Why a Piece of Chocolate Costs More Than a Porsche Taycan

Lindt announced plans to buy back 750 million Swiss francs of equity, edging the shares closer to the record 93,800 franc level.

(Bloomberg Opinion) -- If you were thinking of companies that might want to increase the value of their shares by buying back stock, Lindt & Sprungli AG would likely come near the bottom of the list.

Primary shares in the Swiss chocolate-maker closed at 81,600 Swiss francs ($87,650) apiece March 1. That's roughly enough money to buy a brand-new electric Porsche Taycan, or a five-bedroom house with a vineyard in Portugal. The next day, Lindt announced plans to buy back 750 million Swiss francs of equity, edging the shares closer to the record 93,800 franc level they peaked at last February.

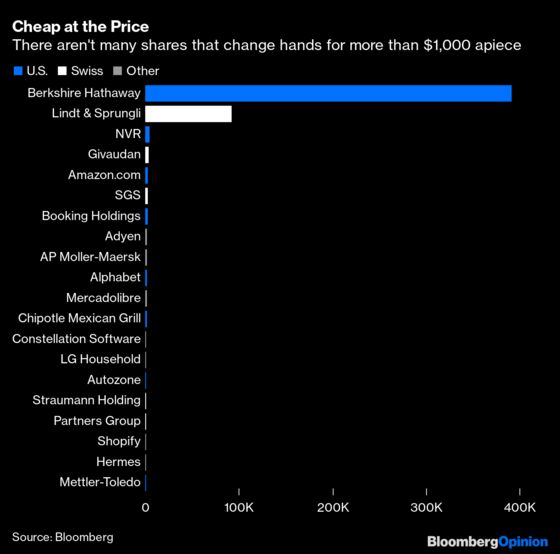

It’s not often an investor will be asked to part with so much to buy a single share. Companies with stock prices that are expensive in absolute terms — as opposed to the usual market meaning of the term, “highly priced relative to forecast earnings” — are rare as hen’s teeth.

Even if you set a relatively low floor, there are only a handful of blue-chip companies whose shares come in at more than $1,000 apiece. A preponderance of those are U.S. tech businesses, such as Amazon.com Inc. and Alphabet Inc., which appear to treat their share prices as a Buffett-style status competition; Japanese real-estate investment trusts, which aren’t much traded; and yet more Swiss companies, including Lindt’s competitor Barry Callebaut AG.

There’s also a twilight zone of equities that are not dissimilar, in their way, to low-priced penny stocks. Most are just the remnants of free-floating stock in companies that are otherwise closely held by their core investors, trading off-exchange in volumes that rarely exceed 1,000 shares a day.

If you want to buy a stake in Berlin’s zoo, for instance, there are 3,000 shares out there, which can be had for 8,350 euros ($9,950) each, if you can find a broker. Equity in the Hotel Majestic, a traditional film star hangout in Cannes, is notionally available for 3,500 euros. You can even get a slice of the Neue Zurcher Zeitung newspaper for 5,250 Swiss francs. Shares in the Belgian or Swiss central banks are available at similar prices.

Lindt, like Berkshire Hathaway, has a separate class of stock so that small-time investors can play. This being Switzerland rather than Nebraska, buying a ticket for the cheap seats would still have set you back 8,115 Swiss francs at Thursday’s close.

If you’re tempted to ask why any company would want shares so expensive that the average retail investor would have to re-mortgage to buy one, the better question might be, why wouldn’t they?

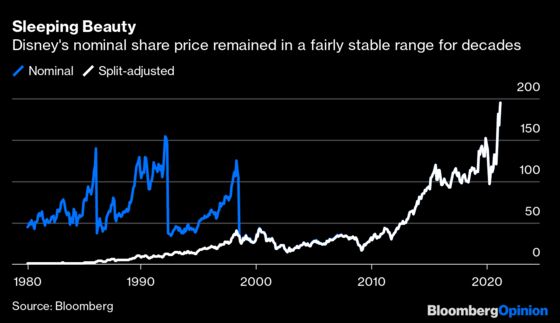

After all, it takes substantial effort to maintain static pricing ranges for shares whose investment case is based upon the idea of continually escalating earnings. Walt Disney Co.’s $11.05 billion of net income in 2019 was about 80 times the $135 million it reported in 1980. Its year-end share price, on the other hand, was less than three times the $51.25 at the end of that year, thanks to an array of stock splits initiated every time the price moved substantially above $100 a share.

All that comes at a cost. Stock splits are major corporate events that entail paying substantial sums to investment banks. Many brokers and exchanges charge fees on a per-share basis, too, so shareholders of companies with a large volume of stock on issue can end up losing money on ticket-clipping. One 2009 study led by then-University of Wisconsin professor William Weld estimated that General Electric Co. shareholders could be paying out $100 million a year in excess trading commissions as a result of the company’s long history of splits.

The traditional explanation for this has been that corporate boards are doing something similar to the managers of dollar stores. If you want a bit of pep in your stock, institutional investors who don’t think twice about dropping four figures on a single share aren’t much use. Their buying behavior will be guided by the needs of a balanced portfolio and stolid analyses of earnings forecasts: hardly the sort of thing to put rocket emojis under your shares. Lower the price to a level where you can get the punters in, however, and valuations — and executives’ share-linked long-term incentive plans — might soar.

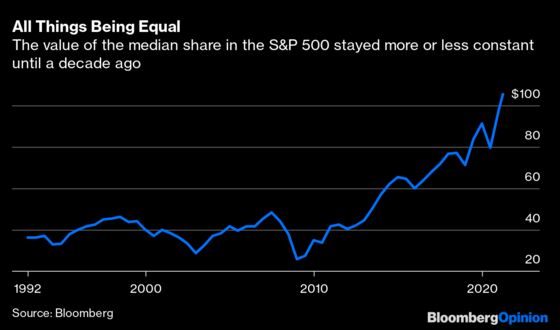

There’s evidence that this way of thinking is fading. Through much of the past century, share splits have clustered U.S. average stock prices around a $20-$50 range. The price of the median share in the S&P 500 started rising sharply about 10 years ago, and is now worth $105.50. If size no longer matters in the stock market, Lindt may have chosen a good moment to get bigger.

Based on the assessed land-tax value of his house. Such assessments often under-value expensive properties, and if it ever actually went to market Buffett's house would probably cost at least as much as a lunch date with him.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.