Goldman Sachs Bankers Win Big. Its Investors Aren’t Pleased.

(Bloomberg Opinion) -- Goldman Sachs’s workers have been the big winners from the recent boom in dealmaking and trading compared with both its shareholders and peers at rival banks.

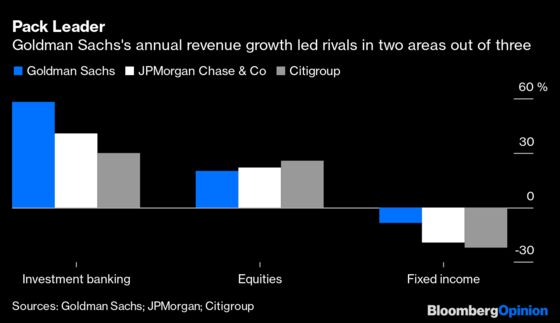

Investors didn’t take the news well: Goldman’s stock tumbled 8% even though it reported record full-year revenue and profits on Tuesday. The bank’s performance in fourth-quarter and full-year investment banking fees and trading revenue in bonds, currencies and commodities also beat that of rivals and analysts’ forecasts. Stock trading was the only downer.

But the concern for investors is that profits are going to be squeezed from here. Higher pay is pushing up costs when revenue in investment banking and markets is expected to slow compared with last year and much of the year before. The central bank and government stimulus during the pandemic that drove activity is being reduced or removed, and higher interest rates coming this year are likely to make investors and company leaders more cautious.

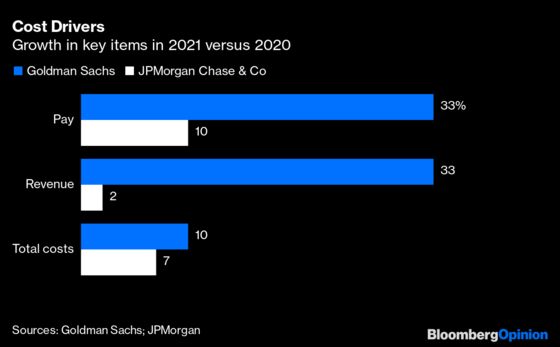

JPMorgan Chase & Co. already said last week that a mix of pay inflation and technology investment costs meant it would return less than its potential over the next couple of years. At Goldman, overall expenses rose more than 10% in 2021, outstripping JPMorgan’s 7%, while Goldman’s payroll costs jumped 33% compared with JPMorgan’s 10%.

To be fair to Goldman, its total net revenue growth of 33% and net earnings growth of 129% also far exceeded the other big U.S. banks that have so far reported.

Goldman Chief Executive Officer David Solomon tried to ease concerns about the revenue outlook. He said that dealmaking among clients should stay strong and that its trading desks should keep taking a leading share of revenue even as markets activity normalizes.

But he acknowledged that wage inflation is everywhere in the U.S. economy, and he was unashamed about the bank’s commitment to hand rewards to top talent. He could hardly complain about the costs of retaining top bankers given the special stock-based bonuses that he and top deputy John Waldron were handed by the bank’s board late last year.

Some of this jump in pay for Goldman’s bankers may be catch-up from the relative conservatism shown by Goldman and other banks in 2020 when the path of the economy through the Covid pandemic was more uncertain than it appears today. But shareholders bore the brunt of that too as regulators demanded banks retain more capital.

Payouts to shareholders through dividends and renewed buybacks rose $3.8 billion to a total of $7.5 billion for 2021, but the extra pay handed to Goldman’s bankers grew by $4.4 billion. In short, the bankers took a greater share of the improvement in the bank’s income.

The deal with traders and investment bankers is that a large chunk of pay is variable. Bonuses and therefore costs in general should fall if activity drops off. But things have been changing on this front, too: More of Goldman’s workers are in jobs with more regular salaries than in the past in areas such as asset management and the consumer business, for example. A big part of the 8% rise in headcount was in technology staff, it said.

On top of this, the bank has been rolling out more non-monetary benefits such as better parental leave and pensions. These are great for Goldman’s people, especially those in administrative or support roles. But they raise the proportion of fixed costs in Goldman’s pay, too, which makes it less responsive to a slowdown. Some of that will matter less if the consumer and wealth business starts to generate better returns as it grows; it is still relatively early days.

Goldman turned in its best return on equity since before the 2008 financial crisis with its 2021 results at 23%. The thing is, that might the best investors see for a few years to come.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2022 Bloomberg L.P.