14,889,930,106,680 Reasons to Fear Recession

Economists put the chances of a recession at 15 percent in the U.S. and 18 percent in the euro zone.

(Bloomberg Opinion) -- Traders and investors will be glad to see the back of 2018. It’s been the worst rout since 1901, by Deutsche Bank AG’s reckoning, with almost every asset class delivering losses. These charts illustrate the backdrop to what went wrong this year — and hint at what could go better in 2019.

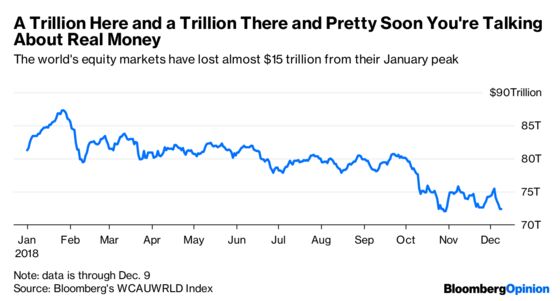

$14,889,930,106,680

That’s how much the total value of companies listed on the world’s stock markets has declined since peaking at $87,289,962,917,450 on Jan 28. In other words, almost $15 trillion has been wiped off the global equity market this year.

The list of potential motivations for the sell-off is long and includes rising geopolitical risks, the prospect of trade wars erupting, the risk that a slowdown in global growth that could degenerate into a worldwide recession, and the evergreen what-goes-up-must-come-down. But might it just be possible that investors start to take the view stocks have fallen far and fast enough to offer value next year?

Talkin’ About a Recession

It’s clear that one of the fundamental worries spooking investors is that the period of coordinated global growth that propelled stock markets higher in recent years is coming to an end.

The R word is increasingly cropping up in news articles. But economists put the chances of a recession in the coming year at 15 percent in the U.S. and 18 percent in the euro zone, according to Bloomberg surveys. Even the Brexit-battered U.K. economy is only at a 20 percent risk, while for Japan the likelihood rises to 30 percent. Perhaps those concerns about a recession are overdone.

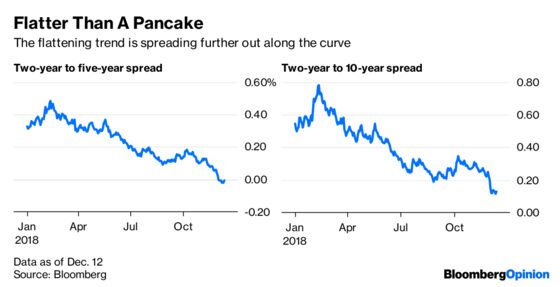

Curving to Inversion

Or perhaps not. One trend was omnipresent in 2018 — the relentless flattening of the yield curve in the U.S.

Yields at the short end of the Treasury market pushed higher with every quarterly increase in the Fed’s benchmark interest rate. Longer-dated bonds danced to a different beat, particularly as the October equity shakeout drove a flight to quality.

An inverted yield curve — when yields on shorter-dated bonds are higher than their longer-dated counterparts — is often seen as an indicator of impending recession. It’s finally happened: Yields on five-years are below those for two-years. A key question for 2019 will be how the feedback loop develops between the Federal Reserve’s policy intentions and the shape of the curve.

Quantitative Tightening

The Fed has been reducing its economic stimulus by not replacing the bonds it bought under its quantitative easing program as they mature.

But this “normalization” is already taking its toll, as the sharp equity market sell-off in October showed. The Fed has a tricky choice to make in 2019 about whether it can persist both with hiking rates and reducing quantitative easing. Is the world ready yet to stand on its own feet without ongoing central bank support?

No Alarms and No Surprises

Economic surprise indexes — which measure actual economic data compared to forecasts — are designed to be portents of the future. And for 2018 they largely did their job. U.S. strength is waning, and Brexit is taking a toll on the U.K. In particular the third-quarter weakness in euro-zone growth, when both Germany and Italy turned negative, was well-flagged from as early as the first quarter.

For 2019 there is a more neutral outlook, but it is interesting that the U.S. economic data is much more evenly balanced in terms of expectations. Europe continues to be the worst performer — quite something considering the predicament the U.K. is in.

Europe Stumbles

Europe has seen growth falter this year, with Italy’s political crisis and Germany’s diesel vehicle emissions scandal taking their toll.

Italy’s third-quarter growth was revised to -0.1 percent, beating only Germany. The prospects for 2019 are none-too-rosy, bar the notable exception of Spain, as momentum has evaporated. Europe remains in the sick bay of the developed world — just as the European Central Bank prepares to remove its monetary stimulus to the economy.

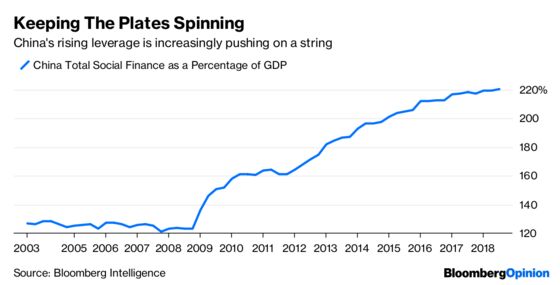

Relying on China

China came to the global economy’s rescue in the wake of the financial crisis, but it is starting to pay the price for increasing its debt to create additional GDP growth. Total social financing as a percentage of gross domestic product — a broad measure of credit creation — is flat-lining. Adding extra debt to boost the economy is becoming a less effective measure. It’s not just the threat of a trade war with America that has pushed Chinese equities down by 20 percent in 2018.

