Markets Have Infinite Reasons to Be Cheerful

(Bloomberg Opinion) -- As we head toward the end of 2020, we’ve spent the final run-up to Christmas much as we have the rest of the year: worrying about Covid-19. The beginning of this week saw a switch into risk-off mode in financial markets as a fast-spreading new virus strain emerged in Britain and Western health systems remained under pressure. That has shaken confidence in a positive start for 2021.

But the momentum behind the global recovery trade will take some stopping. Now would be the time for investors to take advantage of any temporary setbacks and keep the faith that the pandemic will eventually dissipate. Vaccine makers seem confident that their shots will cope with the new mutation, and if all else fails we can rely on central bankers to do whatever it takes to defend economies and markets.

Never has the traders’ mantra “Don't Fight the Fed” been so accurate. There’s every indication it will be the same in 2021.

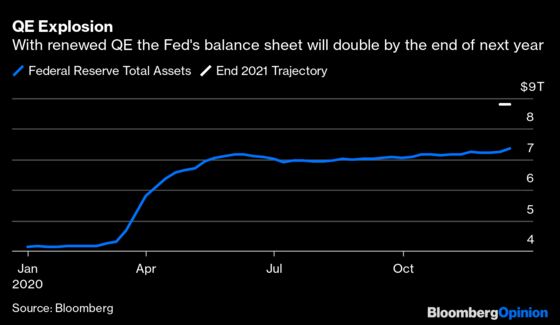

Some $5.6 trillion of stimulus has been pumped into markets by the major central banks since March, so it’s no coincidence that we end the year with record highs for U.S. Stocks and global bond yields close to all-time lows. Ever since the global financial crisis, central bankers’ Quantitative Easing habit hasn’t been shaken off. This year has seen the biggest asset-price reflation ever. One thing is certain for 2021: There’s another generous helping already lined up.

The U.S. Federal Reserve confirmed last week that $120 billion of Treasury bond and mortgage-backed securities will be acquired per month, plus a smattering of other securities that may be added according to discretion. That’s nearly $1.5 trillion over 2021, on top of the $3.3 trillion bought by the Fed in 2020. Add in all the U.S. fiscal stimulus as well, with a $900 billion package finally approved by Congress, and it’s safe to say there’s a favorable backdrop for investors.

The rest of the world isn’t leaving the heavy lifting to the Fed. The European Central Bank just added another 500 billion euros ($610 billion) to its pandemic response, bringing it up to a total 1.85 trillion euros stretching into 2022. The Bank of England has made another 150 billion pounds ($20 billion) of QE purchasing power ready for dispersal next year. The Swiss National Bank took the news of being labelled a currency manipulator by the U.S. Treasury with the vow to renew its interventions (its purchases of foreign currency end up in equities and bonds). The Bank of Japan has bought more than 7 trillion yen ($70 billion) of equity-linked exchange-traded funds this year.

So globally there will be both the ongoing flow of new QE into the system and the benefits of central banks maintaining their huge existing “stock” of bond holdings. Ever higher balance sheets can only bolster asset prices. Analysis from the Bank of England shows that in the absence of bank lending — which creates new assets — all QE can do is inflate the value of existing assets. This is infinite money chasing finite assets such as stocks and bonds, and even Bitcoin.

Two things have been missing that have thus far impaired QE’s effect on economic growth. First, the transmission mechanism via banks into real-economy lending hasn’t been functioning properly; it’s been particularly lacking in the European Union. Second, there has been a noticeable absence of aggressive and focused spending from governments on measures that will lift economic output meaningfully.

Happily, the fiscal side of the equation is finally being addressed with the accelerated distribution of government spending packages kicking in next year across much of the world — notably in the EU with its groundbreaking 750-billion euro pandemic recovery fund. The coordination of monetary policy and fiscal stimulus should create a multiplier effect if done properly.

There are plenty of negatives still around, but my colleague Cameron Crise reminds us of an episode from the trading classic “Reminiscences of a Stock Operator,” where a crafty market veteran keeps repeating, “It’s a bull market, you know.” The big money is made following the big trend not exiting on temporary setbacks. Keep in mind what the Fed and its many friends have in store next year.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.