The Fed's Inflation Logic Is Flawed, and Dangerous

(Bloomberg Opinion) -- With one voice the Federal Open Market Committee declaims that it’s too soon to tighten monetary policy. Thus are short rates kept at pretty much zero and long rates suppressed by dint of the U.S. central bank buying $120 billion of Treasuries and mortgage-backed securities every month.

In speech after speech every committee member declares that the sharp pick-up in U.S. inflation is temporary and that it’s just fine to have a bit of an overshoot to make up for undershooting the target before. That they’re all so consistently dovish doesn’t necessarily make them wrong. But their reasoning is poor, and dangerous.

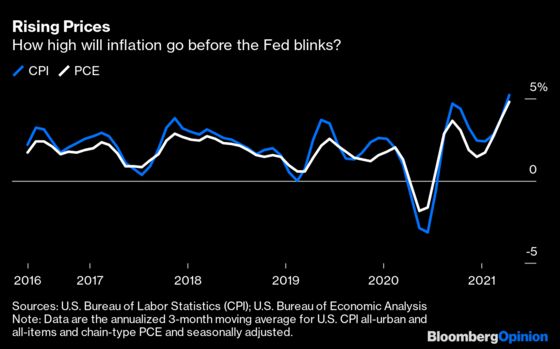

Start with the Fed’s first argument, the oft-repeated claim that the rise in inflation is caused by base effects. The reasoning’s simple: If inflation dropped like a rock in the pandemic then of course it would go up when the economy recovered. Trivially this is true. But the sharp rise in inflation in the past few months — in April, CPI and PCE inflation (the Fed’s favored gauge) rose 4.2% and 3.6% respectively compared with the previous year — is due only partly to base effects.

You can see this by refining the year-over-year comparisons. The chart below shows both CPI and PCE measured by the annualized change in the last three months compared with the previous three months. On that measure CPI is rising at an annual rate of 5.2% and PCE by 4.8%. That’s already higher than the pick-up after the financial crisis, when the collapse in inflation was far deeper. Both measures will almost certainly be higher still in May.

This brings us to the second reason given for why inflation is temporary: that demand is picking up faster than supply right now but that supply bottlenecks will ease over time. The first part of this analysis is correct, but there are problems aplenty with the second bit. There’s no evidence that supply blockages are loosening. Company inventories are at rock bottom. Every corporate survey, including this week’s manufacturing and non-manufacturing ISMs, shows huge worries about rising costs. The same is true of services.

In the meantime we need to consider how much inflation will rise even if it were only “temporary.” On current trends it wouldn’t surprise me if headline CPI averaged 5% this year, even if it falls next year. This means it has further to rise. Armed with massive fiscal and monetary stimulus, the U.S. economy, lest we forget, is really only starting to emerge from the pandemic.

The Fed’s third reason for holding firm is that the domestic output gap is still negative. In English, this means that the central bank believes the economy won’t get a sustained pick-up in inflation while demand is lower than its measures of potential supply. Snuggled within this argument is the Fed’s view that unemployment still has a long way to fall before the economy becomes overheated.

Unfortunately, this may be complacent. There are signs that many people are choosing not to work, either because they’re being paid to stay at home or because they’re frightened of going back to work because of Covid. Companies say they’re finding it hard to find workers. This would be consistent with the lackluster employment gains in last month’s non-farm payroll report. We’ll find out more in Friday’s report for May. The risk is that companies will have to increase wages yet further to lure workers. More generally, I suspect the economy is a lot tightener than the Fed believes.

The Fed’s last argument is that it’s been fighting disinflationary forces for 25 years or so and that there’s no reason to think they have gone away. This is wrong. Domestic, non-tradable inflation, especially services, has been remarkably stable at about 2%. It is prices for manufactured goods that have fallen. And yet, prices of tradable stuff have been rising at a furious pace of late and that shows no sign of abating. Global supply chains have been — and are still — far more damaged than they were in the financial crisis. Small wonder that North Asian export prices have exploded higher.

The question now is whether prices in the ravaged services sector start to pick up smartly as the economy reopens. I think they will because the companies left standing will need to make up for their losses by raising prices and because, being fewer of them, they can.

All this would perhaps be less of a problem were asset markets not at such nosebleed levels. There was a time, all the way back in 2018, when Fed Chair Jay Powell, among others, said signs of overheating could show up in asset prices. Even though they’re much more expensive than they were back then, all the Fed says now is that markets are a bit frothy, Actually, they’re the financial equivalent of a cappuccino: mostly froth and not much coffee.

If I’m right about inflation, the Fed, however reluctantly, will be forced into a volte face. At that point asset prices will fall, probably a lot. That’s the big danger. And I suspect the Fed knows it.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Richard Cookson was head of research and fund manager at Rubicon Fund Management. He was previously chief investment officer at Citi Private Bank and head of asset-allocation research at HSBC.

©2021 Bloomberg L.P.