Hyundai’s Riding High on Hope Alone

The South Korean carmaker reported that operating profit fell 35 percent in the fourth quarter from a year earlier.

(Bloomberg Opinion) -- Hyundai Motor Co. investors are riding high on nothing but hope.

The South Korean carmaker reported Thursday that operating profit fell 35 percent in the fourth quarter from a year earlier. The stock initially fell as much as 3.5 percent, though the results shouldn’t really have been a surprise.

Hyundai Motor shares have rallied almost 10 percent this year after a series of announcements that signaled an overhaul, covering management reshuffles and a stream of futuristic technology investments. Yet a commitment to bring back returns for investors or profit growth has been missing. The shares lost almost a quarter of their value in 2018.

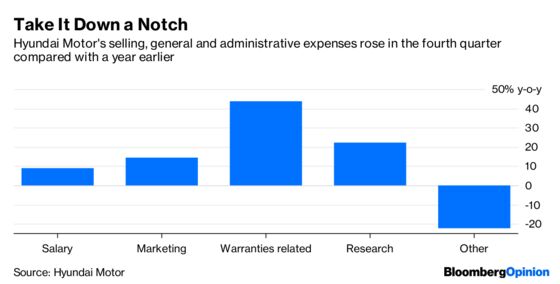

The company hasn’t mentioned deep surgical changes such as culling unproductive facilities, cutting costs or streamlining its business. In fact, an increase in expenses was to blame for the poor fourth-quarter earnings. Profitability has failed to show signs of a recovery, with Hyundai’s net margin shrinking in the last three months of the year.

Instead, it’s stuck to cosmetic adjustments. Hyundai will expand production in Vietnam by the second half of next year from the 60,000 or so cars currently made there, the company said Thursday. The carmaker is also building a plant in Indonesia and said it was strengthening sales plans in India and Southeast Asia. Hyundai could get a boost from those markets, but it won’t be enough to underpin a recovery of the core business anytime soon.

Hyundai’s December sales ticked up in the U.S. and South Korea, but its market share was little changed. For the year, sales fell globally. In response, Hyundai is holding out more hope: It sees sales in China rising 8.8 percent this year, after an 8.6 percent decline in 2018. That’s well above estimates of 3 percent to 4 percent growth for the rest of the industry.

China’s auto sales dropped for the first time in decades last year, and the market faces severe hurdles in 2019. Predicting a complete reversal in such a depressed environment risks leaving Hyundai looking foolish.

Meanwhile, the automaker is still dealing with the recall of 168,000 cars in the U.S. because of faulty fuel pipes, and must contend with a campaign by activist investor Paul Singer’s Elliott Management Corp.

The path to Hyundai’s recovery should begin with prudence. Instead, it looks to be taking investors for a ride.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.