China faces the classic emerging-market middle-income trap where growth fueled by credit runs out of road. This debt bubble will not be easily fixed.

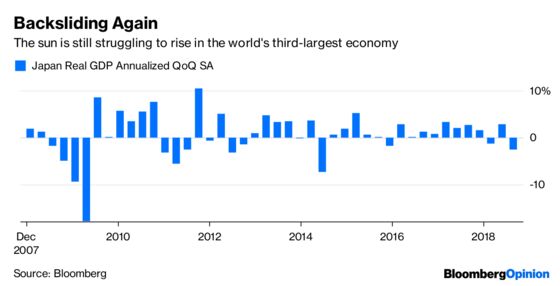

Finding Reverse Again

Japanese Prime Minister Shinzo Abe’s famous three economic arrows are failing to hit their mark. Debt that stands in excess of 250 percent of GDP is hampering all efforts to resuscitate inflation and sustainable growth in the world’s third-largest economy. Third-quarter GDP contracted 2.5 percent on an annualized basis, the worst performance for four years.

Tokyo might be hosting the Olympics in 2020, but there is little benefit flowing through so far. Japan, like the rest of the once dominant Asian export powerhouses, is just as beholden to the outcome of the trade war with Trump as China is.

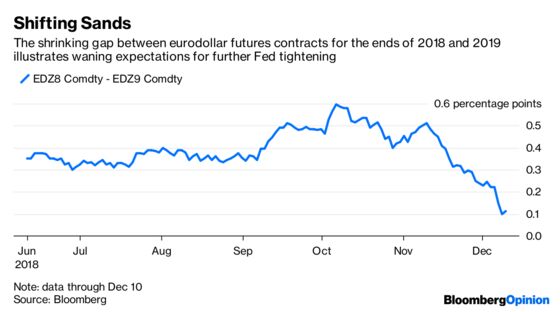

Hunting for Neutral

Until very recently, many economists were anticipating at least four more rate increases from the Fed next year at a pace of one per quarter. While the futures market still suggests a Dec. 19 hike is a done deal, the outlook for monetary policy in 2019 has shifted significantly in recent weeks.

Goldman Sachs Group Inc. has trimmed its forecast for number of potential Fed rate increases in 2019; billionaire fund manager Paul Tudor Jones said earlier this month that he’s not expecting any additional tightening from the U.S. central bank next year. A halt to the hikes might prove as pleasing to financial markets as to President Donald Trump.

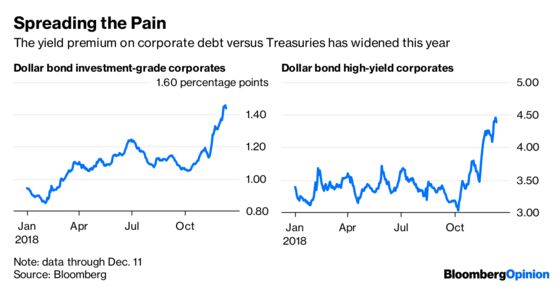

Credit Squeeze

Companies with dollar bonds have seen their borrowing costs soar relative to those of the U.S. government as the Fed has driven its benchmark interest rate higher this year. Investors have seen a corresponding slump in the value of the corporate debt they own.

Any slowdown in the ascent of U.S. borrowing costs as the Fed pauses for breath should give succor to corporate bonds — provided it isn’t accompanied by a rise in defaults.

Other People’s Money

It’s been a terrible year for the stocks of firms that manage other people’s money for a living.

Fund managers tend to invest in each other’s shares. And you’d expect them to have better-than-average insight into the business prospects of their peers. So watch for an inflection point in asset management stocks — it might be a sign of a turning point for the wider market.

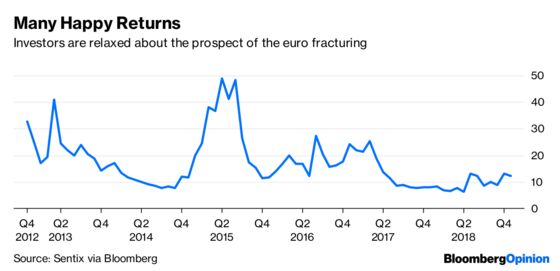

Happy Birthday to the Euro

The common European currency celebrates its 20th birthday at the start of January. During the two decades of its existence, rumors of the euro’s demise have been proven to be greatly exaggerated.

The European debt crisis at the beginning of this decade posed an existential threat to the euro’s well-being. The currency survived. At several points in the past few years, Greece seemed on the verge of either quitting or being ousted from the project. Its membership survived. And Italy’s election of a populist government earlier this year raised the prospect of a founding member threatening to leave if it wasn’t allowed to break the bloc’s budget rules. Still, the euro survives.

In fact, as the chart above shows, investors are close to the most relaxed they’ve been about the euro fracturing in more than five years based on the Sentix Euro Break-Up Index, a monthly gauge of investor concern about the threat. So let’s end by wishing the euro many happy returns.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.