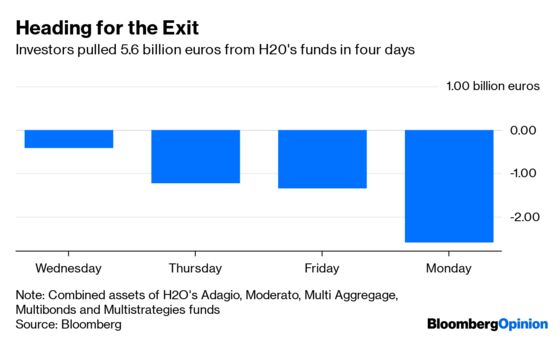

(Bloomberg Opinion) -- On the face of it, H2O Fund Management’s speed in reducing its exposure to illiquid securities should stanch the outflows that saw more than 5.6 billion euros ($6.4 billion) exit in just four days. But after Neil Woodford and GAM Holding AG both froze funds that owned hard-to-sell securities, investors are in no mood to risk becoming trapped behind a gate. They might avoid this in future by keeping in mind a few pearls of wisdom:

1) “Size is the enemy of performance.”

Guess who is the author of those words? That would be Bruno Crastes, co-founder and chief executive officer of H2O, in a glowing profile published by the Financial Times in February soon after the fund reached 30 billion euros. “It’s a great thing if we can deliver alpha without limits, but unfortunately, like everything, it doesn’t come free,” Crastes told the newspaper. Claims to the contrary would be “a lie,” he said.

If he’s right, recent withdrawals that have shrunk six of his funds to less than 16 billion euros should make generating alpha a bit easier in the future without the need to add illiquid bonds, as figures compiled by my Bloomberg News colleague Lucca de Paoli show.

Crastes was aware of the risk of growing too quickly. Last year, the firm imposed entry fees of as much as 5% to slow inflows that saw assets under management double since 2017. At his peak, Woodford oversaw almost $20 billion, while the absolute return funds that GAM shuttered a year ago had more than $10 billion of assets.

So investors should be wary of funds that have undergone rapid expansion – no matter how stellar the returns.

2) “Fashions fade, style is eternal.”

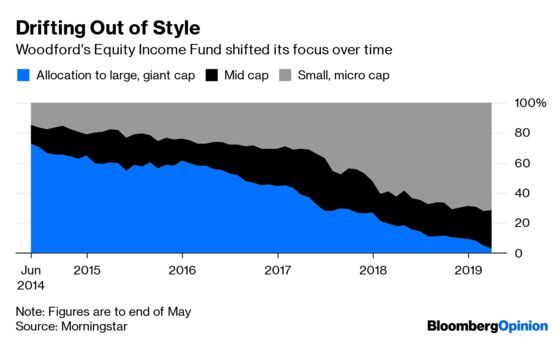

That quote, attributed to Yves Saint Laurent, is as applicable to the world of investing as it is to haute couture. Style drift – when a portfolio manager is tempted into unfamiliar assets when the previous method of making money threatens to become less profitable – is a well-established risk. It certainly seems to explain Woodford’s fall from grace, as the chart below shows.

With the yields available in the fixed income market compressing, H20 “began to search for different sources of performance,” Crastes said in a video posted by the H24 Finance news service on Friday. That search for assets that were “diversified compared to our large strategic holdings” led to the firm buying private placement bonds issued by companies linked to Lars Windhorst – which the Financial Times detailed last week, leading Morningstar to suspend its rating on one of H2o’s flagship funds and investors to head for the exit.

Investors should be mindful when a portfolio manager starts playing in a different sandbox than the one that generated returns that persuaded them to invest in the first place.

3) “It’s liquidity that moves markets.”

Legendary investor Stanley Druckenmiller was talking in 2015 about the ability of central banks to influence financial markets. But he could just as well have said that liquidity – or the lack thereof – has the power to make or break a fund.

“More than $30 trillion of global assets are held in investment funds that promise daily liquidity to investors despite investing in potentially illiquid underlying assets,” Bank of England Governor Mark Carney said in a speech in Tokyo earlier this month. On Wednesday, he went further, telling lawmakers in London that the pledge is “built on a lie.”

It’s not just investors who need to ask hard questions about how easily asset managers can buy and sell the securities they own. Regulators are waking up to the risks of what Andrew Bailey, chief executive of the Financial Conduct Authority, this week called the “regulatory arbitrage” indulged in by Woodford in his efforts to transform illiquid holdings by the expedience of listing them in Guernsey. A tightening of the rules governing how much funds can invest in untraded securities and what counts as a liquid investment seems inevitable – and probably overdue.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.