Italy and Austria Take the Bond Market to a Very Weird Place

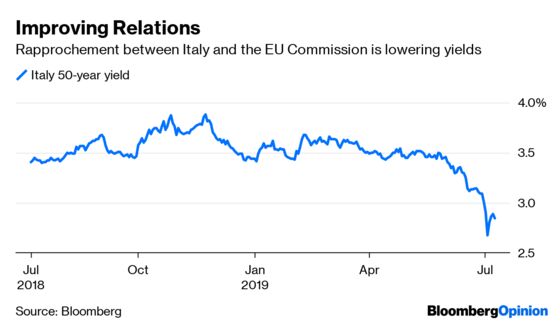

(Bloomberg Opinion) -- For the bond market’s “tale of two cities,” look at Rome and Vienna. Both Italy and Austria have come to the market recently with ultra-long duration debt sales. It’s remarkable that the latter managed to get a 98-year issue away with a 1.17% interest rate, but Italy’s 48-year offer this week at a near 3% yield is pretty miraculous too given all of the political and economic risk in that country.

Kit Juckes, a currency analyst at Societe Generale SA, wrote on Tuesday that “the shortage of positive-yielding ‘safe’ bonds is still driving investors to overpay for what’s left.” Not half.

I’ve written before about the Austrian offer and what it said about the market’s abject desperation for yield, but the Italian sale is the other side of the same crazy coin. Things are at a pass when “safe” investors have to sign up for 98 years to get 1.2% (a similar level to euro zone inflation), and those with appetite for a bit more risk have to swallow 48 years of Italy for a not-exactly eye-watering 2.85%. Many investors will be dead before the Italian paper matures; definitely so at the end of the Austrian bond’s term.

Bondholders are clearly dicing with danger by taking on such long-dated debt of a country like Italy, whose populist government is still battling with the European Union over its budget deficit. Whatever. There were still more than 18 billion euros ($20.2 billion) of orders for the 3 billion-euro offer. That was despite it offering just 11 basis points more yield than Italy’s 30-year benchmark bond.

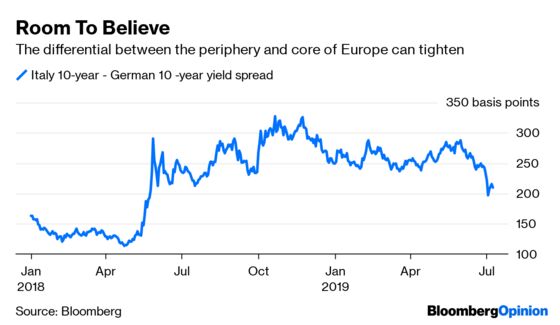

The hope among those buying in now is that Italian yields will fall further (bonds rise in value when yields drop) if relations stay cordial between Rome and Brussels after a recent thawing. The spread between the German 10-year benchmark bund and its Italian equivalent was as tight as 140 basis points in 2016; it is 210 basis points currently.

It’s certainly smart of the Italian treasury to take advantage of the unique environment to reach for ultra-long financing. At the half-year mark, more than 60% of the country’s 250 billion-euro funding requirement for 2019 has been completed. Significantly, much of it has been of a longer duration and that will relieve pressure for many years to come. At least this offers some consolation to investors that the risk of an Italian funding crunch is being reduced rapidly.

Of course, Austria's 98-year ultra-long security also carries risk given that its meager return is at or below the prevailing euro area inflation rate. Knowing whether either country will remain in fit shape to repay the principal over such a long time requires a strong constitution.

Still, the key metric for bond investors is that Austria’s government debt was just shy of 73% of gross domestic product at the end of the first quarter this year. Italy’s debt is running at 132.2%, and the European Commission estimates it will exceed 135% in 2020.

Yield-starved, euro-denominated investors probably have had little option than to buy both issues and blend the risks. But it’s alarming that these buying decisions – between safe and a bit more risky – are now having to be made on such absurdly distant time horizons. Who would want to be a fund manager holding a parcel of ultra-long bonds when the music stops?

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.