(Bloomberg Opinion) -- The “Masters of the Universe” are a lot of things, but magicians they are not.

With all of the largest U.S. banks except Morgan Stanley now having reported fourth-quarter earnings, it’s clear that bond traders struggled to meet expectations in the final three months of 2020. On Tuesday, Goldman Sachs Group Inc. disclosed fixed-income, currencies and commodities sales and trading revenue of $1.88 billion, short of estimates for $2.02 billion, even as its equities trading blew forecasts out of the water, soaring by 40%. At Bank of America Corp., FICC trading revenue was $1.74 billion, missing expectations for $2 billion. Citigroup Inc. also fell short of FICC estimates, a notable blemish given that it’s one of the larger revenue-generating groups inside the bank. JPMorgan Chase & Co. barely squeaked by, with FICC sales and trading revenue of $3.95 billion, topping forecasts for $3.92 billion.

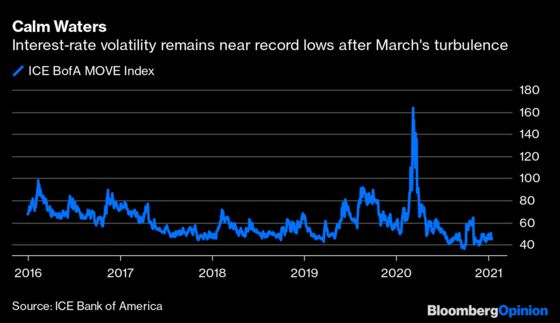

It’s not exactly a mystery why fixed-income trading slowed. For one, interest-rate volatility remained near all-time lows in the fourth quarter, as measured by the ICE BofA MOVE Index, which is a yield-curve weighted index of the normalized implied volatility on one-month Treasury options. It temporarily lurched higher in the 30 days ahead of U.S. elections, though the rise in benchmark yields was more subdued.

Meanwhile, U.S. companies took a step back from issuing new debt after borrowing at a blistering pace from April through September. About $241 billion of U.S. investment-grade corporate bonds were issued in the fourth quarter, according to data compiled by Bloomberg, compared with $389.5 billion in the third quarter and a whopping $761 billion in the second quarter. Without as many new bonds hitting the market in the final months of 2020, traders naturally had less work. The fact that credit spreads slowly compressed week after week didn’t exactly drum up much excitement, either.

Of course, fixed-income trading was largely responsible for carrying the biggest U.S. banks through the worst of the Covid-19 pandemic. At Goldman, FICC revenue in the first quarter of 2020 surged 68% compared with the last three months of 2019. Then its second-quarter FICC revenue soared 149% relative to a year earlier, beating even JPMorgan’s 120% gain. As I noted in July, this kind of blistering pace was never going to be sustainable. JPMorgan Chief Executive Officer Jamie Dimon said it best at the time: “For trading, because no one asked, cut it in half … and that’ll probably be closer to the future than if you say it’s going to still be double what it normally runs.”

Goldman’s fourth-quarter FICC revenue, at $1.88 billion, was up 6.3% year-over-year, though when compared with its huge $4.24 billion haul in the second quarter — the highest in nine years — Dimon’s back-of-the-envelope guidance looks about right. All indications suggest that between the Federal Reserve’s ultra-accommodative policy stance and the federal government’s willingness to deploy additional fiscal stimulus until the Covid-19 pandemic is in the rearview mirror, markets are neither going to experience the sharp decline of February and March nor the stunning rebound of the following months. Goldman CEO David Solomon said as much on a conference call with analysts. A lack of volatility in either direction makes life that much harder for bond traders.

On that same conference call, Stephen Scherr, Goldman’s chief financial officer, acknowledged that there “might be a less impressive opportunity set” in global markets relative to 2020. And while the bank’s asset-management arm and consumer division provide more durable revenue, “none of those are necessarily meant to be compensating factors for what could be a shortfall in global markets,” he said.

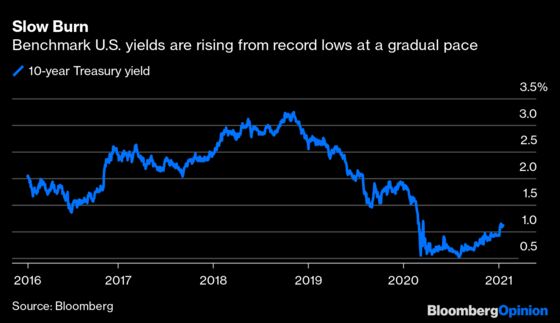

The first week of 2021 looked as if it could be the start of a significant bond-market reversal, with benchmark 10-year Treasury yields rising by 20 basis points to 1.12%. But the selling didn’t last, prompting DoubleLine Capital Chief Investment Officer Jeffrey Gundlach to say on Twitter that there’s a “yield peak in place, at least for the short term.”

At least outwardly, some bank executives seem to be taking the other side of that wager. “With the change in interest-rate environment, I think you could see a lot of activity in FICC, so I don’t think there’s a reason to think it’s going to decline dramatically from here,” Paul Donofrio, Bank of America’s chief financial officer, said Tuesday. The bank’s own interest-rate strategists are forecasting the 10-year Treasury yield to reach 1.5% by the end of the year, and some investors are starting to raise the bar to 2%. Consider me skeptical.

If interest rates are indeed kept mostly in check, that most likely puts a cap on what banks can expect from their bond traders in the months ahead. For the consumer-focused institutions, lower-for-longer yields also constrain their net interest income. That probably means a heightened focus across the board on controlling expenses: At Goldman, operating costs fell 19% year-over-year, while Bank of America’s efficiency ratio topped estimates. Investment bankers may have to pick up the slack as well. And as I wrote last week, it probably also means that the big wild card for bottom-line results in 2021 will be just how quickly the banks release credit reserves.

To get through 2020, whether it was navigating historic interest-rate volatility or helping to raise emergency cash for corporate America, bond traders had to reprise their role as “Masters of the Universe,” a phrase from Tom Wolfe’s 1987 Wall Street novel “The Bonfire of the Vanities.” Banks certainly had a great year because of this effort. In 2021, however, bond trading looks as if it will come back to Earth. It’s up to Wall Street CEOs to figure out how to make sure their profits don’t follow the same trajectory.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.