What’s Driving Iron Ore’s Price Spike?

(Bloomberg Opinion) -- There’s nothing worse than things going crazy at the office while you’re away on holiday.

That’s what happened to Chinese iron ore traders over the past fortnight, after Vale SA’s Brumadinho dam disaster prompted fears that as much as 40 million metric tons of metal could be taken off the market while the Brazilian miner closed similar facilities.

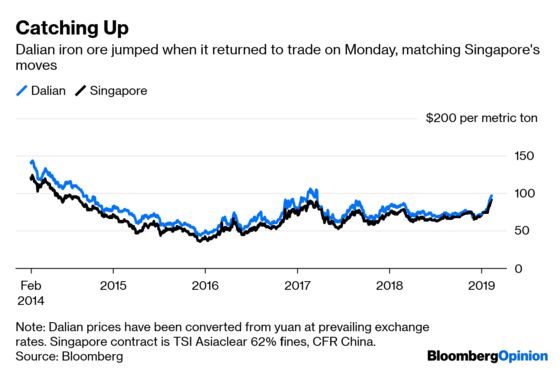

As mainland traders tucked into their dumplings with their families last week, down in Singapore iron ore futures jumped 8.4 percent on deepening concerns of a supply shortage. The main global contract traded in Dalian, to the southeast of Beijing, rushed to catch up Monday — putting in a 4.9 percent gain — after going dark throughout the Lunar New Year holiday. That’s the highest close in nearly two years.

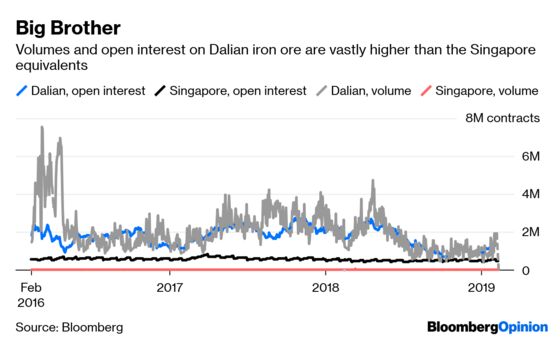

It’s increasingly rare for Singapore’s contracts to get the feeling of leading the Dalian market. Chinese iron ore is vastly more liquid, with typically two to three contracts outstanding for every one in the city-state, and nearly two million changing hands daily compared with 10,000 or so on the Singapore Exchange. That exaggerates the difference somewhat, since Dalian double-counts its buy and sell orders as separate trades and Singapore has some over-the-counter trades as well. Even so, bid-ask spreads (the best way of measuring liquidity) tend to be below 10 basis points, less than a third of what you see in Singapore.

That mainland dominance has only grown in the past year. In 2018, the Shanghai Futures Exchange established a new oil benchmark to challenge West Texas Intermediate and Brent, and opened it to foreign investors. Dalian later did the same with iron ore.

In many ways, the Dalian market has been more successful: While Shanghai’s medium sour grade has failed to really make a dent in the far more established New York and London-traded benchmarks, offshore iron ore investors appear to have moved en masse to participate in the mainland option.

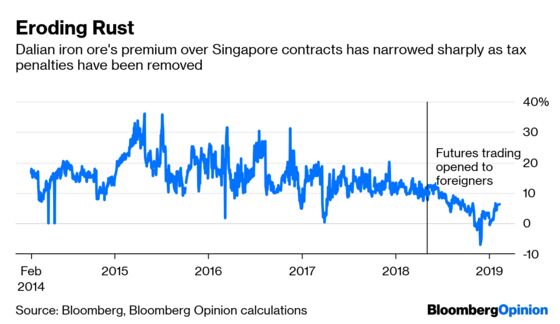

You can see this in the spread between the Dalian and Singapore contracts. Chinese-traded iron ore used to revert toward a level at least 17 percent above the offshore product, in line with the value-added tax that Beijing imposed on metal imports. Since last May, however, offshore traders have been able to participate in the iron-ore futures market tax-free as long as physical delivery of the product took place within bonded Chinese stockyards. As a result, the premium has vanished, or even gone negative.

That’s not entirely bad news for Singapore. The Dalian contract is physically settled, meaning that those holding long positions at the end of each month have to be able to take delivery of hundreds of tons of rust. In the city-state it’s cash-settled, so traders will instead simply see debits or credits in their Singapore Exchange Ltd. accounts.

In most commodity markets, the cash-settled contracts are more liquid. So it’s possible that with a tighter linkage to the physical market in mainland China, Singapore can become a place for global commodity traders to make speculative cash bets in sufficient volumes to drive improved price discovery.

That might particularly be the case given the city-state’s lighter-touch regulation of new products, such as options (an indispensable risk-management tool for most commodity traders that’s barely tolerated in mainland China) and cash-settled futures, such as SGX’s new high-iron-content 65 percent contracts which started trading in December.

Still, as we’ve seen in contracts ranging from apples and cotton to, yes, iron ore, the mass of retail investors who keep things so lively in mainland Chinese futures markets are often strikingly good at predicting the long-run direction of prices. As a result, it’s not clear the world needs an offshore cash-settled market.

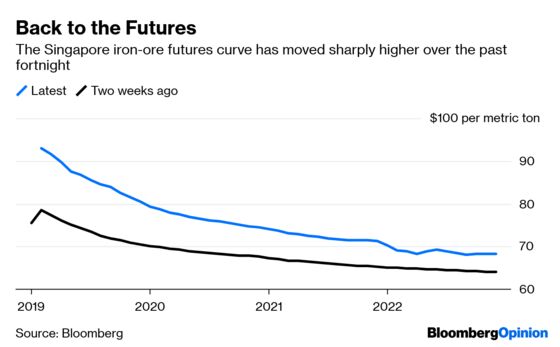

Given the signs of rapid weakening in the demand side of the iron ore market, the best bet is still that the current price spike is a short-term squeeze prompted by worries of a Brazilian supply shortage. Still, pricing of futures contracts in Singapore didn’t touch $80 a metric ton at any point just two weeks ago; now, thanks to the rapid rise at the front of the forward curve, it doesn’t drop below that level until 2020. Dalian’s refusal to repudiate the past week’s price action in Southeast Asia should give iron ore bears (including this columnist) pause for thought.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.