Maybe Goldman Sachs Should Take the Rest of the Year Off

(Bloomberg Opinion) -- Another day, another dollar — or rather another few billion dollars in surprisingly strong results from a big U.S. bank.

Goldman Sachs blew away the superlatives Friday with forecast-beating profits and revenues across the board for the third quarter. You could almost hear the analysts throwing bouquets for outgoing Chief Financial Officer Stephen Scherr on his last call. Its shares were up more than 3%.

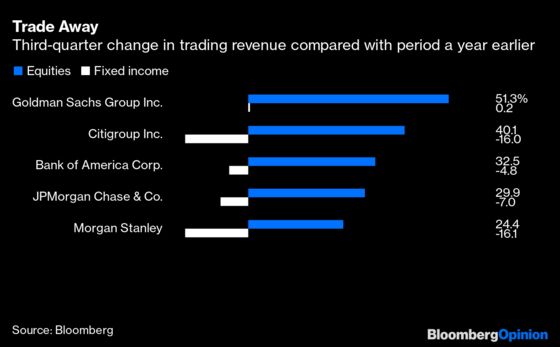

Goldman outperformed all the other banks that have reported this week in its core business of trading equities, bonds, currencies and commodities. It also turned in strong numbers for investment banking and its consumer and wealth businesses.

It reported total revenue for the first nine months that was greater than any 12-month total it had previously reported, but I doubt Chief Executive Officer David Solomon will be telling his employees to take the rest of the year off.

One of the main ways that Goldman is doing this is by expanding its balance sheet and financing more trades. Its risk-weighted assets — the measure of assets that is used to set capital requirements — have grown 10% during the year and are 23% larger since the end of 2019.

Most of that growth has come in the trading business, where Goldman has been doing things like lending to young financial technology companies to fund the mortgages they originate. Goldman will then turn round, repackage those and sell them to other investors later. This kind of business should grow further with GreenSky, the buy-now-pay-later business it is buying for $2.2 billion.

This kind of activity helped its FICC financing grow 55% compared with results in the period a year earlier, which was a chief reason that Goldman was the only big U.S. bank in the third quarter to hold its total fixed-income trading revenue flat compared with a forecast for a decline of 22% and the loss of revenue endured by its peers.

Financing in the equities trading business was up even more. Revenue doubled compared with last year’s figures and helped the equities trading revenue line beat forecasts by 41% — easily the strongest beat among its peers and putting it ahead of Morgan Stanley for the quarter.

Equities financing mainly means lending to hedge funds. The gain there was possibly less about simply taking market share from European banks that have lost their appetite, such as Credit Suisse, and more to do with switching out weaker, less profitable clients for more interesting and more profitable ones.

One way in which Goldman didn’t expand its balance sheet was through attracting billions of dollars of extra deposits from ordinary people that it would have to keep in low-yield Treasuries or central bank funds. It’s not that sort of bank after all.

It is, however, the sort of bank that also beats its rivals on net interest income growth — which investors were hoping was where all the big traditional lenders would do well. Lending more to rich clients in its consumer and wealth business lifted net interest income there 36% year-over-year. And all that financing in its trading arm lifted NII for the markets division by 45% year-over-year.

Solomon sounded a sober note on dealmaking: M&A has been driven by private equity funds, and that will have to slow down. He said Goldman was being more careful about the risk around big deals, which sounded as if he is becoming wary of getting stuck with a large chunk of leveraged buyout financing at some point.

But that was the only downbeat, and any worries about bubbles or market stumbles can wait for another day. Maybe the bank should take the rest of the year off and come back after the Federal Reserve has begun its next experiment in taking away the massive monetary support for markets that has driven this banking boom.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2021 Bloomberg L.P.