(Bloomberg Opinion) -- Home Depot Inc.’s DIY renovation project has hit some snags. But its stumble isn’t necessarily a warning sign about either consumer spending or the housing market.

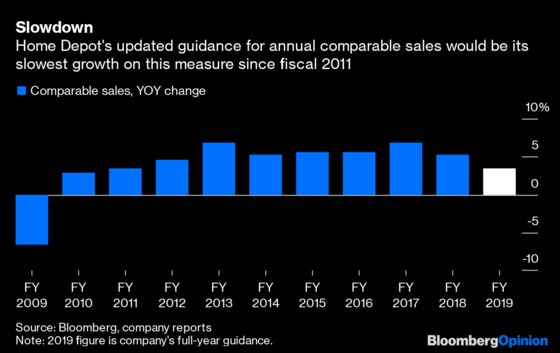

The big-box giant reported Tuesday that comparable sales rose 3.6% from a year earlier in the third quarter. That’s not exactly a weak increase, but it was well below analysts’ expectations. The growth was slow enough that the retailer cut its full-year guidance on this measure, sending shares down more than 5% in morning trading.

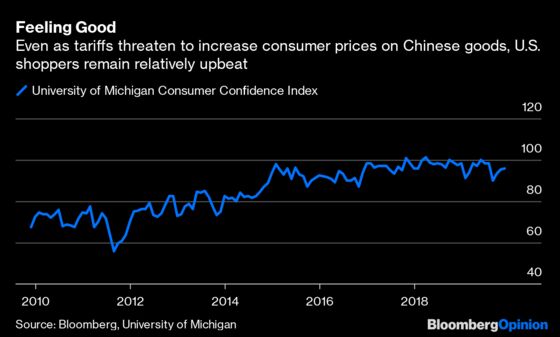

On a conference call with investors, Home Depot executives didn’t suggest the results reflected any softening in the larger economy. The housing market looked “healthy and stable,” they said, and noted that growth in big-ticket transactions, those over $1,000, was strong — a sign that shoppers are spending with confidence.

That sunny portrait of the consumer is similar to what Walmart Inc. described last week when delivering robust third-quarter results. And it is consistent with other readings of consumer sentiment.

Instead, Home Depot said it suffered because some elements of its long-term strategic plan are taking longer than expected to benefit the company’s results. In particular, executives said it was proving challenging to upgrade its technology systems to better support their website for home-improvement professionals.

The company had already slashed its sales guidance once this year, but that was largely because of factors beyond its control, including tariffs on goods coming to the U.S. from China and lumber price deflation. Today’s guidance cut is noteworthy because it suggests that even Home Depot, a generally well-run chain that has essentially been untouched by the retail apocalypse, is finding the shift to a more digital-centric business to be a bumpy one.

These results should hardly leave anyone in a state of alarm about Home Depot’s future. Many mature retailers can only dream of 3.6% comparable sales growth at a time when Amazon.com Inc. is encroaching on their turf. Home Depot saw comparable sales growth in all U.S. geographic divisions and across all product categories except lumber and electrical — indicators of balanced, diversified strength. In addition, Home Depot has been conservative about opening new stores for years now, a prudent decision many of its industry counterparts have not been smart enough to imitate.

The downside surprise at Home Depot also puts sharper focus on the quarterly results of Lowe’s Cos., which are scheduled for release Wednesday morning. Under CEO Marvin Ellison, Lowe’s is looking to change the perception that is an also-ran to Home Depot. A strong showing in a quarter when Home Depot disappointed could help Ellison do that.

Whatever happens with its chief rival tomorrow, however, Home Depot’s results are a reminder that digital transformations in retail are extremely hard to execute.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.