Housing Might Rescue the Economy From Trump’s Trade War

(Bloomberg Opinion) -- Manufacturing data released Tuesday made two things clear: The Federal Reserve might be powerless to prevent the negative effects of the trade war from hurting economic growth, but it still has the juice to boost the housing market.

The ISM Manufacturing Index report showed that industrial activity in the U.S. plunged in September, the sixth straight monthly decline, to the lowest since the Great Recession ended in June 2009. But the silver lining is that the Fed's efforts are showing up in recent housing data, including Tuesday's construction spending report, with activity continuing to perk up after several sluggish quarters.

An acceleration in housing while manufacturing contracts is unusual, with the closest comparable period being 2001, when the technology bubble was going bust and the Fed was rapidly cutting interest rates. In contrast with that time, today's technology sector remains relatively sound, even if some recent initial public offerings have struggled. So there's a strong case to be made that renewed housing growth and stable consumption will offset any drag from the trade war, even if there are pockets of weakness in the Midwest. In other words, the Fed's proactive rate cuts may have been enough to stave off a broader economic decline.

The slowdown in manufacturing activity signaled by the ISM report is consistent with trends seen around the world, with Euro-area manufacturing in its biggest slump since 2012. Since the source of the U.S. slump is a function of the global trading environment and rising tariffs, any improvement in domestic manufacturing probably will depend on a cessation in trade hostilities.

Still, the Fed has to be concerned about the deterioration in industrial activity, regardless of international conditions. The question is, What can it do? Respondents in the ISM report cited slowing global trading activity and tariffs, not interest rates or the availability of credit, as the leading causes of the contraction in manufacturing activity. Yet one way in which cutting interest rates might help, as President Donald Trump has tweeted, is with the dollar, which remains at elevated levels. Lower rates should weaken the dollar, making U.S. manufactured goods more competitive overseas. The risk, of course, is that the Fed might not be able to reverse course quickly enough if a halt in the trade war and an improvement in global growth leads to unexpected inflation pressures.

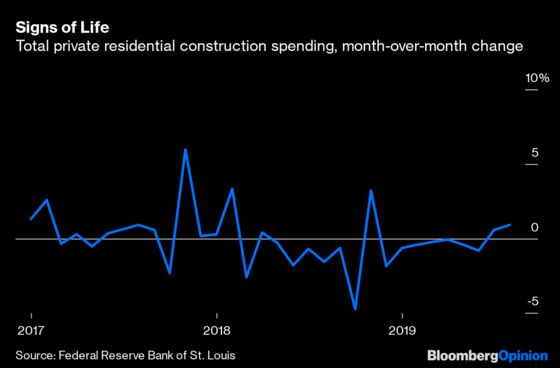

Fortunately for the Fed, its dovish stance this year has bolstered the housing market. This improvement has been underway for much of the year but is only now being reflected in the vast majority of housing market indicators. The first was the National Association of Home Builders Market Index, which had fallen sharply last November and December in response to higher interest rates and a declining stock market. It has improved steadily throughout 2019 -- in part due to the fall in mortgage rates -- and has now recovered all of the ground it lost at the end of 2018. Mortgage-purchase applications, which became sluggish in response to last year's rise in rates, are now growing at a healthy pace. New home sales rose this summer and are reaching new highs for this economic expansion. August was the best month for building permits -- a reliable leading indicator of housing starts -- in more than a decade. And private residential construction spending, which was contracting during most of 2018 and the first half of 2019, has now shown two consecutive months of growth for the first time in a year and a half:

Investors have bought into the improvement, with the iShares U.S. Home Construction ETF up about 50% since its low in late December.

This year may end up be a more muted version of 2001, when the U.S. economy spent eight months in recession as technology stocks were cratering and corporate America slashed capital spending. The Fed responded then by lowering the fed funds rate from 6.50% to 1.75%. In response to lower rates, homebuilder stocks rallied despite the domestic recession, anticipating the housing boom to come. In 2019, instead of a nasty tech recession, we've have a mild trade and manufacturing recession that has sapped, but not crippled, U.S. economic growth. In response to these risks, the Fed probably will end up cutting interest rates two or three times this year instead of the multiple rate increases it anticipated at the beginning of the year.

The Fed will understandably be concerned if manufacturing weakens further. But unlike in 2001, this time around housing might have strengthened enough to protect the rest of the economy.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He is a portfolio manager for New River Investments in Atlanta and has been a contributor to the Atlantic and Business Insider.

©2019 Bloomberg L.P.