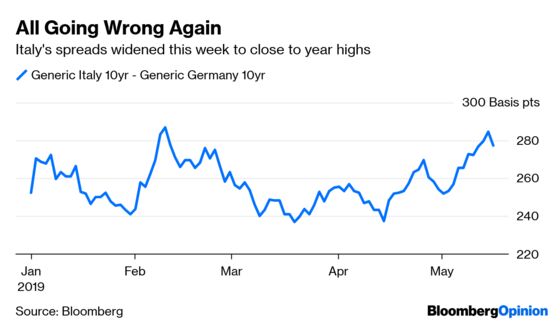

(Bloomberg Opinion) -- It’s become depressingly familiar to watch Italian government bonds yields push higher, with the spread over German bunds getting close again this week to its widest point of the year.

For that, you can thank more political posturing by the country’s populist leaders ahead of the May 23 European elections. Matteo Salvini, leader of the League and deputy prime minister, said he was prepared to countenance Italy's debt-to-GDP ratio reaching a whopping 140%. You can imagine how that went down in Brussels.

None of this ought to be a surprise. As I wrote a month ago, Italy is an accident waiting to happen from a markets perspective. Much of this is self-inflicted, of course, as my colleague Ferdinando Giugliano has pointed out. But there’s still a need for some grownup assistance, with the European Central Bank best placed to ease some of the pain. The only problem is it will need to be much more accommodating in terms of its policy decisions, and that’s by no means a given as rivals jostle – some of them hawkishly – to replace Mario Draghi as the bank’s president.

The ECB’s upcoming meeting on June 6 in Vilnius, Lithuania will be crucial in offering a sense of its future approach. It might provide a more positive outlook of Italian GDP than the European Commission, but forecasts are only part of the picture at the moment. The country’s economy is in a tight spot on any view.

U.S. President Donald Trump’s ratcheting up of China trade tensions is clearly negative for global growth, and any drop in Chinese orders for European goods will hit Italy’s export-led economy hard. Yet even a successful resolution of the U.S./China dispute might not do much for European countries, if it means the Chinese switch more of their import orders to American companies. And this is without even factoring in the very real risk of Trump taking aim at Europe in the upcoming EU/U.S. trade negotiations.

With this as the background, the ECB could certainly be more proactive in making sure there isn’t a tightening of financial conditions. Details are expected from the Vilnius meeting on a new round of super-cheap ECB loans to banks (known as targeted long-term refinancing operations, or TLTROs). This is especially pertinent for Italian lenders, which have some of the highest costs in the euro area. There is always caution about favoring one country too much, but given the state of Italy’s economy and politics, this isn’t the time to let those fears dominate.

The ECB needs to recognize that despite the euro zone’s fairly respectable first-quarter growth, there really won’t be much more good news this year from Italy and Germany, two of the bloc’s largest economies. You only have to look at the inflation forecasts to appreciate this point. Five-year forward inflation for the euro area, an indicator frequently cited by Draghi, is back to its 2016 lows. Similarly, 10-year German government bonds are yielding minus 0.1%. These warning signs should not be ignored.

Yet Europe is apparently no longer in crisis, according to the ECB, evidenced by its feeling confident enough to halt new bond-buying programs at the end of last year. That looks more and more premature with every passing month. The bank’s governing council needs to act now to prevent a slowdown becoming something more serious. Italy is the canary in the coalmine.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.