Hong Kong Brokers Are Already Reading From Beijing’s Script

(Bloomberg Opinion) -- The national security law China imposed on Hong Kong this week will damage civil liberties with long jail sentences and grant immunity to Chinese agents working in the territory. For investors who depend on the city as a financial center, though, there may be an extra sting in the tail.

The law could increase self-censorship by Hong Kong’s analysts and economists, and damage the credibility of research reports, the Financial Times reported this week. The need to maintain relationships with mainland clients has influenced coverage in the past, but many fear the new law will exacerbate this trend.

It’s a bit late to be worrying about that, though. Self-censorship isn’t just a matter of avoiding gratuitous digs and glib phrases. If you look at the ratings given by equity analysts in recent years, it seems to include portraying companies with strong mainland connections as better investments than they actually are.

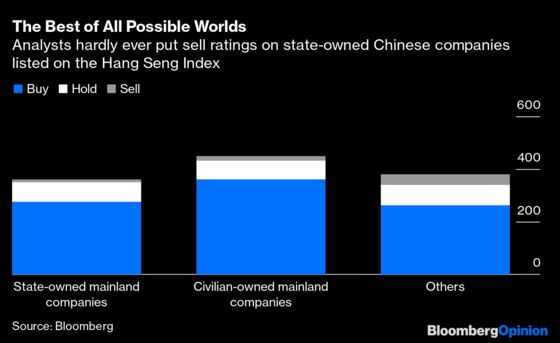

Take the 50 companies on the Hang Seng Index. You can easily break them into three groups: 15 Chinese state-owned enterprises, or SOEs, such as Bank of China Ltd. and PetroChina Ltd.; 13 civilian-controlled mainland Chinese businesses, or COEs, such as Tencent Ltd. and Sino Biopharmaceutical Ltd.; and 22 other, mostly locally controlled stocks, such as HSBC Holdings Plc, CK Hutchison Holdings Ltd. and AIA Group Ltd .

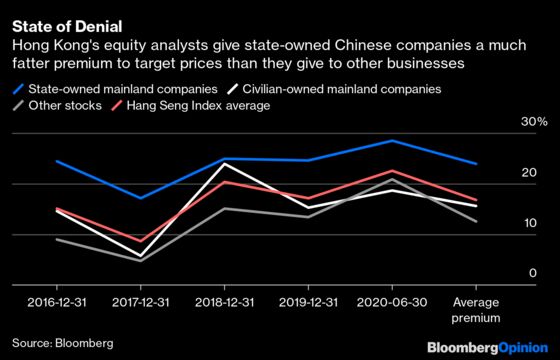

Then look at the extent to which analysts’ consensus target prices have exceeded actual stock prices in recent years. SOEs get the most favorable treatment, with target prices exceeding actual prices by an average of 24% since the start of 2016, compared to 16% for the COEs and 13% for non-mainland companies.

It’s not just in Hong Kong that brokers’ target prices tend to run higher than the actual market — there’s a reason they’re called sell-side analysts. China is still an emerging market, too, so it’s not impossible that its stocks simply have more upside than those operating out of a mature economy such as Hong Kong.

So perhaps the reason state-owned enterprises get a target price premium over local companies is simply that they’re better investments that will deliver higher returns to investors?

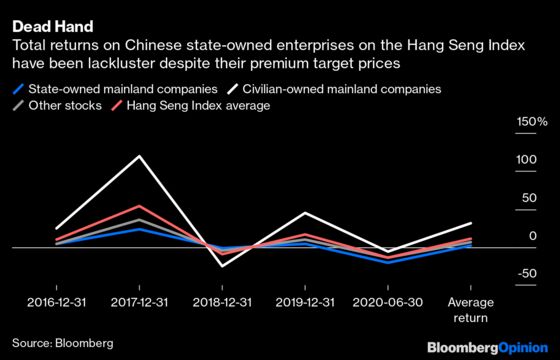

If only. Thanks to booming tech and biotech stocks and the huge run-up in prices during 2017, civilian-owned Chinese companies did achieve pretty stunning average total returns of 31% over the past four-and-a-half years. SOEs, however, averaged a measly 1.9%, far less than the 6.1% achieved by the non-mainland stocks.

It’s not totally irrational that possessing a wealthy patron should be seen as an advantage for some investments. The Chinese state tends to put its thumb heavily on the scales in favor of its own organs, with diminishing benefits the further you get from the commanding heights of the economy, as my colleague Shuli Ren has written.

In particular, it’s logical for credit analysts to give state-owned enterprises a better rating than those that can’t count on the backing of the Chinese government to bail them out. Even there, you’ve not been paying attention if you think the interests of private bondholders are going to be treated equally with those of better-connected investors.

Still, when looking at the equity market, the proof should be in the pudding. If analysts predict a stock will consistently outperform — as they tend to do in relation to SOEs — then it should do that. If not, they’re either bad at their jobs or misleading their clients.

There are many things to worry about in Hong Kong’s new national security law. The integrity of equity research is probably not one of them. Sell-side brokers themselves gave that away long ago.

We've equal-weighted each of these baskets of stocks so that a few stocks with huge market caps like Tencent, HSBC or China Construction Bank don't skew the overall result.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2020 Bloomberg L.P.