JPMorgan and Citi Pay Raises Leave Less for Investors

(Bloomberg Opinion) -- The great economic rebalancing between capital and labor is finally here — in banking at least.

The share prices of JPMorgan Chase & Co, Citigroup Inc. and most other U.S. banks tumbled on Friday after both banks reported higher costs for 2021 and predicted more inflation to come, most of which is being driven by higher pay.

What is more, the jump in staffing costs is kicking in just as the revenue from trading stocks and bonds is dropping from the exceptional levels of the past couple of years while the industry struggles to find growth in lending and interest income. For investors, this likely means a squeeze on returns ahead even as interest rates start to rise.

JPMorgan was first to deliver the bad news Friday, and the early reaction of its stock price was the biggest earnings day fall it has encountered in more than a decade. The bank’s stock valuation had little room for disappointment: It has been trading at nearly two times forward book value and a big premium to most rivals, so without unalloyed good news the only way was down.

It reported robust investment banking fees for the fourth quarter, up 37% compared with those in the period a year earlier, in line with the bank’s guidance. But income from trading was worse than expected, with quarterly bond and currency trading revenue down 16% year over year and stock trading revenue down 2%.

It was a similar picture at Citigroup, although the misses were bigger compared with expectations, especially for equities trading, an area in which Citi had outperformed much of the rest of Wall Street in the third quarter last year.

At the same time, net interest income — the revenue from traditional lending — was little changed. JPMorgan’s rose 2.3% over the same period last year, Citi’s was flat and interest income at Wells Fargo, which also reported Friday, was down 1.1%.

Wells Fargo was the only large bank whose stock rose, however, which underlines the focus on costs. Wells has had to focus on cost cuts in part because of the size cap that regulators imposed on it as punishment for wrongdoing in its consumer bank. It is barred from growing, and so the revenue from its balance sheet has been squeezed more than most as interest rates fell.

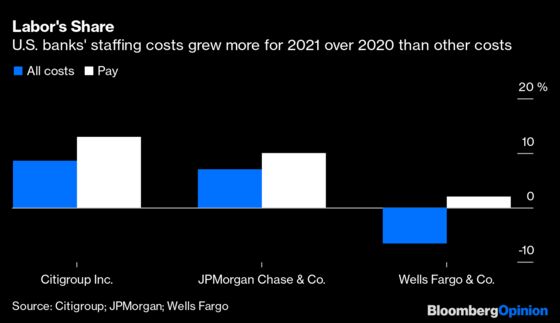

Total costs at Wells were down nearly 7% for all of 2021 compared with those in 2020, although it still spent more on people; personnel costs rose 2% for the year. But that compares with a jump in annual costs of 7% at JPMorgan and 9% at Citi. At both those banks, staff costs rose faster: They were up 10% at JPMorgan and 13% at Citi.

For both Citi and JPMorgan, those costs are likely to continue. JPMorgan Chief Executive Officer Jamie Dimon warned that the bank’s profitability would be lower than its normal potential over the next couple of years as it invests heavily in technology and people. He said different industries are now competing with banks for talent: electronic market makers, all kinds of fund managers and financial technology companies.

Investment banking and trading experienced the biggest rise in costs at JPMorgan, and pay was the biggest part of that. This suggests banks are likely to see a rise in the share of revenue going to pay bankers in the years ahead. As investment banks fight it out for the people they want, more bankers get a higher proportion of their pay guaranteed in advance. With all dealmaking and trading revenue likely to slow further from the record numbers seen at different points in the past couple of years, compensation ratios will naturally rise.

Dimon is determined to pay for good people as part of the competition against other banks and industries, a competition he unsurprisingly wants to win. Rising wages are a good thing for workers, he said; he’s not complaining. Businesses “shouldn’t be crybabies about it,” he added.

He might as well have been telling investors — the providers of capital — that they shouldn’t moan either about more of the returns from business going to labor instead of them. Although with more of those pay gains likely going to investment bankers than branch tellers, it’s probably not the kind of rebalancing between capital and labor many people would have had in mind.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2022 Bloomberg L.P.