For Private Equity, Japan Still Beats China

Private equity funds are sitting on billions in potential investment. They’d be wise to look at Japan.

(Bloomberg Opinion) -- Japan lost its position as the world’s second-biggest economy to China awhile ago. But it’s beating out its Asian rival in one area at least: private equity. For restructuring experts such as KKR & Co. LP, whose founders recently declared Japan the company’s “highest priority” outside the U.S., the smaller country offers much more attractive opportunities. And the reasons are as much political as financial.

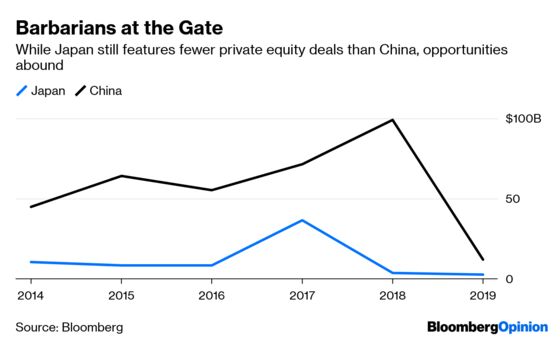

That might seem surprising, given that the Chinese market dwarfs Japan’s. (Private equity investment value in greater China, including domestic yuan funds, averaged $72 billion annually in the past five years, compared to just $9 billion in Japan.) The mainland features growth companies galore and easy exit opportunities through initial public offerings in Hong Kong, the U.S. and soon, for tech firms, Shanghai.

Private-equity companies from around the world have raised billions of dollars to invest in China, hoping to take advantage of its domestic consumption story and tech frenzy. KKR has bought into Chinese firms such as pork producer Cofco Meat Holdings Ltd. and personal-finance platform Shenzhen Suishou Technology Co. Ltd.

Yet several factors undercut China’s attractiveness. Typically, for instance, most targets aren’t as mature as those in Japan or the U.S.; they’re still in empire-building mode, so only minority stakes are available for purchase. Deals are in the range of a few hundred million dollars on average — small potatoes compared to Bain’s $18 billion purchase a couple years of ago of Toshiba Corp.’s memory chip business. Valuations, too, are frothy.

By contrast, as in the U.S., Japan’s dying conglomerates offer rich pickings. They house a slew of underloved or non-core assets: About a quarter of the companies on the Nikkei 400 have 100 or more subsidiaries apiece, and many have more than 300 divisions below the parent company.

There’s a real chance to create global leaders from these assets — an opportunity that China’s domestic-focused private equity investors don’t enjoy. KKR, which has been in Japan since 2010 and invested in six deals since then, has put this strategy to work with the healthcare business of Panasonic Corp., which it acquired in 2013. Since renamed PHC, the unit bought Bayer AG’s diabetes care unit and is in the midst of acquiring Thermo Fisher Scientific, Inc.’s pathology business. In 2016, KKR also bought auto-parts maker Calsonic Kansei Corp. from Nissan for $4.3 billion. The takeover target has since announced plans to buy Fiat Chrysler’s high-tech parts-making business.

Equally important is the fact that the Japanese government now actively supports such buyouts, a big change from the insular boom years when private equity firms were decried as rapacious foreign raiders. There was remarkably little public backlash after Toshiba sold off its crown jewel, or when Nissan sold Calsonic. At least in part, that’s because Prime Minister Shinzo Abe has pushed for a greater focus on corporate governance and shareholder returns. That means slimming down unwieldy conglomerates and revamping management at underperforming companies.

Foreign private equity firms can help do both, and then get these essentially mature businesses to expand globally. They can address another problem as well: Thousands of Japanese family-owned firms are facing potential succession crises as founders near retirement. That’s much less of a problem in China, where companies are newer.

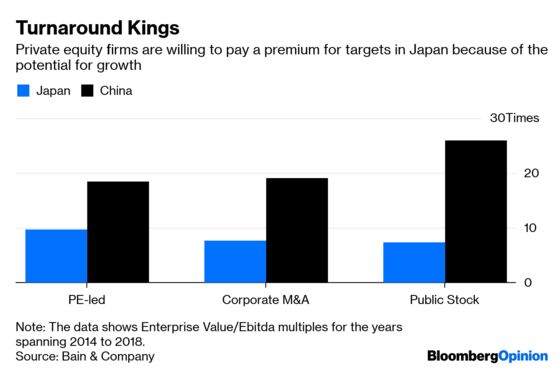

Investors clearly see opportunity. A study by Bain & Company found that private equity firms in Japan are willing to pay 9.7 times Ebitda in the form of enterprise value for their targets, while corporate acquirers and the stock market pay almost 25 percent less.

No one’s giving up on China; indeed, KKR’s own former China heads recently raised an eye-catching $2 billion for a debut private equity fund focused on the mainland. Yet, around the world, billions of dollars have been raised but not spent for lack of targets. That money might find a comfortable home in Japan.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.