Is the Stock Market Overvalued, Cheap or Just Right? A Debate

(Bloomberg Opinion) -- Most discussions about the stock market eventually get around to the question of valuation: Are shares prices too high, too low or just right? But valuation may not offer the answers investors want to hear. Bloomberg Opinion columnists Nir Kaissar and Barry Ritholtz recently met online to debate.

Barry Ritholtz: Value as a measure means much less than many people imagine.

That sounds controversial, but it shouldn't be. “Stocks are pricey, overvalued and prone to crash” is something I have been hearing since the early 1990s.

Valuation measures are not useless; they just are not the be-all metric many believe. Valuation provides a rough range of expected returns – but only a broad estimate. In reality, fair value is a level that markets tend to careen past on their way to becoming incredibly cheap or wildly expensive. It is not a point where equities ever spend much time.

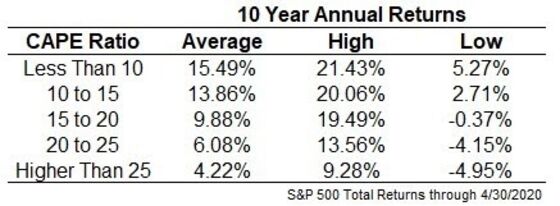

As the table below shows, averages can be misleading. The cyclically adjusted price-to-earnings ratio, or CAPE, produces a broad range of possible outcomes. Sometimes low CAPEs yield mediocre returns; other times expensive CAPEs generate very good returns.

Source: Ben Carlson

Here is a radical statement: For much of the past three decades valuation measures haven't been a useful guide for buying or selling equities.

Valuations matter -- just not as much as many people believe.

Nir Kaissar: I would argue that valuations matter more than people realize. If used properly, valuation is among the most powerful tools available to investors.

Here’s why: Most financial decisions require an estimate of future returns from investments. The problem, of course, is that no one can predict the future. So the question is: What is the most reliable way to estimate future returns?

This is where valuation comes in handy. There’s a strong correlation, for instance, between the U.S. stock market’s valuation, as measured by earnings yield (the inverse of the famed price-to-earnings ratio), and subsequent returns. That is, high earnings yields have historically signaled higher future returns and vice versa. From 1881 to June 2010, the longest period for which numbers are available, the correlation between the S&P 500 Index’s earnings yield and its subsequent 10-year total real return was 0.56, counted monthly. That’s based on cyclically adjusted earnings, but the correlation is similar using other measures of earnings.

And contrary to popular perception, valuation has been even more reliable in recent decades. The correlation spiked to a near-perfect 0.94 from 1990 to 2010. Why? High earnings yields during the stagflation of the early 1980s were followed by a two-decade bull market. Then, low earnings yields during the dot-com mania of the late 1990s were followed by a lost decade for stocks. And most recently, high earning yields during the 2008 financial crisis were followed by one of the strongest bull markets on record.

Valuations are similarly useful for gauging future returns from bonds and other stock markets. There are some important caveats, though. While valuation is a useful tool for estimating returns over a longer period, it tells you nothing about the path. It can’t tell you if or when markets will crash or how they’ll perform in the near term. Anyone using it for those purposes is likely to be disappointed, as you rightly point out.

Also, a strong correlation isn’t a perfect one, which means that valuation will be wrong sometimes. But it’s better than assuming, as many investors do, that future returns will resemble those of the past. Often, it’s just the opposite.

BR: On average, equity valuations have risen over the past century. Rising prices have scared off overly value sensitive investors away from many of the most lucrative investments in history. This is a reminder that no single metric alone should drive your decisions; everything requires proper context. Interest rates, inflation, innovation and creative destruction all matter.

Consider the past century of corporate America: Companies once required labor, raw materials and enormous amounts of capital. Think about the thousands of square miles of land railroads had to purchase, then buy and lay steel tracks. That’s before building locomotives, buying coal and hiring engineers -- and before steel companies built foundries to turn ore into iron. All of these were tremendously capital-intensive activities.

To attract investors, companies had to be cheap. Otherwise, they could not generate a sufficient return on capital. Today, it takes a few founders, a couple of laptops and access to cloud services to launch an enterprise.

Should 20th century and 21st century companies be similarly valued? The first expensively assembles material into a final product; the second cheaply manipulates digital bits. Of course, an investor is going to pay more for the latter than the former.

