Undermining Activist Investors Will Hurt Japan Inc.

(Bloomberg Opinion) -- Having gained encouragement and some success during the rule of Prime Minister Shinzo Abe, foreign activist investors may be about to find Japan turning less hospitable. The government should be wary of alienating an ally that has aided its campaign to improve shareholder returns at the nation’s companies.

Overseas investors will have to report when they buy 1% of a company related to national security, down from 10% now, under rules scheduled to be passed by the Diet by Dec. 9. While the Ministry of Finance has announced a list of exemptions following opposition from market participants, hedge funds and private-equity investors remain perturbed amid a lack of clarity over how the law will be applied.

Dan Loeb, with tilts at Sony Corp. and Seven & i Holdings Co., and Paul Singer’s Elliott Management Corp. are among activist investors that have ventured into Japan since Abe unleashed the “third arrow” of his so-called Abenomics program: corporate governance reform. The premier was addressing a key problem of Japan Inc. Companies had long been awash with cash and stingy with buybacks or dividends, while minority investors often took a back seat.

The push has shown progress, as my colleague Shuli Ren has noted. Buybacks in Japan almost doubled to 4.7 trillion yen ($43 billion) in the six months through September from a year earlier. Takeover battles such as the tussle for developer Unizo Holdings Co., are a sign of how things have changed. A bidding war involving foreign private-equity firms including Elliott, Blackstone Group and Fortress Investment Group would have been almost unthinkable before Abe.

Stealth is a key weapon for activist investors, which buy large numbers of a company’s shares and then seek board seats to push for changes that will unlock value. Being forced to disclose when they have accumulated only 1% may tip off other investors to their interest, driving up the price and potentially making such strategies unprofitable.

Japan’s Ministry of Finance has clarified that foreign asset managers will be exempt from a pre-notification requirement only when there is “no intention to influence management,” Goldman Sachs Group Inc. strategists led by Kathy Matsui wrote in an Oct. 20 note. “This issue continues to be difficult to reconcile in the context of the government’s mission to promote greater levels of engagement between investors and corporate managements, as well as to protect the interests of minority shareholders.”

The list of sectors covered by the regulations is also broad. They include traditionally sensitive areas such as defense, agriculture, telecom, railways, nuclear power and utilities — but also categories such as information processing equipment, software and internet services, which typically rely on venture-capital funding. Deals such as Bain Capital’s buyout of Toshiba Corp’s memory-chip business last year are among those that might have been affected had the law been in place then. New York-based hedge fund Fir Tree Partners Inc. has invested in Kyushu Railway Co.

Geopolitics appears to be the motivation for what looks like a counter-productive move for Japan. China is the obvious target of the tightened regulations. Japan is a key U.S. ally, and Washington has been growing increasingly wary of Chinese investment amid rising trade tensions. The U.S. is drawing up a “white list” of foreign states that would be subject to lighter scrutiny of acquisitions made in America. Passing a stricter national security law gives Japan a better chance of being included in that list, according to Bloomberg Law analyst Grace Maral Burnett.

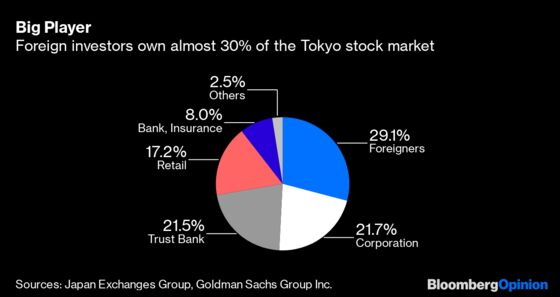

Abe’s government must tread carefully. Japan’s opening to overseas investors has benefited the stock market, with foreigners accounting for about 70% of Tokyo Stock Exchange turnover and 30% of market ownership, according to Goldman Sachs. Anything that forces the activists to pack up and go home would be a self-inflicted wound.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.