(Bloomberg Opinion) -- The IPO market just got a shot of caffeine from JDE Peet’s BV. Don’t expect other consumer listings to get such a rush.

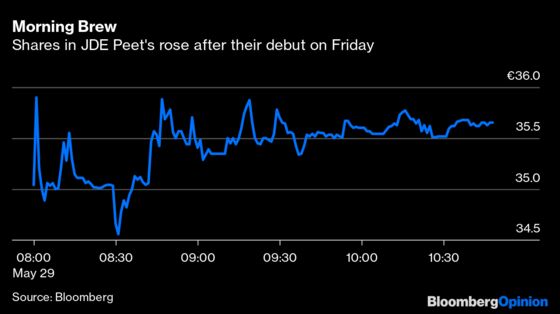

The owner of Peet’s Coffee, Douwe Egberts, Kenco and Tassimo on Friday priced shares in its initial public offering at 31.50 euros, in the upper half of the offering range, valuing the company at 15.6 billion euros ($17.3 billion), and rose to about 35.50 in mid-morning trading.

The biggest European IPO this year, pulled off in a swift 10 days, is a remarkable feat for a consumer business in the midst of a pandemic and a looming global recession. But JDE Peet’s has been uncannily well-placed to capitalize on changing consumer habits during lockdown, the prospects for reopening and a resurgence in equity markets.

The Dutch company was floated by JAB Holding Co., the investment fund backed by Germany’s billionaire Reimann family. Cornerstone investors, including funds run by George Soros’s firm, had agreed to take up a third of the offering, setting the tone.

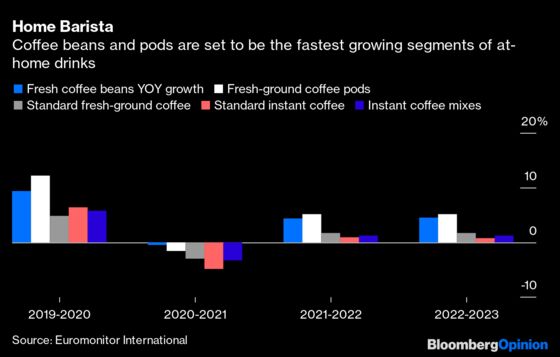

In a world crowded with coffee chains, JDE Peet’s gets 80% of its sales from coffee that is drunk at home. That meant it benefited as corner cafes shuttered and people working from home were forced to become their own baristas. Now that they can start going out again, it’s ready to serve them their favorite hot beverage too at the Peet’s Coffee chain. And just as Nestle SA benefited from people looking to stock up on the Starbucks-branded coffee it sells in supermarkets, so JDE Peet’s may gain new customers at its cafes if they discovered its products in the grocery store during lockdown.

As consumers navigate post-lockdown life, JDE Peet’s looks well insulated. That may explain why the valuation, as of mid-morning trading, is approaching that of Starbucks Corp. on a calendar 2019 enterprise-value-to-Ebitda basis.

With consumers likely pulling in their purse strings, homemade coffee may be more popular than pricey takeaway lattes. Yet the valuation may also reflect optimism about reopening, and expectations that people will be eager to get out and about. Early indications from U.S. retailers, such as discount-chain owner TJX Cos Inc. and even department store Macy’s Inc., are that sales have been stronger than expected since Americans were able to shop in person once again.

And let’s not forget about the IPO timing with stock markets gaining from their lows in March. That may be one reason why Peet’s was so keen on an accelerated book build: to avoid any sudden market turbulence.

The fortunate confluence of factors may not come together for other consumer-facing groups looking to float or spin off a division. L Brands Inc.’s desire to eventually separate its Victoria’s Secret lingerie chain comes to mind. It was grappling with a tired image and too many stores even before the Covid-19 outbreak.

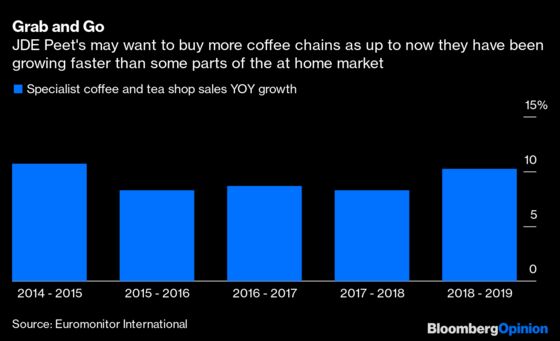

As for Peet’s, the successful float leaves it with firepower for further acquisitions. It plans to use the proceeds to cut debt — it aims to reduce the leverage ratio from 3.6 times to below 3 times by the end of the first half of 2021 — but it gets an acquisition currency in the form of equity.

Competition for coffee assets has been intense. There was a flurry of deals two years ago with JAB’s $2 billion purchase of Pret A Manger, which sells coffee as well as food to go; Coca-Cola Co.’s $5.1 billion swoop on Costa Coffee; and Nestle’s $7 billion deal for the rights to sell Starbucks coffee in supermarkets.

But JDE Peet’s could get lucky here, too, particularly in the market for drinking coffee outside the home. With the lockdown-induced distress in malls and on main streets, it may be able to grab something to go for a better price.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.