Harley-Davidson Hits Stock Throttle With EV Bike Spinoff

(Bloomberg Opinion) -- Legacy manufacturers seeking relevancy in a stock market that is increasingly driven by technology giants and high-flying electric-vehicle makers are finding that two companies are better than one.

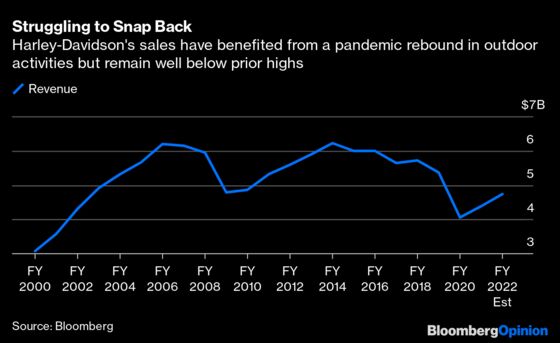

Harley-Davidson Inc. announced on Monday that it would create a separate public listing for its LiveWire electric motorcycle unit by merging the business with special purpose acquisition company AEA-Bridges Impact Corp. The transition to electric was a key tenet of Chief Executive Officer Jochen Zeitz’s “Hardwire” strategy to boost the company’s sales growth and profitability. But structural declines in demand meant that plan was set to deliver only mid-single-digit annual revenue growth in the motorcycle segment — an uninspiring target considering overall sales this year are on track to be about 30% below the 2014 peak, as Bloomberg Intelligence analyst Kevin Tynan has noted. The “Hardwire” revamp also entailed $190 million to $250 million of spending annually, a tall order for a company that lacks the backing of a larger industrial parent enjoyed by most of its rivals.

Carving out the electric motorcycle business “will give LiveWire the freedom to fund new product development and accelerate its go-to-market model,” Zeitz, who will serve as acting CEO of the new entity for up to two years, said in a statement. “LiveWire will be able to operate as an agile and innovative public company while benefiting from the at-scale manufacturing and distribution capabilities of its strategic partners, Harley-Davidson and KYMCO.” The latter is a Taiwan-based power-sports equipment manufacturer, which will also make a $100 million investment in the new LiveWire entity. Harley will retain a 74% equity interest and support the business through its engineering and manufacturing expertise and global supply-chain infrastructure — meaning it should still accrue some of the valuation benefits of repositioning for the energy transition without having to shoulder the full burden of the necessary capital investments.

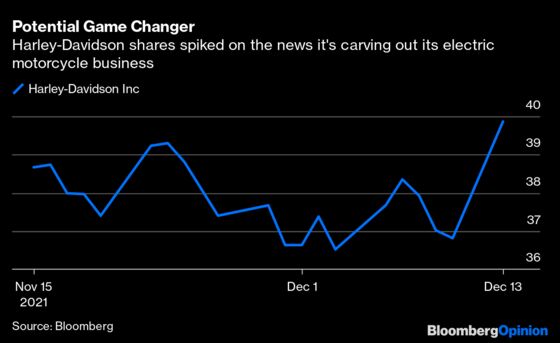

Investors are thrilled: Harley shares jumped as much as 19.5% on the news before settling down to a gain of about 5.5%. Even the smaller rise is set to add several hundred million dollars to the company’s equity value. Before Monday’s announcement, Harley’s market capitalization was essentially flat on the year.

The Harley deal is a microcosm of a bigger trend in the industrial realm. A long-standing complaint of legacy manufacturers has been that they get little credit from investors for innovation whereas startups with no revenue and business prospects that rely to some degree on hopes and dreams are rewarded with sky-high valuations. For example, EV startup Rivian Automotive Inc. has no significant revenue but a market value of more than $100 billion. And yet I regularly read reports questioning whether Rockwell Automation Inc., a company that generates close to $2 billion in quarterly sales and is in a prime position to capitalize on an arguably equally important narrative in factory-floor robotics and software, is overvalued with a $41 billion market capitalization. And Rockwell is one of the lucky ones.

As a group, industrials “have a very serious growth problem,” Melius Research analyst Scott Davis said in an interview earlier this month. For every hot product or high-flying thematic such as factory automation or indoor air quality equipment, there’s a slower-selling or out-of-favor counterpoint, like grocery-store refrigerators, oil and gas pumps or regular motorcycles. Why would investors pay top dollar for an electric motorcycle or industrial software business when it comes with all the baggage of a legacy manufacturer? The conclusion many companies are arriving at is that if they want recognition for their crown jewels, they have to give investors a chance to own them separately.

Swiss manufacturing giant ABB Ltd. is planning an initial public offering for its EV charging division in the first half of 2022; it will retain a majority holding in the business. Emerson Electric Co. is combining some of the company’s software assets with Aspen Technology Inc. to create a focused industrial software entity in which it will own a 55% stake. The idea is that the software-focused business will carry a higher multiple and have a stronger currency to use for future acquisitions. That deal is modeled after Schneider Electric SE’s 2018 merger of its software business with Aveva Group Plc in exchange for a 60% stake in the combined company. The industrial sector has been unraveling conglomerate structures for the better part of the past few decades, but most breakups have historically focused on dumping the junkier assets that were weighing down the overall valuation. Carving out the faster-growing parts to remove the burden of the industrial parent’s lackluster valuation requires a mental shift but is likely to deliver a higher payoff in today’s market.

There is a parallel debate going on in a sector tied intimately to Harley’s traditional hogs: Oil. Valuation multiples on renewables-related stocks are much higher than those of oil majors, in part because those renewables businesses tend to consume case rather than generate it right now. Like Harley, therefore, some of these companies are weighing ways to capture the excitement around the energy transition — and, thereby, lower capital costs — while keeping it integral to their overall business. Catering to two much different sets of shareholders at once is always a difficult arbitrage that tends to attract the attention of activists, as Royal Dutch Shell Plc is finding with Dan Loeb’s call to break up. A more nuanced approach, and one directly comparable to Harley’s move with LiveWire, is that of Eni SpA. The Italian oil major is set to spin off its retail energy and renewables businesses next year into a new listed entity, Plenitude, in which it will retain a 70% stake. The idea is to tap into ESG excitement while signaling the traditional business also remains committed to net-zero emissions targets.

The incumbents have an important role to play in the economy of the future but perhaps it’s a role that’s best played from a distance.

More from other writers at Bloomberg Opinion:

- Dan Loeb’s Plan for Shell Requires Delicate Touch: Liam Denning

- What’s the Right Answer to a $1 Trillion Tesla?: Chris Bryant

- Ask Rivian and Ford What It Takes to Make an EV: Anjani Trivedi

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2021 Bloomberg L.P.