Read India’s Tea Leaves in Bonds, Not Stocks

Gas prices & higher yield curve are better indicators of rising discontent than shares floating on government-injected liquidity.

(Bloomberg Opinion) -- Consumers are feeling cheated at the gas station. Investors are returning empty-handed from government bond auctions. The Indian state is struggling to make its fiscal math work without shortchanging the first group or disappointing the second.

Each of these discontents could curtail a still-unfinished recovery from the massive Covid-19 disruption. But you wouldn’t see any of those concerns reflected in the stock market, which is floating on $85 billion of liquidity pumped into the banking system in less than two years. At the height of the optimism surrounding the 2014 election that brought Narendra Modi to power, the benchmark Nifty 50 index peaked at a price-to-earnings ratio of 23. The multiple is currently at 36 and climbing higher.

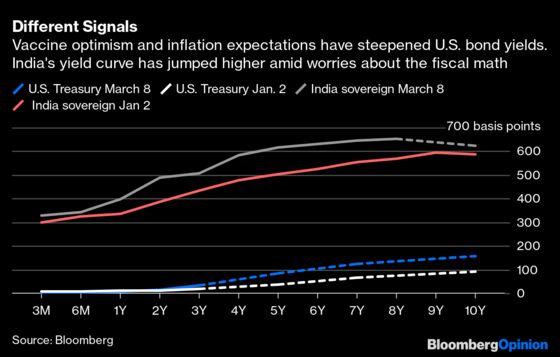

The liquidity magic isn’t working on bond markets, though. Steepening U.S. long-term yields, an offshoot of vaccine optimism and hardening inflation expectations, are setting the stage for a selloff in emerging-market debt. In India, the story is different. The entire yield curve has moved higher. This isn’t a sign of optimism about growth, but a worry about rising oil prices and the hard-to-square arithmetic of next fiscal year’s targeted budget deficit of 6.8% of gross domestic product, on top of an expected 9.5% shortfall in the current year that ends on March 31.

Since the government announced those figures, only two-fifths of the sovereign notes put up for sale have been bought by investors. The rest of the auctions were partially cancelled or devolved on primary dealers.

Investor anxiety has a lot to do with gasoline and the strain it’s putting on stretched household budgets. Monday’s price of 97.6 rupees a liter in Mumbai ($5 per gallon) was 65% higher than in New York. Between 2012 and 2014, when crude oil was hovering near the $100 level, the average price gap between the two cities was 30%.

The discontent caused by that surge was was masterfully utilized by Modi’s campaign, which blamed the previous government’s policies for causing people to suffer. But after he came to power as prime minister, his administration didn’t pass on the subsequent decline in international crude prices to consumers. It kept most of the windfall and spent it. Six years ago, fuel taxes made up less than 10% of the Indian government’s revenue. Now, they account for almost 20%.

More than half of what customers pay goes into the kitties of federal and state authorities. Had petroleum products been put under India’s 2017 goods and services tax at the top rate of 28%, the burden on the common man today would have been no more than 75 rupees for a liter from an average imported crude oil cost of $60 a barrel, according to State Bank of India economist Soumya Kanti Ghosh. Households could have used the savings to increase discretionary spending.

State governments, which were surrendering most of their local levies for a share of the nationwide tax on consumption, didn’t want to lose all leverage over their revenue. So petroleum products were kept out of the GST. But the new system didn’t live up to its billing, leading to a 1% of GDP revenue shortfall — an unacknowledged fiscal crisis — between April 2018 and March 2019.

Then came the pandemic, which created a whole new fault line of vulnerability. It runs from consumers who are finding gasoline, diesel and cooking-gas prices unbearable to the government that can’t afford to cut its high fuel taxes — lest the bond market is spooked further. Sitting on this fractured ground is a state-dominated banking system that has yet to account for most of its pandemic-related stress. When it eventually does, a less-than-healthy consumer economy and small-and-midsize firms propped up by emergency state-guaranteed loans could lead to a fresh wave of loan losses.

A 2.4% decline in private consumption last quarter “and reports of rising urban utility-bill defaults and social security withdrawals point towards stress among retail customers,” according to Fitch Ratings, which estimates a hole of anywhere between $15 billion to $58 billion in government-controlled banks’ capital base under varying degrees of loan losses. That dwarfs the $5.5 billion of new capital New Delhi has promised them. A bigger Band-Aid for banks will mean even unhappier debt investors.

Amid the celebratory noises coming from liquidity-fueled equity markets, it’s worth remembering that Covid-19 hasn’t gone away yet. After almost normalizing in February, economic activity is once again almost 5 percentage points below the pre-pandemic usual, according to the latest Nomura India Business Resumption Index. Consumer sentiment is improving — but only a narrow elite is in a mood to splurge. Just 5% of Indians believe that now is a good time to buy consumer durables, according to Mahesh Vyas at the Center for Monitoring Indian Economy.

This sobering reality is finding an expression in the apprehensions of global debt investors. They have pulled out more than $14 billion from India in the past 12 months even as the local equity market has witnessed $29 billion of net inflows from overseas. The latter may get more attention, but what buoyant stock prices are serving up as optimism about resurgent corporate earnings is weak, watery tea. For more reliable signals, it’s the bond market leaves that are worth reading.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2021 Bloomberg L.P.