(Bloomberg Opinion) -- It’s slim pickings in the bond market at the moment. What else can fund managers do but fall into line with their index, close their eyes and buy?

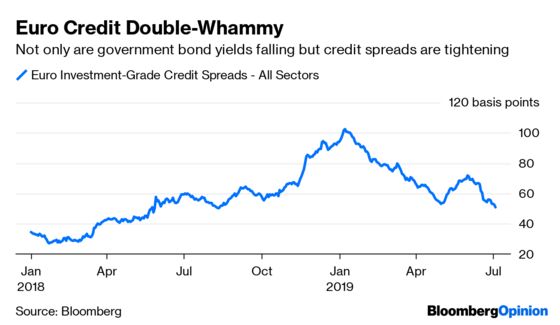

A pervasive fear of missing out on even the slightest hint of yield has created an unseemly buying frenzy that has swept across Europe, touching government bonds and making its way down the credit spectrum to high-yielding corporate debt.

It's become such a battle for investors to get hold of any form of fixed-income asset that yields on the bonds of France, Belgium, Austria and Sweden at a range of maturities, even beyond 10 years, have turned negative. U.K. retailer Marks & Spencer Group Plc, currently battling to revive earnings and figure out how to get people to buy its clothes, felt the FOMO. On Wednesday its 250 million pound ($314.3 million) eight-year bond was six times oversubscribed, and the spread on offer dropped 35 basis points from initial price talk to pricing.

The backdrop to this is an expectation that the European Central Bank will push its deposit rate ever more negative and restart quantitative easing in the autumn to battle the bloc’s worsening economic weakness. Good news for bond returns.

But there’s much more to the latest plunge in yields. The fund managers who, all year, had sat on the sidelines in the belief that they could not get any lower are now finding that their performance has fallen behind. Now, they have to catch up, and sharpish. This tectonic shift in fixed income is forcing them to make purchases that in the cold light of day defy logic. Underperforming in a bull market is not a good look.

One important law of financial logic – if you lend money for longer, you should see a higher return – has been broken. Long bond yields around the world have dropped below the official overnight rates of central banks. The time value of money has essentially disappeared.

The U.S. 30-year bond, for example, yields 2.47%, less than the 2.5% upper bound of the Federal Reserve's benchmark rate. It’s even worse in Europe. As my colleague Dani Burger puts it, the continent has gone beyond Japanification, now that a number of EU countries have a higher percentage of negative-yielding debt.

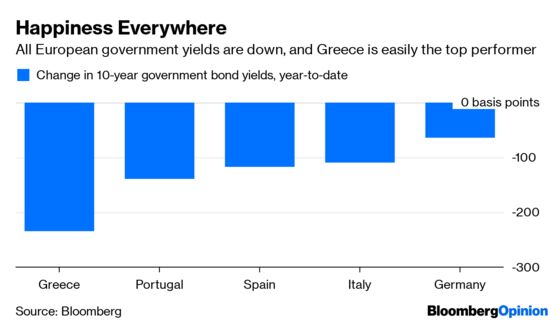

What sort of world is it when the Greek 10-year is within 10 basis points of U.S Treasuries? If you thought 1.17% was crazy for a yield on Austria’s reopening of its 100-year bond, it now yields 1.06%.

The evident desire of both the European Commission and the Italian government to avoid a summer row over government spending limits opened the floodgates for investors to pile into the last liquid market with any yield to speak of. The Italian curve has shifted so far down that two-year yields have returned to zero for the first time since the formation of the current populist government in May last year created a fixed-income drama.

Fund managers who, with ample justification, had been underweight Italy have had to cave in. The year is half over, and there’s no other way to keep performance from being destroyed other than capitulation against their better judgment.

Where does it stop? It doesn’t look like it will anytime soon. The consummate Euro-federalist Christine Lagarde will deliver continuity when she takes over from Mario Draghi as ECB president on Nov. 1. "Whatever it takes" is alive and well.

Fund managers have to strap on duration and secure any yield they can while it still sort of exists. Just try not to think about how all those pensions will get paid in the future.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.