Jobs Strength Leaves Fed and Powell With Nowhere to Hide

(Bloomberg Opinion) -- The Federal Reserve and Chair Jerome Powell have come under fire the last couple of months for seemingly ignoring the spike in inflation. The latest salvo came Thursday, when Senator Joe Manchin, the West Virginia Democrat, urged Powell to start pulling back on the Fed’s $120 billion in monthly bond purchases aimed at providing stimulus. Failing to do so “will lead to our economy overheating and to unavoidable inflation taxes that hard-working Americans cannot afford,” Manchin wrote in a letter he made public.

Measures of inflation have surged, it’s true, but Powell defended the Fed’s stance by saying he was more concerned about the more than 6 million Americans who were still out of work because of the pandemic. But as Friday’s strong jobs report showed, Powell can no longer hide behind that excuse. Expect a less dovish tone from the central bank, and for it to start tapering its bond purchases as soon as next month.

Almost every part of the employment report exceeded expectations. The economy added 943,000 jobs in July, the most since August 2020 and exceeding the 870,000 median estimate of economists surveyed by Bloomberg. Not only that: June’s numbers were revised higher, to 938,000 from the 850,000 originally reported. The unemployment rate fell to 5.4% from 5.9%. And average hourly earnings rose 4% from a year earlier, up from the pre-pandemic five-year average of 2.7%.

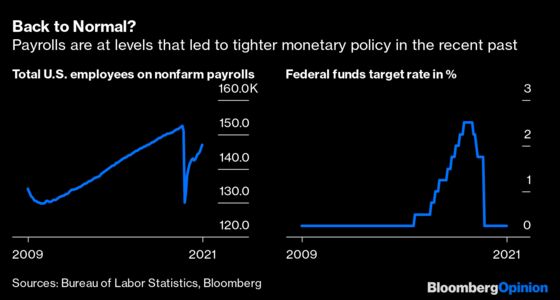

While some 5.7 million Americans remain out of work, total employment of 146.8 million is at the level it was in late 2017, when the Fed was raising interest rates. Also, the jobs numbers don’t capture the surge in the number of Americans who have decided to retire early.

The more important number may have come from the household survey, which investment bank FHN Financial says includes the self-employed and part-timers not included in the broader payroll count. Here, employment rose by a whopping 1.04 million, the most since October. Here’s how FHN Chief Economist Chris Low put it in a research note:

As Fed Chair Jay Powell predicted months ago, the looming end of federal unemployment programs would lead to millions actively seeking work. It took longer than he initially expected for the process to begin, but the big drop in benefit recipients in July foreshadowed this jobs gain. August should be another big month, and September as well as there are still millions who need to find work quickly.

The doves may say that the jobs numbers were goosed by an unusually large 220,700 seasonally adjusted gain in local education payroll, the result of the government attempting to smooth out the school-related dismissals that occur during the summer months. Bloomberg News reports that because of smaller staffing levels this spring, the adjustment resulted in a larger-than-normal July gain.

Nevertheless, the bigger point is that job gains are accelerating. The report makes the Kansas City Fed’s annual policy retreat in Jackson Hole, Wyoming later this month all the more important. This event is known for signaling big changes in monetary policy, and Powell has confirmed he will speak at the conference.

Expect Powell to make clear that the economy has made “substantial further progress” and that the Fed is ready to ease its foot off the stimulus pedal. The next gathering of the policy-making Federal Open Market Committee starts on Sept. 21, which is when the central bank will likely lay out when it will start tapering its bond purchases and by how much. It’s time.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.