of the epidemic on credit losses.” And JPMorgan doesn’t look like an outlier — Citigroup Inc. also set aside about $1.5 billion less for bad loans in the third quarter than analysts had expected.

Still, I would take a breath before declaring this an all-clear for the U.S. economy.

For one, it was obvious that JPMorgan was being somewhat conservative with its past buildup in loan-loss reserves, using record-breaking trading revenue as cover while still beating overall expectations. “If the base case happens, we may be over-reserved. I hope the base case happens,” CEO Jamie Dimon told analysts in July. In total, JPMorgan has almost $34 billion reserved for credit losses.

The bank’s base case now is for a U.S. unemployment rate of 9.5% at the end of the year and 7.3% by the end of 2021, compared with estimates of 10.9% and 7.7%, respectively, as of July, when the jobless rate was in the double digits. Considering that the unemployment rate fell to 7.9% in September, JPMorgan is either being overly cautious yet again or expects the labor market gains to slow, if not reverse.

Chief Financial Officer Jennifer Piepszak addressed this tension multiple times during the bank’s conference calls. The reserve releases that contributed to lower-than-expected provisions for bad loans shouldn’t be seen as a sea change in the bank’s assumption about how the economy will perform, she said, though she indicated that JPMorgan doesn’t expect any significant increase in charge-offs until the second half of 2021. “The medium to longer term is still highly uncertain, in particular as it relates to future stimulus,” she said. “So we remain heavily weighted to our downside scenarios.”

JPMorgan, fresh off its most profitable quarter of 2020, is trying to strike a difficult balance. Clearly, there’s still pain among small businesses and unemployed workers. “There are a lot of people who are under a lot of stress and strain who won’t survive another year” of total economic lockdown, Dimon said during a call with analysts.

But this is an unprecedented year for the economy. Consider, for instance, that Americans’ incomes fell in August by the most in three months after the government’s extra unemployment benefits expired, yet combined spending on JPMorgan’s debit and credit cards in September increased year-over-year for the first time since Covid-19 shutdowns began. The bank’s total deposits have surpassed $2 trillion, up more than 30% from last year, propelling it to the top spot in U.S. retail deposits for the first time. Yet total loans rose just 1% during the same period, dropping JPMorgan’s loans-to-deposits ratio to just 49%, indicating the bank is lending less relative to its capacity to do so. More than half of consumer loans in payment deferral at the end of the second quarter have exited those plans, with about 92% of those that came out of deferral programs now current on their payments.

This all points to a much murkier path forward than JPMorgan’s initial headline figure on loan-loss provisions seemed to indicate. What happens to those consumers who remain squarely in deferral? Will the bank start extending more loans and take greater risk — and if not, what becomes of those turned away? Are people increasing credit-card spending for good reasons or because they’re using a $3 trillion buffer to make up for the lack of additional federal aid? “We’ve built significant reserves, so we’re prepared for it to be a delay rather than change the outcome” of losses, Piepszak said.

It’s probably best to avoid drawing sweeping conclusions from JPMorgan’s results. Yes, it’s fair to assume that Bank of America Corp. and Wells Fargo & Co. probably won’t set aside large sums to cover potentially souring loans when they announce third-quarter earnings on Wednesday, leaving the nation’s four biggest lenders far short of analysts’ estimates for $10 billion in additional loan-loss provisions in the third quarter. It’s an unambiguous sign that things at least aren’t getting worse for the U.S. economy as a whole.

As for whether the world’s biggest economy has reached a turning point? That remains inconclusive.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.