(Bloomberg Opinion) -- The battle over investment fees is coming to a college campus near you.

A group of Harvard University alumni known as the Class of 1969 Ad Hoc Committee on Harvard’s Endowment Management recently complained in a letter to Harvard President Lawrence Bacow that the university’s endowment is overpaying its top executives. The group has been criticizing pay at the endowment since 2003, but with performance sagging at Harvard and other big university endowments in recent years, investment fees are likely to be scrutinized more than ever.

The cost of investing has declined drastically since 2003, but little has changed at big university endowments. The asset-weighted average expense ratio for U.S. mutual funds and exchange-traded funds has fallen by half over the last two decades, according to Morningstar’s latest study of fund fees. Millennials and Generation Z are turning to financial technology for low-fee — and in some cases no-fee — investing and financial advice, forcing mighty Wall Street firms such as JPMorgan Chase and Bank of America to follow.

Meanwhile, big university endowments continue to incur huge investment costs. It’s true that executives at Harvard and other big university endowments are paid well. According to Harvard Management Co., which runs the Harvard endowment, its top five executives received a combined $35.3 million in 2017. But that’s a fraction of the fees endowments pay every year.

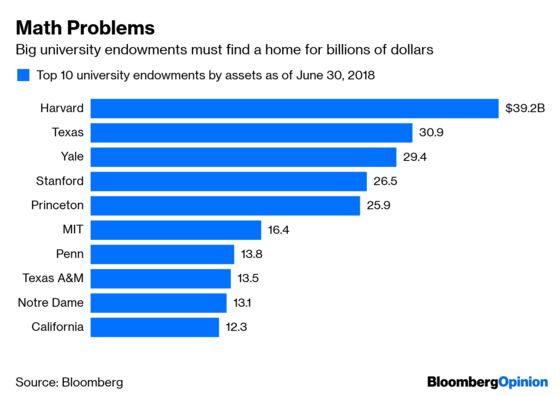

The so-called endowment model of investing pioneered by Harvard and Yale and widely adopted by other endowments calls for big investment in private assets and hedge funds, many of which still charge a 2% management fee and 20% of profits or more. At the end of fiscal year 2017, Harvard allocated roughly 58 percent of its $37 billion trove at the time to those strategies, incurring hundreds of millions of dollars in fees.

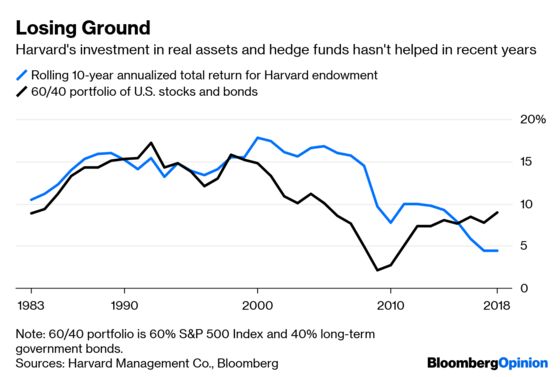

Until recently, those costs were easy to overlook. Endowments got a big boost during the heyday of private assets and hedge funds in the 1990s and 2000s. Harvard’s endowment generated a return of roughly 16% a year during the decade through 2003, outpacing a traditional 60/40 portfolio of U.S. stocks and bonds by 6 percentage points a year, as represented by the total return from the S&P 500 Index and long-term government bonds.

That stellar performance continued for several more years. Harvard’s endowment beat the 60/40 portfolio by roughly 10 percentage points a year during the 10 years through 2008. But private assets and hedge funds stumbled during the financial crisis and have never recovered their former glory. As their returns faded, so did those of endowments. Harvard returned just 4.5% a year over the last decade through 2018, lagging the 60/40 portfolio by 4.5 percentage points a year. Its experience is typical of universities following the endowment model.

The prospects for private assets and hedge funds aren’t likely to improve, at least not soon. Trillions of dollars are chasing those strategies. Private equity valuations are stretched. Capitalization rates for real estate are at historic lows. Hedge funds are struggling to find compelling trades.

That’s a problem. Harvard’s endowment contributed $1.8 billion to the university’s operating budget in 2018, which is roughly 5% of the endowment’s value at the end of 2017. At that spending rate, and assuming inflation of 2%, the endowment will have to generate a return of 7% a year just to maintain its value in today’s dollars, or 2.5 percentage points a year more than it generated over the last decade.

Suffice it to say, Harvard can no longer ignore cost. It would be easy to cut pay for executives at the endowment, as Harvard’s alumni group seeks to do, but it wouldn’t help much. The $35.3 million paid to the top five executives amounts to just 0.09% of the endowment’s value at the end of 2018, and that percentage is likely to decline as the endowment grows.

Instead, Harvard and other big university endowments will have to rein in the precious 2-and-20 they hand outside managers every year. It shouldn’t be difficult. They have billions of dollars with which to negotiate lower fees, and lots of managers are eager to count prestigious universities among their clients. Failing that, or a turnaround in the fortunes of private assets and hedge funds, endowments will have to find more affordable locales for their money.

They may not have a choice. If Harvard and other universities continue to fall short of the returns required to maintain the value of their endowments, they should expect the battle raging over fees in other realms of investing to spill onto campus.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2019 Bloomberg L.P.