Shouldn’t investors change what they are willing to pay for equities given this changing corporate cost structure?

NK: I agree that companies have generally become less capital intensive over time.

It’s also true that the U.S. stock market has generally been more expensive in recent decades. Going back to my earlier example, the cyclically adjusted earnings yield for the S&P 500 averaged 7.6% from 1881 to 1994. Since 1995, however, it has averaged just 3.9%.

Is that the work of leaner capital structures? Hard to say. First, those trends began well before 1995, and yet valuations were lower in the 1970s and 1980s than during the two decades that preceded them. Second, the period since 1995 happens to include two asset bubbles in dot-coms and housing that pushed valuations higher. Third, recency bias may be exaggerating the importance of the last two decades, even though they represent only a small fraction of the historical record. And finally, there’s little evidence that evolving capital structures have boosted stock valuations in other countries.

Fortunately, it doesn’t matter. Investors have no ability to control valuations or predict where they’re going, so what’s driving them isn’t particularly important. Also, most investors should have some allocation to stocks regardless of valuations as part of a broadly diversified portfolio, and they should never blow out of them entirely because they think valuations are too rich. The evidence is overwhelming that all-in-all-out market timing is doomed to fail.

And regardless of what’s driving them, in addition to their usefulness as a gauge of longer-term returns, valuations can help tame investors’ demons. If you’re tempted to chase stocks in a hot market, low earnings yields are a good reminder that it’s probably not worth it. Inversely, if you’re tempted to dump stocks during a crisis, high earnings yields are a good reminder that staying in your seat can be rewarding. And for brave and disciplined investors, modestly adding to their stocks when yields rise and trimming them when yields fall may boost their returns modestly over time.

BR: Those are all persuasive points. We agree about much of this, but I suspect using very different analyses.

Where we differ is the concern of how valuation is used as a reason to sell (or not own) stocks. How bull markets progress over time, pull in new investors, change in character and valuation over the course of each secular cycle is an important but oft-overlooked point. The combination of investor psychology and market cycles affects buy and sell decisions, often for the worse.

Consider the 1982-2000 secular bull market. P/Es for the S&P 500 began that cycle at 7 and finished at 32. During that run, markets gained about 1,000%. Three-quarters of that was due to multiple expansion. In other words, investors were willing to pay more and more for the same dollar of earnings. Stocks were cheap at the beginning of the cycle, passed fair value somewhere in the middle of the cycle and were expensive during the last four years. It is hard to see how valuation measures were any help to investors over that period.

Why is this significant? Because when the cycle ends, stocks tend to give back 30% to 50% of those long-term gains. The challenging part from an investors' perspective is that those losses will be mostly made up through dividends and price appreciation while the news remains almost all bad. When the next secular bull market begins, those same investors who sold (or refused to buy) during high P/E stock markets tend to get caught up in all of the negative news flows. We have seen this too many times to count: Investor psychology leads those who depend too much on valuation metrics to miss the end of one bull market but -- even more importantly -- miss the beginning of the next cycle. Your comments as to why timing is doomed to fail are very well noted.

NK: Valuations weren’t helpful to investors darting in and out of stocks from 1982 to 2000 because they never are for that purpose. But they were a useful guide to future returns. The correlation between the S&P 500’s earnings yield and subsequent 10-year total real return was strongly positive during the period (0.67).

Your point about investor psychology reminds me of another reason valuations are useful: They’re the best gauge of the market’s mood. I often hear people arguing about whether investors are bullish or bearish. No need to squabble; that information is in the valuations.

For example, the P/E ratio of the S&P 500 based on analysts’ forward earnings estimates was 25.4 as of Monday, according to data compiled by Bloomberg going back to 1990. That’s just shy of the record of 27 set in December 1998. So despite what anyone may say to the contrary, investors in U.S. stocks as a whole are demonstrably bullish.

More generally, valuations are among the best tools we have for gauging future returns, which has many important applications such as planning and portfolio construction. It’s a shame that their misuse by some has obscured their utility.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

Barry Ritholtz is a Bloomberg Opinion columnist. He is chairman and chief investment officer of Ritholtz Wealth Management, and was previously chief market strategist at Maxim Group. He is the author of “Bailout Nation.”

©2020 Bloomberg L.P.