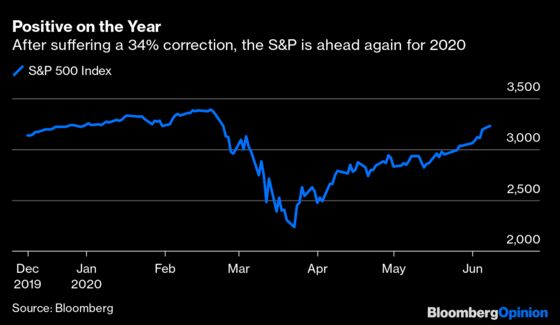

(Bloomberg Opinion) -- The U.S. Federal Reserve must be rather pleased with how it has contained the financial fallout from the pandemic. The S&P 500 index turned positive for the year this week and the Nasdaq reached a new high. The world is no longer clamoring for the dollar as a safe haven, and Treasury bond yields and corporate credit spreads are substantially lower than they were at the start of the Covid-19 crisis.

For Fed Chairman Jay Powell, dampening down volatility in the financial markets was the key to bringing things back under control. Only by taming the wild swings of March, when investors kept lurching from hope to despair, was it possible to tempt people back into risk assets such as equities and corporate bonds. The action by the central bank means we’ve just been through the shortest bear market in history.

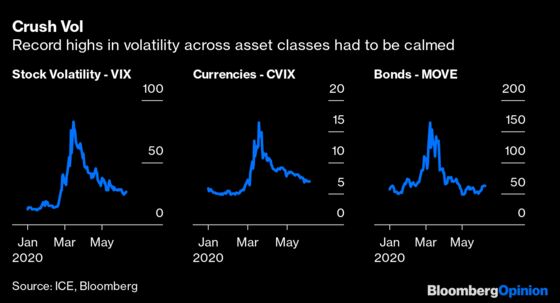

As the Fed can’t buy stocks, it had to manage this market rescue act by controlling the volatility of bond prices and by flooding the money markets. This gave investors enough of a feeling of security to start buying shares again, rather than sticking to haven assets.

By pumping in excess dollars and increasing so-called swap lines for foreign central banks — letting them deliver U.S. dollar funding to their country’s banks in a time of extreme market stress — Powell was also able to calm the sharp movements in currencies, which might otherwise have started an emerging markets crisis as investors fled to the greenback.

Using a similar playbook to the global financial crisis of more than a decade ago, although on a far bigger scale, the monetary authorities have successfully reflated financial valuations in all asset classes. That in turn should help restore economic confidence and lessen the depth and length of the recessionary impact of the lockdown. It’s to be hoped that last week’s surprisingly robust U.S. jobs data was an indicator of better times.

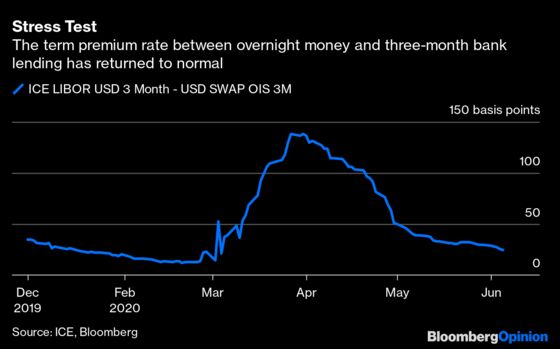

The biggest lesson from the last two crises is that the plumbing of the money markets is vital to stopping panic. This time, banks were charging a huge premium to lend longer than overnight and that was causing a breakdown in confidence across all asset classes, as well as that stampede into dollars. Even stable major currencies such as the U.K. pound were affected.

The Fed has increased its balance sheet by 70% to more than $7 trillion to fix these problems, so it might be time to rein back on some of the stimulus as the trade-weighted value of the dollar is turning lower at last, and the first phase of the pandemic eases in the West.

Yet Powell can’t relax his guard entirely. While equity volatility has fallen, it is still higher than at any other time since 2011. With Treasury bond yields rising sharply again last week, the Fed’s job isn’t over.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.