Insurers Won’t Save a Heating World From Floods and Fire

(Bloomberg Opinion) -- There’s bad news for those looking for comfort in the face of flooding that’s inundated cities in China, Germany and India and wildfires that have consumed suburbs in California, Canada, and Australia: The insurance industry isn’t planning on hanging around to bail you out.

An insurance rescue mission is such a routine aspect of natural disasters in rich countries that the value of losses from major events is often as familiar as their physical characteristics, such as wind speed or Richter magnitude. The industry paid out $82 billion in such losses last year alone, according to Munich Re AG, and some $143 billion of catastrophe bonds have been issued since 1997.

As anyone who’s tried to put in a claim knows, though, insurance isn’t charity. If it becomes too expensive to cover losses for natural disasters, insurers and reinsurers will raise prices and pull back toward areas that are more profitable.

Worryingly, we’re already seeing signs of that happening in precisely the areas that are hitting the headlines. People with homes in high-risk regions that are currently protected by insurance coverage need to think about what they’d do if that safety net was whisked away.

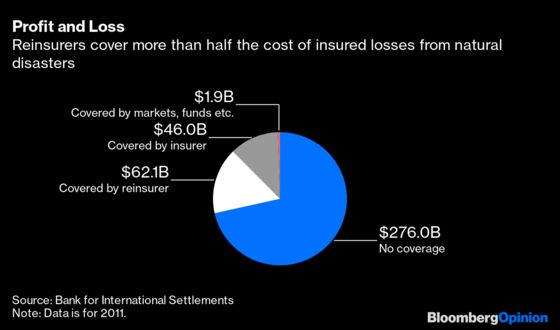

Reinsurers — the places where insurance companies get their own insurance — are crucial to how the world handles natural disasters. Despite representing only 5% or so of the $7 trillion in gross premiums written by the industry each year, reinsurers use their global reach and huge balance sheets to cover as much as two-thirds of the losses from major events.

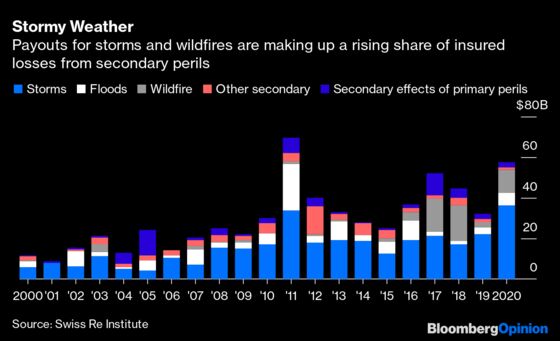

Those have been rising dramatically. Disaster payouts last year were the fifth-highest in history. There were no catastrophes on the scale of the 2011 Tohoku earthquake and tsunami, or of Hurricanes Harvey, Irma and Maria in 2017. Instead, an increasing proportion of losses have resulted from so-called “secondary perils” — landslides, wildfires and drought, as well as flooding, wind and hail damage from storms. These tend to be smaller-scale and harder to predict than the vast calamities inflicted by cyclones and earthquakes.

Traditionally, reinsurers haven’t paid much attention to the distinction between these secondary perils and the larger catastrophes in which they specialize. While front-line insurers argue with their customers and lawyers about the nature of the disaster and whether it was covered by a policy, reinsurers simply pay out whenever covered losses rise above the level where they’re on the hook for a slice of the cost.

As the frequency and severity of small-scale disasters increase, they’re having to pay more attention. Swiss Re AG, the world’s largest natural catastrophe reinsurer, said last year it had started paring back parts of its portfolio with high exposure to secondary perils, and is raising its modeled risks associated with weather events in Australia, typhoons in Japan and wildfires in California. That will increase the costs of coverage for primary insurers and customers down the chain.

“Our aim was to move more out of those unmodeled risks,” Swiss Re’s head of underwriting, Thierry Leger, told an investor call in February. Secondary perils had been making up a larger and larger share of losses, he added: “That trend we had to break as well.”

Climate change makes all these problems more difficult. Insurers’ models for the cost of natural disasters are based on historical data, but those trends are shifting in unpredictable ways as the climate warms. A warmer atmosphere, for instance, is able to carry more moisture. That’s likely to be contributing to the devastating recent flash floods in China’s Henan province, in Germany and Belgium, and in parts of India’s Maharashtra state, as clouds are now able to hold unprecedented volumes of water before dumping them on populated areas.

Whenever scientists respond to natural disasters with awe at the gathering speed of these climate effects, it’s likely that reinsurers will be reacting with something closer to alarm. To a meteorologist, a broken model is a research opportunity. To a reinsurer, it’s a threat to the business — while the worst effects will fall on individuals, who already bear nearly three-quarters of natural disaster costs.

All that is going to lead to increased premium costs, exclusions and deductibles. Even absent climate change, the effects of the Covid-19 pandemic will lump an additional $50 billion to $80 billion of costs on the industry, making it one of the most expensive disasters in history. Germany's recent floods would add as much as 5 billion euros ($5.9 billion) on top of that, and the damage from the Chinese and Indian floods and Canadian wildfires is still being assessed.

Meanwhile, record-low interest rates are making it harder for insurers to make money from debt-heavy investment portfolios, forcing them to push harder on maximizing earnings and minimizing losses from underwriting if the business as a whole is to make a profit.

Reinsurers can help to move some of the costs of climate change around, but they don’t have magical powers to make them go away. After a period during the past decade when the cost of reinsurance was pushed down by hedge funds, pension funds and sovereign wealth funds moving into the market, we’re now facing a cycle of hardening. That means a larger share of costs are being kicked back to primary insurers and consumers, just as climate change starts increasing the frequency of disasters.

When the final bill for the next decade’s floods and wildfires and hailstorms comes due, an insurance industry with an eye on its own survival will have already minimized its own exposure. It will be you and I who have to pay.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.