(Bloomberg Opinion) -- Not all high-yield bonds are on a hot streak.

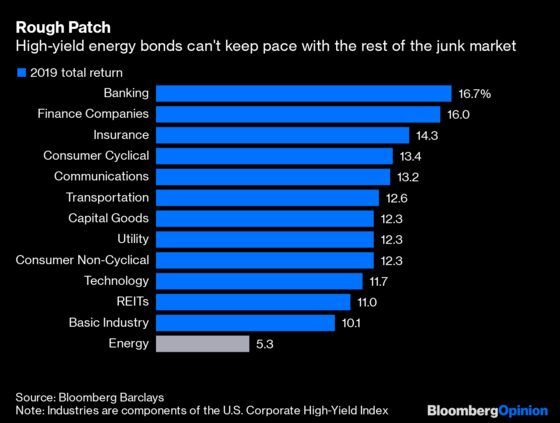

On its face, the U.S. junk-bond market appears as if it can do no wrong. The average yield on the Bloomberg Barclays U.S. Corporate High Yield Index dropped to a 20-month low of 5.58% on Wednesday. Investors poured $3.3 billion into junk-debt funds this week, the most since February. Overall, high-yield securities have gained 11.7% in 2019 and delivered positive returns in all but one month as the Federal Reserve and other central banks lower interest rates to keep the global economic expansion on track.

Anyone invested in high-yield energy debt, however, has been on a much different ride in 2019.

Those bonds have earned just 5.3% this year, worse than every other high-yield industry group tracked by Bloomberg Barclays indexes. They’ve especially sputtered in recent months, losing 1.1% in July and then 2.5% in August. It’s not hard to figure out why — oil prices stagnated in July and then dropped 6% last month. Energy companies, and especially those with weaker credit profiles, depend on higher oil prices to stay afloat and make payments to creditors.

So when oil surged on Monday by the most on record after an attack on Saudi Arabia — which my Bloomberg Opinion colleague Liam Denning described as a strike at oil’s future — it felt inevitable that this beaten down corner of the otherwise thriving junk-debt market would get a lift. It didn’t disappoint: The Bloomberg Barclays High Yield Energy Index jumped 1.5% in a day, the biggest increase since early January, with spreads tightening by a remarkable 38 basis points. The high-yield market excluding energy, by contrast, was unchanged.

That spike in the price of oil, of course, didn’t last. It pared almost half of Monday’s gain on Tuesday alone. At about $58 a barrel, the price of crude is just a few dollars higher than it was at this time last week and back below its six-month average. High-yield energy bonds, too, gave up a chunk of their gains.

On the one hand, it’s understandable that the depressed market for speculative-grade energy bonds reacted the way it did to the attack on Saudi Arabia’s production facility. It accounts for about 5% of global crude production, and when it looked as if it would take a while for the plant to get back up to speed, naturally the supply-demand driven oil market didn’t wait around to react. It’s also hard to put firm odds on a renewed conflict in the Middle East, and even harder to price in the implications.

And yet, there’s also this:

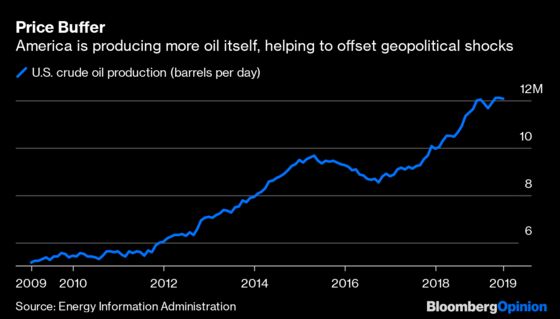

President Trump has a point. The U.S. has been steadily producing more crude oil since he took office, according to data from the Department of Energy’s Energy Information Administration. As a headline Thursday in the Washington Post put it, “Saudi Arabia’s Oil Troubles Don’t Rattle the U.S. as They Used To.”

Yes, making that claim after observing oil prices this week doesn’t mean quite as much. Still, there were questions about how long a shock could last almost immediately after the attack. “How sustainable is this rally?” asked Bloomberg Intelligence credit analyst Spencer Cutter. “If prices fall back below $55 again,” he said, “then the bonds may give back all of their gains.”

The fact that this was such an open concern, and yet some distressed energy bonds from California Resources Corp. nevertheless jumped from 55 cents on the dollar to 63 cents in a day of heavy trading, is surprising. For one, it’s not particularly easy to just hop into a position in that kind of speculative-grade debt, which has a CCC+ composite rating. Some large mutual funds that already own the securities possibly took the opportunity to add to their holdings. As Cutter said, “some creditors who expected to take maybe an 80% loss may now take a 60% loss.”

For those who ended up buying California Resources debt, things only became worse on Thursday, and not just because of stagnant crude prices. The oil and natural gas producer’s bonds plunged to as low as 48 cents on the dollar after Debtwire reported that it met with restructuring advisers.

Even without factoring in that news, expecting such a fundamental shift in recovery rates earlier this week after a one-day record surge in oil prices was shortsighted. Denning pointed out last month a crucial shift in the way energy stocks are pricing in oil’s decline relative to recent history. Usually, valuation multiples would fall when oil prices rose, effectively pricing in a cyclical reversion. Multiples would then climb when oil dropped. But in the past year, as crude slumped, so did those multiples.

Investors in high-yield energy bonds ought to be similarly dubious about long-term pricing and what it would take for oil to stay at a level that allows companies to generate free cash flow and make good on their debts. As Moody’s Investors Service noted in a recent report, exploration and production companies accounted for three of the seven largest defaults in the second quarter: Sable Permian Resources, Legacy Reserves LP and Jones Energy Holdings. E&P remains the only segment of the junk-bond market tracked by Moody’s with a “liquidity stress indicator” that’s flashing “a more worrisome signal of default risk.” That is to say, there’s likely more shakeout to come.

The temptation to wade into energy bonds is obvious. They offer an average yield of 8.15%, almost 300 basis points more than high-yield debt excluding energy. Correctly identifying a turning point for oil-dependent companies could make a fixed-income portfolio manager’s entire year. But sometimes securities are cheap for a reason.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.