(Bloomberg Opinion) -- Just wait until the next stock market meltdown. Then you’ll see the value of a seasoned stock picker.

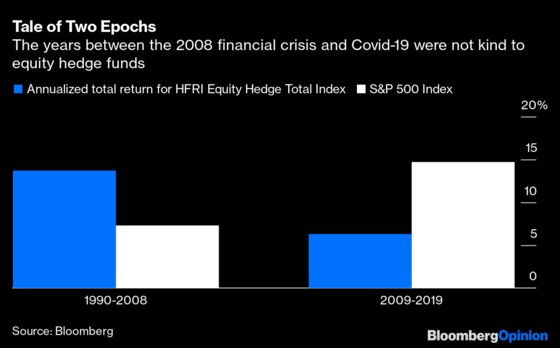

That was the refrain from equity hedge fund managers between the 2008 financial crisis and the arrival of Covid-19, the second-longest stretch without a bear market on record. The S&P 500 Index quintupled in value during that period, and stock pickers struggled to keep up, particularly long-short hedge funds that simultaneously bet on some stocks (long) and against others (short). When a rising market lifts all stocks, long-short managers have little hope of winning.

And they didn’t. The HFRI Equity Hedge Total Index, a basket of long-short hedge funds, trailed the S&P 500 by a demoralizing 8.4 percentage points a year from 2009 to 2019, including dividends. It was a stunning reversal from the heady golden age that preceded it, when hedge funds appeared to deftly navigate the dot-com and housing bubbles and their ensuing busts. From inception in 1990 through 2008, the HFRI index beat the S&P 500 by 6.4 percentage points a year.

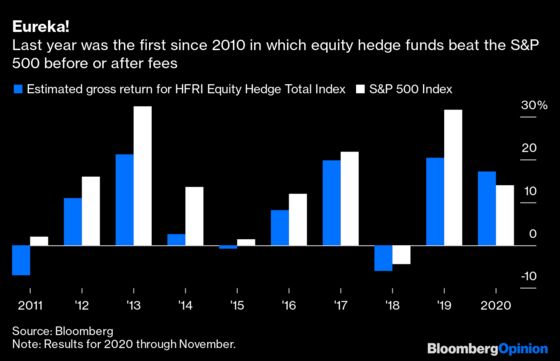

The mayhem Covid-19 unleashed on markets last year was the long-awaited opening equity hedge funds had been carping about, and they seized on it. Five of the seven best-performing hedge funds last year were long-short equity, according to results compiled by Bloomberg. By all accounts, it was a standout year for stock pickers relative to other hedge fund strategies.

The spoils were shared broadly. The HFRI index was up 11.6% through November, nearly double its average annual return during the years between the financial crisis and coronavirus. And that’s net of hedge funds’ hefty fees, customarily a 2% management fee and 20% of profits. Gross of those fees, the HFRI index most likely generated a return closer to 17%, which is 3 percentage points better than the S&P 500. It’s the first time equity hedge funds beat the market, before or after fees, in any calendar year since 2010.

So how did they do it? It’s hard to know for sure because hedge funds are famously tight-lipped, but there are some clues. It’s probably safe to assume their shorts didn’t help much, and may have even cost them, because most stocks have recovered and even surpassed their pre-Covid level. That means the boost must have come from the stocks they wagered would rise in value.

The result is a mishmash of stocks, mostly technology and communications companies, with a sky-high valuation, lean profits and a dollop of debt for good measure. According to numbers compiled by Bloomberg, the VIP index boasts a price-to-earnings ratio of 67, more than double that of the S&P 500; a return on equity of just 3.6%, which is a third of the S&P 500; and a debt-to-equity ratio of 172%, or a third higher than the S&P 500.

It’s a strategy that was well trafficked in 2020: Buy the hot stocks, never mind what’s behind the ticker. And it paid off big.

In fact, the VIP index moved in close step with the coveted Nasdaq 100 Index last year, two-thirds of which is allocated to technology and communications. Dynamic Beta, a New York-based specialist in hedge fund replication, looked at the rolling 20-day correlation between the daily price changes of the VIP index and the Nasdaq 100 and found that it was well above 0.9 for much of the year, a near-perfect relationship. It was no surprise, then, that the VIP index returned an enviable 37% last year through November, nearly matching the Nasdaq 100 over the same time. (A correlation of 1 implies that two variables move perfectly in the same direction, whereas a correlation of negative 1 implies that two variables move perfectly in the opposite direction.)

But the hedgies are no fools. They know that no stock or sector stays hot forever, and they already appear to be moving on. The VIP index shaved roughly 20% from its allocation to the highflying technology sector in the fourth quarter and doubled its exposure to long-suffering financials. Those moves also showed up in the 20-day correlation between the VIP index and the Nasdaq 100, which dipped closer to 0.7 recently.

Still, it would be a bold break from their secret for success in 2020. Equity hedge funds didn’t win last year by outsmarting the market. They simply followed the herd.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2021 Bloomberg L.P.