(Bloomberg Opinion) -- It seems not even the delta variant of the Covid-19 virus will keep Americans away from Disney World. Now, Walt Disney Co. just needs to work on translating more of that enthusiasm for all things superheroes, princesses and “Star Wars” into streaming subscriptions, particularly in the U.S. where Netflix Inc. still dominates.

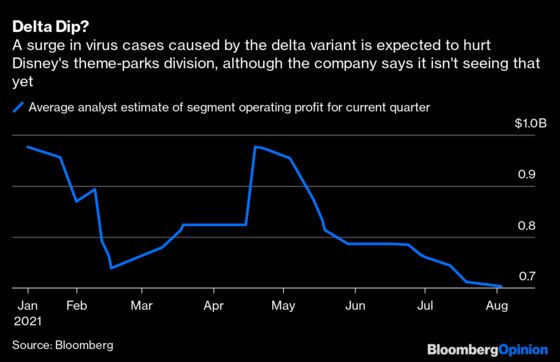

There was some concern heading into Disney’s earnings report Thursday afternoon that the fast-spreading delta variant in the U.S. would trip up the recovery in the company’s theme-park business. As of now, Chief Executive Officer Bob Chapek says that’s not the case. While he has seen some cancellations from large groups and conventions that were supposed to take place at Disney’s resorts, overall park reservations are currently higher than last quarter’s attendance levels. “And those were pretty darn good,” Chapek said on Thursday’s earnings call. Indeed, Disney’s parks, experience and consumer-products division managed to rake in $356 million in operating profit, compared with an almost $2 billion loss a year ago. Across the board, Disney’s results came in better than expected.

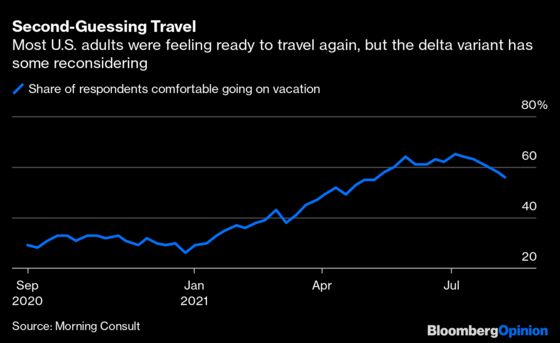

But it’s about more than just Disney’s stock price. The upbeat numbers and outlook bring some relief to investors and consumers more broadly who have become nervous in recent days about the potential disruption the virus may once again bring to our lives. Southwest Airlines Co. warned its own shareholders Wednesday that travelers have begun to cancel flights on account of the delta variant. And school districts are grappling with requiring masks in classrooms and vaccines for teachers. In this week’s Morning Consult survey of 2,200 U.S. adults, 56% said they are comfortable taking a trip right now, down from 65% in early July. And the gap in opinions between younger and older generations has narrowed since the winter, when baby boomers were most hesitant.

It’s hard not to imagine more of those fears around travel and the safety of unvaccinated children hitting Disney, but in the meantime, we’ll have to take Chapek’s word for it. We’ll see if it turns around analysts’ forecasts for the current quarter, which had been lowered substantially in recent weeks heading into Thursday’s earnings report:

Shares of Disney shot up more than 5% in after-hours trading amid surprisingly large subscriber gains at Disney+, although the devil is in the details. The streaming service added more than 12 million subscribers in its quarter ended July 3, bringing the total to 116 million. That’s double the amount it had a year ago. However, a majority of those came from Disney+ Hotstar, a cheaper version of the service in India. Those users now account for an astounding 40% of total Disney+ subscribers. That means behind the impressive growth rate is a trend that’s becoming a drag on profitability. As more Hotstar accounts came into the mix, average revenue per user dropped 10% to $4.16. Excluding Hotstar, it would be $6.12 — and still that trails behind AT&T Inc.’s HBO Max and Netflix, which are higher-priced apps, as well as Disney’s own Hulu.

It’s possible that the Disney+ launch in Japan in October will help improve profit margins. Even though investors are entirely fixated on subscriber growth for now, margins will eventually come into question. Citigroup Inc. analyst Jason Bazinet got it exactly right when he asked Chapek on Thursday’s call about the future of an industry that at its best is still only earning one-fifth of the average revenue per user that traditional pay-TV did. Chapek redirected it back to the growth potential, kicking the can down road, as every streaming company is doing. None can answer this question with any detail: How does streaming make money, and lots of it? After all, these are businesses accustomed to the latter. Hulu is now profitable, but that is largely because it incorporates commercials, an option Disney+ and most of its rivals are avoiding for obvious reasons.

Still, it’s clear what Disney needs to do next to keep shareholders and customers satisfied. Across its three streaming platforms — Disney+, Hulu and ESPN+ — it has about 174 million subscribers, many of which are frustrated by having their favorite programs spread across different apps. They should all be one service, and it seems very likely that 1+1+1 will equal more than 3 in this case. Putting Disney’s family-friendly fare together with its more adult content and sports creates a product with a much wider appeal that can compete more directly with Netflix and HBO Max. Comcast Corp. still owns a piece of Hulu, which is what Chapek may have been referring to when he said Thursday that “there could be certain constraints” limiting Disney’s “ability to do long term what we might feel is ideal.” It’s time to call up Brian Roberts, Comcast’s CEO, and get this sorted out.

The company pulled off a strong quarter in a very bizarre and trying moment in its history. The delta variant remains a threat, but the bigger one is still Netflix if it wants Disney+ to become synonymous with Walt Disney Co.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering the business of entertainment and telecommunications, as well as broader deals. She previously wrote an M&A column for Bloomberg News.

©2021 Bloomberg L.P.