Insider Trading Is Rife With No Regulators in Sight

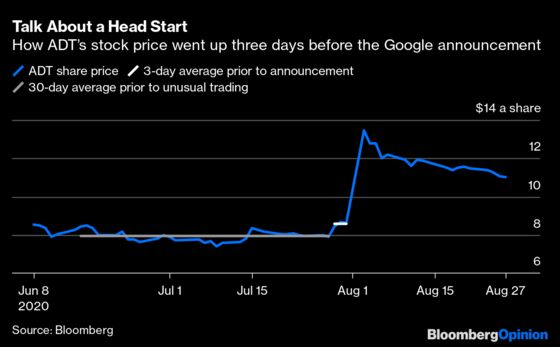

(Bloomberg Opinion) -- At 6 a.m. on Aug. 3, Google bought a 6.6% stake in ADT Inc., the largest U.S. home security company, for $450 million. ADT appreciated 100% as soon as the stock market opened. But the headlines detailing the transaction weren't a total surprise because more than a few people knew ADT was poised to benefit from an event big enough to be gaining Google's hitherto inaccessible technology.

Three days earlier, when ADT wasn't reporting much of anything, a series of computerized trading alerts derived from the algorithms of Bloomberg Automated Intelligence (BAI) revealed insiders' unmistakable handiwork:

-- On July 29, the frequency of people searching for articles about ADT and reading them exceeded the most recent 30-day average.

-- The same day, ADT rose 6.3% via trades 90% more numerous than the 20-day average and when its weekly gain until that point was 4.1%. ADT competitors closed with an average decline of 2.6%.

-- On July 30, ADT bonds changed hands four times more than the five-week average.

-- The following day, ADT volume jumped to more than five times the 20-day average.

All of this activity means investors, who were informed enough to buy ADT at $7.91 a share before the BAI alerts, could sell the stock at $17.21 on the news of the Google stake in ADT. The return was 118%, or the equivalent of turning $1 million into $2.8 million in four days.

Trading was significant: The three-day average value of the shares ($8.55) prior to the deal's disclosure was 8.2% greater than the 30-day average price prior to July 29, indicating investors' behavior changed in the 72 hours of trading before the news, according to data compiled by Bloomberg.

There's no end to the parade of corporate transactions preceded by trading underlying their selective disclosure. And there's no sign regulators see the possibility of insider trading in at least a dozen of them during the past year, including Google's offer for Fitbit, LVMH's plan to buy Tiffany, Avaya's strategic partnership with RingCentral, and Stryker’s taking over Wright Medical.

That's too bad because financial markets provide the clearest signals of people profiting from confidential information.

August 2019 was an especially busy month for unexplained, nicely timed trades. They began before Carl Icahn disclosed his stake in Cloudera Inc. Muddy Waters Research acknowledged short-selling Burford Capital, and Philip Morris announced talks to acquire Altria Group. Millions of dollars were pocketed from anomalous trades with the belated disclosure of these deals, according to data compiled by Bloomberg identifying unusual price fluctuations.

The stock market was little changed during the middle of Aug. 6, 2019. Amid the serenity, Burford Capital tumbled 8.1%, a loss bigger than any daily decline in 16 months, according to an automated Bloomberg report conceived to alert investors to abnormal moves in the market in the absence of any news. Trading in the company's shares was 76% greater than the 20-day average.

Burford, which provides financing for corporate litigation, arbitration and other disputes, ended the day down 18.8%, the largest slump since the company's initial public offering in 2009. Nothing was said about this aberration at the end of the day when the benchmark FTSE 100 index retreated less than 1%.

The company’s Burford's calamity deepened on Aug. 7. Muddy Waters, the firm founded by Carson Block to profit from inflated valuations by selling borrowed securities and buying them back later at a lower price, said Burford's accounting was flawed. Burford shares plummeted 66% before closing down 46%. The short-selling before the Muddy Waters announcement realized a profit of as much as 85%, or $1 million for every $1.85 million over two days.

