Cash Is No Longer a King Trading Strategy in Japan

(Bloomberg Opinion) -- Cash is king, unless you are in Japan. One successful trading strategy there has recently lost its luster, thanks to the Bank of Japan’s never-ending obsession with negative interest rates.

When a global recession looms, investors tend to hug stocks that pay handsome dividends. Cash rewards also have appeal at corporate headquarters. Since the collapse of Lehman Brothers, the S&P 500 companies have shelled out as much as 35% of their spending to buy back shares – even at the expense of capital investments – propelling the U.S. market to a record bull run.

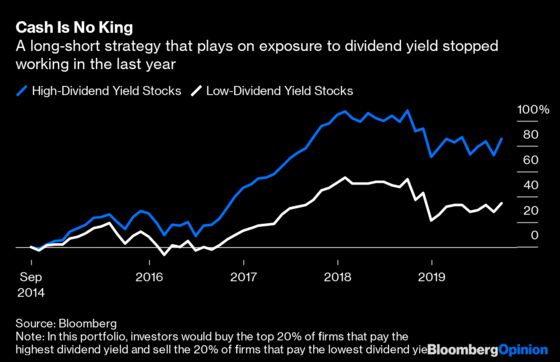

This magic wand is no longer working in Japan, however. Prime Minister Shinzo Abe has nudged Japan Inc. to improve shareholders’ returns – via dividend payouts and stock repurchases – since as early as 2013. Until recently, dividend yield was indeed a strong predictor of future returns.

Perhaps driven by the perception that their stocks are undervalued, Japanese companies are buying back shares at a record pace this year. In the half-year ending in September, buybacks almost doubled from a year before to 4.7 trillion yen ($44 billion). Companies on the Topix Index now generate close to 3% cash yield, the highest in three years.

Yet companies are no longer being rewarded. Dividend yield has not delivered superior returns in the past year. Share buybacks, meanwhile, have never impressed stock investors, perhaps because of their one-time nature.

What drives the investor indifference?

It could be that the dividend payers also tend to be structurally unattractive. Of the top 20% of Topix companies that pay the highest dividends, a good three-quarters are banks, which investors shy away from as long as the Bank of Japan continues with its negative interest-rate policy, dividends or not.

Another possible explanation is that cash is no longer a valuable asset to many investors. Combined, banks and insurers still own roughly 14% of Japan’s stock market and they have struggled to deploy their cash. Negative interest rates at home are forcing insurers abroad. Overseas assets already account for roughly 40% of their total investments.

Banks don’t want to hold any more cash, either, because they have to pay the BOJ for parking it there. Excess reserves in Japan have soared to over 60% of GDP, versus less than 20% in the Eurozone and even less in the U.S.

Indeed, if we construct long-short trading strategies based on single financial metrics such as sales growth or dividend yield, we can clearly discern the shifting taste of investors. Sure, profitability is still the trump card, but sales growth – a losing strategy in a seven-year horizon – is now making a sharp comeback, just at a time dividend yield is losing its appeal.

This could explain the severe polarization in Japan’s stock market. While 45% of the Tokyo-listed stocks now trade at less than one time book, stocks trading at more than 4 times book has reached its highest level, more than 10%, since 2006. Peptidream Inc., for instance, is one of those standout growth stocks; the biotech company now boasts $5.7 billion market cap on a meager $65 million annual revenue.

One concern with negative rates is that this kind of monetary policy forces investors to seek yields that don’t reflect the risks. From failing regional banks to retail investors dabbling in exotic foreign exchange trading, the BOJ already has enough worries. Now, the $5.8 trillion stock market is flashing red warning lights, too.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.