Kamala Harris Overshadows Joe Biden’s First Jobs Day

(Bloomberg Opinion) -- It took all of 15 seconds for Vice President Kamala Harris to render mostly irrelevant a data release that has long been considered one of the most important in the world.

The latest read on the U.S. labor market was disappointing, with nonfarm payrolls increasing by just 49,000 in January, falling short of the median estimate of a 105,000 gain in a Bloomberg survey of economists. The revised figure for December was even worse, with the Labor Department now saying that the world’s largest economy lost 227,000 jobs, compared with a decline of 140,000 previously. On its face, the unemployment rate looks a lot better, at 6.3% from 6.7% previously, but that’s in part because the labor force participation rate is sliding lower again.

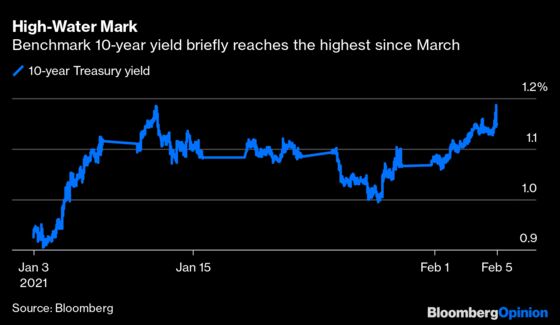

Treasuries reacted about as expected in the immediate aftermath, with benchmark 10-year yields falling from a high of 1.17% to 1.15% within 10 minutes of the report’s release. Yet they soon bounced back and breached 1.1855%, the top-tick from last month that was the highest level since March. Long bonds came within two basis points of 2%.

Why so upbeat? Well, heading into the week, it looked as if this jobs report would set the tone for fiscal stimulus talks in Washington. President Joe Biden had proposed a $1.9 trillion Covid-19 relief package, while 10 Republican senators had countered with a $600 billion plan. Biden has said from the start he hoped to reach a bipartisan agreement. In this context, it certainly seemed as if the state of the U.S. labor market could swing momentum in one direction or the other. Just about 24 hours ago, my colleague Peter Coy of Bloomberg Businessweek wrote an article titled “A Strong Jobs Report Friday Could Doom Biden’s $1.9 Trillion Stimulus,” capturing this dynamic.

Harris quashed that line of thinking early Friday on the Senate floor after an all-night vote-a-thon. “The yays are 50, the nays are 50, the Senate being equally divided, the vice president votes in the affirmative, and the concurrent resolution as amended is adopted,” she declared. The 51-50 vote sets into motion a series of events that will effectively allow Democrats to craft a stimulus bill in the next few weeks that can pass without any Republican votes under special budget rules.

The vote effectively dismantled the “good news is bad news” line of thinking that sometimes dominates the narrative leading into these jobs reports. Estimates from economists ranged from a 250,000 monthly decline in nonfarm payrolls to a 400,000 increase. But even if it had come in at the top end, few expected it would do much to alter the path forward on fiscal stimulus. “We can say with a straight face that if headline payrolls come in [greater than 1 million], the political calculus would quickly change in a way that lengthens the path to a deal,” Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets, wrote ahead of the report. “Alas, such a gain isn’t on the table; hence the apprehension regarding any call for NFP to derail stimulus.”

Indeed, some of the details from the report, the first since Biden’s inauguration last month, underscore the hardship job seekers still face during the pandemic. “Among those not in the labor force in January, 4.7 million persons were prevented from looking for work due to the pandemic; this measure is little changed from December,” according to a note from the Labor Department. Of those who are unemployed, almost 40% have been without a job for 27 or more weeks, the highest in about nine years. The number of job losses considered “permanent” increased in January by the most since September. It’s also worth noting that the government accounted for almost all the gains in the past month — private payrolls increased by only 6,000 in January.

The U.S. economy, in short, seems very much mired in a “K-shaped” recovery. That’s exactly what fiscal stimulus can help remedy. As I noted recently, from March 31 through Sept. 30, after Congress passed the first fiscal aid bill, the overall wealth of Americans in the bottom half increased by more than 20%, the largest two-quarter boost since late 2013, even though many are among those disproportionately affected by the pandemic. The measures included in the latest stimulus bill would keep up that effort.

So, no, the U.S. economy isn’t running hot on its own just yet. The push for more effective vaccine distribution still needs to be the priority to get more Americans to work. But in one fell swoop, Harris removed the worst-case scenario — a weaker-than-expected labor market and less-than-expected fiscal stimulus — from the equation even before the jobs report was posted. That sets the stage for a recovery that, at the very least, looks a lot like the past several months. That, in turn, could mean Treasury yields continue their slow grind higher.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.