Several hours before Icahn reported a 12.62% stake in Cloudera Inc. on Aug. 1, Bloomberg alerts provided multiple indications of market chaos for the Palo Alto-based maker and distributor of software for managing business data. Just after 10 a.m., the measure of future price swings, or implied volatility, surged to a level higher than 80% of every session during the past 12 months.

By 1 p.m. Cloudera was up 5.4%, more than any daily gain since June 17, 2019, and trading in options, which give holders the right to buy the shares at a specified price, exploded to triple the 20-day average. Within a span of 30 minutes, the number of social-media postings rose more than fivefold to 10 per 30 minutes from the average of 1.8 — completing every form of notification of unusual trading when there was no news to explain it.

By the end of the day, Cloudera was up 6.2% when the benchmark Russell 2000 Technology Index fell 0.3%. It was an exceptional outcome for a company whose shares rose more than 6% on only six days during the previous 12 months, when earnings exceeded analyst estimates or the analysts pronounced themselves bullish on the company. But there was no such news spurring the latest rally, even though every automated alert was triggered by the abnormal trading.

Sure enough, after the market closed, Carl Icahn's nearly 13% stake was disclosed. The previously unfathomable trading now made perfect sense. Call options that allow investors to benefit from rallies — and are among the most-traded derivatives — gained more than 10% on Aug. 1 after advancing more than 13% during the preceding few days for a record net increase. Anyone who purchased these options reaped a 30% profit in two days.

The extraordinary activity in Burford Capital and Cloudera were the warm-up acts for the climax on the morning of Aug. 27, 2019, when Philip Morris Inc. announced that it was in discussions with Altria Group Inc. over what it said was a potential all-stock merger of equals.

Four days earlier, the value of puts, or options that give holders the right to sell Philip Morris shares at a specified price on a specified date, gained 81% without a snippet of news to justify the activity. Early the next trading day, Aug. 26, Philip Morris options changed hands at a rate more than triple the 20-day moving average as the most-traded options on the day. The puts, allowing holders to capitalize on their bearish bets, appreciated 139%.

By noon, Philip Morris shares were in a free fall, plummeting 6% in their worst loss of the year. The carnage occurred when the benchmark S&P 500 index climbed 1.2% on the day.

The denouement was perfect as these hitherto inexplicable trades reaped a bonanza after the Philip Morris announcement. The shares fell 7.76% to the lowest price since January 2019 and the biggest loss since April 2018.

The S&P 500 was calm by comparison, down 0.3%. The options traders making the bearish bets preceding the company's statement collected a profit of as much as 760%, or $7.6 million for every $1 million they invested, during the preceding three trading days.

These aren't isolated examples of bizarre activity during the busiest year for mergers and acquisitions since at least 1998 when data started. They actually help explain more recent examples of probable market manipulation, such as Fitbit options surging during the week leading up to the Google takeover indicating a bid was imminent in the absence of any news.

Trading in Tiffany exploded along with its measure of implied volatility before LVMH's announced offer. Wright Medical similarly rallied in the absence of news before the Stryker acquisition announcement. People purchased Ring Central options just before the announced partnership with Avaya.

All of these publicly traded companies are noteworthy. Their valuations changed significantly in the absence of any explanation before inexplicable trading was confirmed by public information.

In a recent study of BAI stories on 5,000 U.S. companies during the past two years, Bloomberg quantitative analysts found that 20% of the time, through its automated news, certain combinations of alerts, including stock trading, social media activity and credit default swaps, were followed by a mergers-and-acquisition announcement in five days. The ratio is triple the outcome if all anomalies were to occur randomly.

So where are the regulators?

-- With assistance from Shin Pei.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew Winkler, Editor-in-Chief Emeritus of Bloomberg News, writes about markets.

©2020 Bloomberg L.P.