Hugo Boss Can't Compete When Luxury Is All About Handbags

(Bloomberg Opinion) -- Just 24 hours after LVMH reported knockout sales growth, Hugo Boss AG has provided a sober reminder that the luxury sector’s spoils will not be spread evenly.

The maker of smart suits on Thursday issued a warning on full-year sales and profits, the second time it’s pared its outlook in two months, blaming the problems in Hong Kong and ongoing weakness in the U.S. The shares fell as much as 14% to the lowest level in nine years.

Chief Executive Officer Mark Langer made a mistake by being too optimistic about the outlook. What’s far less clear now is whether his plan of boosting online sales, focusing on a slimmed-down portfolio of brands and embracing faster fashion is enough to weather the shocks on the horizon on top of the enduring shift toward casual office attire.

Hugo Boss gets just 2-3% of its sales from Hong Kong, compared with about 6-7% in China, so it should have been more cushioned. But it struggled to offset a 50% plunge in third-quarter sales in Hong Kong, which remains a popular shopping destination for mainland Chinese. By contrast, LVMH said its Hong Kong sales fell 40% in August and September, but much of that was recouped elsewhere.

Workwear, unlike handbags, isn’t the sort of thing you naturally buy on your holidays, so lost sales of suits, say because stores are closed, are less likely to be transferred to another shopping location.

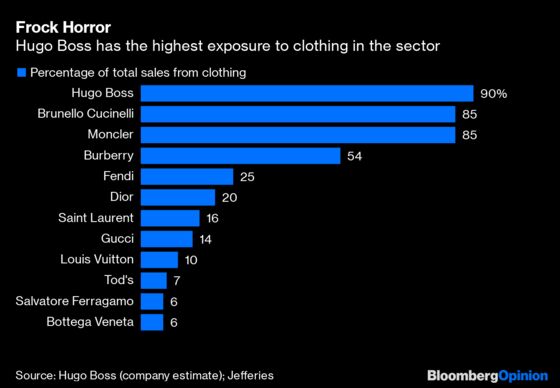

That highlights one of Boss’s two big weaknesses: It generates 90% of its sales from clothing. These are proving more vulnerable than leather goods, which remain highly desirable, particularly for middle class and younger Chinese consumers.

The other is that Boss also operates in the upper premium segment of the market, rather than super-luxury part. The very wealthy tend to be more resilient spenders than the merely comfortably off who have greater cause to fear political and economic uncertainty. Hugo Boss’s professional customers are more likely to fret about instability, which seems to be popping up everywhere, as well as the possibility of a U.S downturn next year.

Boss blamed its last downgrade to forecasts, in early August, on problems in the U.S. It generates about 15% of its sales in that market, where it has been hurt by heavy discounting by rivals and fewer tourists, given the strength of the dollar. With U.S. consumer confidence posting the biggest drop since the start of the year in September, that doesn’t bode well for a quick recovery in this crucial market.

All this raises serious questions about the ambitious targets that Langer set less than a year ago. Expanding sales growth from 4% in 2018 to 5-7% by 2022 always looked ambitious. Now the trajectory looks even more challenging, given that the company’s new forecast is for sales growth in the low single digits in 2019. Lifting the margin to 15% of earnings before interest and tax looks equally unrealistic. Analysts at RBC estimate the EBIT margin at 11.7% in 2019.

The shares have fallen 37% over the past year, and trade on a forward price-earnings ratio of just 10 times, about half the other clothing-focused luxury groups, indicating that investors have little faith in the group meeting its medium-term goals.

Langer’s strategy of moving to just two brands – Boss, catering to core customers, and Hugo for the younger crowd – looks sensible. Bolstering online sales, getting the latest looks into stores more quickly and increasing personalization are logical moves, too. But all of this is increasingly being undermined by weak markets and consumers continuing to turn off clothing.

Like an ill-fitting suit, Langer’s aspirations need some careful alterations.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.