(Bloomberg Opinion) -- It has been an absolutely awful year for some of the world’s most well-regarded macro hedge funds.

First, Bloomberg News revealed in early August that Alphadyne Asset Management, which has never had a down year since starting in 2006, was facing losses of about $1.5 billion through the first seven months of 2021 after being caught in wrong-way bets on rising interest rates. Element Capital Management, the $15 billion firm considered with Alphadyne to be among the best in the world at trading rates, tumbled 7% in February as global bond yields jumped and curves steepened. Element, led by its billionaire founder Jeffrey Talpins, began mounting a comeback more recently by simply avoiding wagers on interest rates.

Yet somehow their struggles pale in comparison to those of billionaire Chris Rokos. Bloomberg News’s Nishant Kumar broke news Wednesday that Rokos’s hedge fund declined a stunning 11% this month, bringing losses for the year to 20%. That would mark its worst year ever — and is particularly painful for Rokos because he concentrated all decision-making in his own hands in 2019.

How could these macro hedge fund superstars get burned so badly? All signs point to the wild fluctuations in yield curves across the globe as central bankers begin to react to persistently elevated inflation.

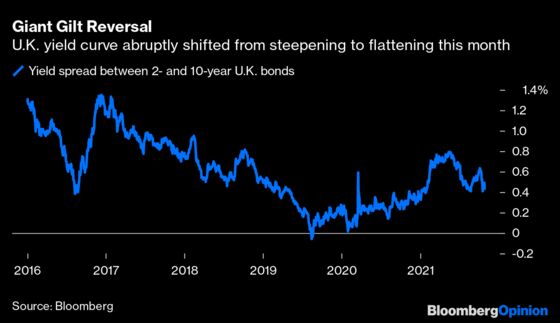

For London-based Rokos, just consider U.K. gilts. Heading into the start of this month, the yield spread between two-year and 10-year U.K. debt was steepening at the quickest pace since March. After peaking at 63 basis points on Oct. 5, the curve flattened sharply by more than 21 basis points in less than two weeks as traders began ramping up bets that the Bank of England would increase interest rates this year. Aside from the bout of volatility in March and April 2020, that sort of move hasn’t happened since early 2018.

The Rokos Global Macro fund slumped 5% in June, when this same curve flattened 10 basis points. While there’s no indication that Rokos is betting on U.K. rates or these maturities specifically, it serves as a useful proxy to potentially understand the magnitude of losses that big-swinging hedge funds stand to suffer if their bets go awry.

In the U.S., the Treasury yield curve from five to 30 years has been similarly volatile, flattening more than 30 basis points this month to 78 basis points, the lowest since March 2020. Bond traders are expecting that the Federal Reserve will have to raise interest rates later next year, soon after winding down its asset purchases, to further combat inflation pressures. The last time this yield curve flattened so drastically was in June, when Alphadyne’s flagship fund tumbled 4.3% in its worst month on record.

It’s worth reiterating that these hedge funds are managed by some of the world’s best and brightest rates traders. Alphadyne Chief Investment Officer Philippe Khuong-Huu was Goldman Sachs Group Inc.’s head of interest rates in the early 2000s. Glenn Hadden, one of Alphadyne’s top portfolio managers, ran interest-rate trading at Morgan Stanley. Before founding Element, Talpins was the head trader in Citigroup Inc.’s fixed-income options franchise. Rokos, who has a mathematics degree from the University of Oxford, co-founded Brevan Howard and made trades that netted the firm about $4 billion in profits.

Yet for all the accolades and accomplishments, these hedge funds are worse off than their (mostly smaller) macro peers, which have gained 6.3% through September, according to data compiled by Bloomberg. Again, this isn’t a matter of them losing their edge over time — Alphadyne is coming off four consecutive years of double-digit gains, while Rokos surged 44% in 2020 and hadn’t previously lost more than 4% in any given year. There’s clearly something about the global macro environment in 2021, and the way markets have reacted to it, that has thrown them off their game.

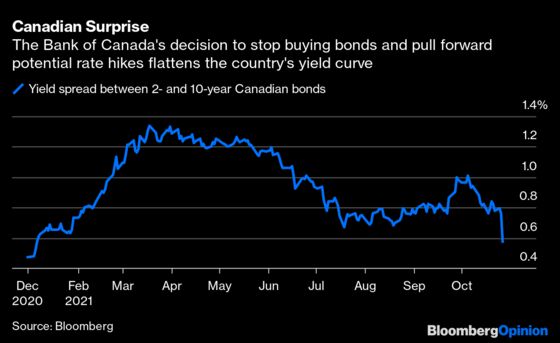

This brings us back to inflation and central banks’ policy frameworks. At the start of the year, officials were unwavering in their view that price pressures were transitory and would ultimately fade, meaning rock-bottom interest rates would stay firmly in place to support economic growth and maximum employment — ideal conditions for steeper yield curves. Ten months into 2021, central bankers are acknowledging it might not be so simple. Just on Wednesday, the Bank of Canada ended its bond-buying program and moved forward the potential timing of future rate increases to the “middle quarters” of 2022 in a bid to combat inflation. The Canadian two-year yield rose more than 24 basis points after the decision, drastically flattening the country’s yield curve.

It’s certainly possible that the recent yield-curve flattening has moved too far, too fast, given central banks seem to have a greater tolerance for overshooting inflation targets than in the past. The Fed, for its part, is still divided 50-50 between raising rates or leaving its benchmark unchanged in 2022. Traders won’t get an updated dot plot until its Dec. 15 decision.

That’s of little solace to traders like Rokos, who took big macro swings and whiffed time and again in 2021. Rates have always been a difficult market to master, of course, but the top firms seemed to have them figured out year after year. It turns out the mix of the highest inflation in decades, the lasting scars from a once-in-a-century pandemic and a potentially ill-timed policy shift by central banks can stump even the brightest hedge fund stars.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.