(Bloomberg Opinion) -- The stock market has a message for U.K. companies: Don’t come begging.

Kier Group Plc’s emergency fundraising was shunned by most of its shareholders on Thursday. The British construction firm has its problems — but there’s a much broader warning here. If banks further withdraw funding for U.K. Plc, equity investors can’t be relied on to fill the hole.

Three weeks ago, Kier shares traded in a different universe. The company was worth 735 million pounds ($934 million) before it cautioned that lenders wanted to cut their exposure to the company and the industry, and that customers were directing new business to contractors with low levels of leverage. Kier moved to raise 250 million pounds in a rights offering. A group of investment banks agreed to be the buyers of last resort in return for a 14 million-pound fee.

But the stock plunged below the price at which the new shares were being sold. Some investors supported the fundraising out of loyalty; others will have been offered a fee by the underwriters to do so. Still, the bookrunners will be left with just under half of the offering, racking up a paper loss as big as their fee.

The cash call clearly needed a bigger discount than the 34 percent set. But pricing the shares more cheaply would have meant issuing more stock to raise the same sum. That would have required a shareholder meeting and slowed the process down. The money wouldn’t have arrived in time to boost Kier’s balance sheet in time for the year-end.

While the company got its money, the market now sees it as a riskier business with diminished prospects. Kier has a market value of less than 600 million pounds, based on the current stock price and the increased number of shares after the offering. The new money appears to have made no difference to the outlook for the business, but without it, would Kier have been worth even this much? It’s hard to see how it could have won much new work next year given its indebtedness.

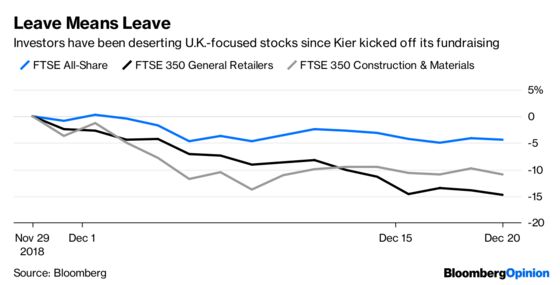

Construction has an easy bear case given the lumpiness of low-margin contracts and the collapse of Carillion Plc. Most shares in the U.K. building industry have been hit since Kier announced its fundraising. But then so have the U.K. mid-cap sector and retail index as well.

There are fewer than 100 days till Britain is due to leave the European Union. British lawmakers are divided on what to do. Amid that uncertainty, don’t expect banks to rush to lend to U.K.-focused corporates. It’s now clear the equity market is loath to be an alternative source of finance.

It’s possible the situation will improve in January, when asset managers aren’t so fearful about meeting their performance targets for the year. If not, British companies face a year of self-help — cutting costs and selling assets. Those that can’t will have to pay a high price to secure immediate funds.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2018 Bloomberg L.P.