Jobs Data Was ‘Perfect Miss’ for Fed and Fiscal Stimulus

(Bloomberg Opinion) -- “Perfect miss.”

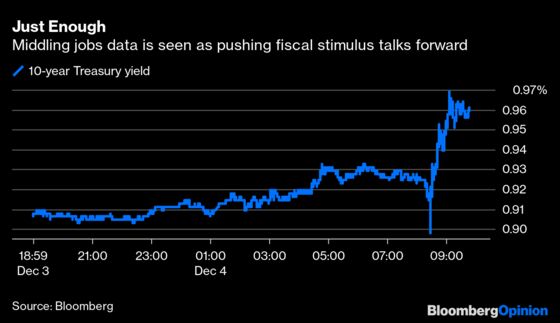

That was the first reaction to the November jobs report I saw on Twitter. And it turned out to be exactly right in the eyes of the $20.4 trillion U.S. Treasury market. The benchmark 10-year yield extended its climb, increasing 6 basis points on the session to 0.97%, breaking through to its highest level since March.

Certainly, the headline number was bad: Nonfarm payrolls increased by 245,000 in November from the previous month, missing the median estimate of a 460,000 gain in a Bloomberg survey of economists, though forecasts ranged from a 100,000 monthly decline to a 750,000 gain. Digging a bit deeper, the labor force participation rate also unexpectedly dipped to 61.5% from 61.7%, which helped drive the overall unemployment down to 6.7% from 6.9%. That’s not the way the jobless rate declines in a healthy labor market.

Yet the report wasn’t so ugly that it made investors rethink the outlook for the U.S. economy as a whole. The participation rate is “not the direction one would like to see at this stage in the recovery,” wrote Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets. “Clearly the resurgence of Covid-19 and the lockdowns are having an impact, but not such a dramatic one as to recast expectations.”

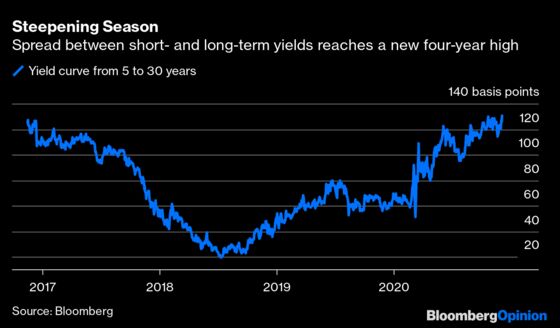

Jim Vogel at FHN Financial correctly predicted roughly 24 hours before the release that this sort of “middle” outcome would cause Treasury yields to rise the most. Indeed, on top of 10-year yields nearing 1%, the yield curve from five to 30 years steepened to 130 basis points, on pace to end the week at the highest closing level since November 2016.

Here’s how Vogel described the push-and-pull dynamics that bond traders have been feeling with regard to the Federal Reserve’s monetary policy and the potential fiscal aid coming out of Congress:

Even though a disappointing number might improve chances for stimulus next week, traders will put more weight behind the bond-positive impact on the FOMC. And, because curve steepening has largely taken the Fed out of the picture anyway, a good number does little except depress expectations for stimulus. A middle outcome will put the most pressure on interest rates, then, because payrolls will be deemed inconsequential and current negative price momentum will dominate.

On the Fed side, investors are on the fence about whether the central bank will announce on Dec. 16 that it intends to extend the weighted-average maturity of its $80 billion in monthly Treasury purchases. Just how split are they? In a survey from BMO Capital Markets asking whether the Fed will move ahead with such a policy shift this month, 56% of respondents said no, and 44% anticipate the change will be formalized. That kind of uncertainty around such a significant move is rare, especially as policy makers are about to enter their self-imposed quiet period.

This round of jobs data probably isn’t enough to tip the scales and compel them into action. “It’s unclear that they need to spend that bullet,” Jeffrey Rosenberg, senior portfolio manager at BlackRock Inc., said on Bloomberg TV after the release.

And over on Capitol Hill, it seems to be a good bet that politicians will be sensitive to headlines indicating a weaker U.S. labor market right around the holiday season and feel increased pressure to strike a deal on another round of fiscal aid. Senior Republicans are starting to get on board with the idea of using a $908 billion proposal from a bipartisan group of lawmakers as a basis for a compromise. House Speaker Nancy Pelosi and Senate Democratic leader Chuck Schumer already said they would use that same blueprint in negotiations.

Part of that proposal strikes directly at the heart of the softening jobs market: $180 billion would fund an extension of pandemic unemployment benefits, providing an additional $300-a-week for four months. White House economic adviser Larry Kudlow also called for such a measure on Friday, about an hour after the jobs report was released.

As I wrote earlier this week, Fed Chair Jerome Powell likes to think about fiscal policy as a “bridge” to get the economy through the pandemic and over to the side that includes widespread vaccinations. If this latest read of the labor market is any indication, the economy is swerving but hasn’t fallen off a cliff. It might just be enough to get Congress to act.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.