Global Bonds Are Selling Off for All the Right Reasons

(Bloomberg Opinion) -- The weakness in the global bond market on Tuesday is surprising for one primary reason: It’s a sign central banks may finally be taking the right steps to get the worldwide economy back on track.

Central banks have taken a lot of heat by trying to combat slowing economic growth and inflation with the same strategies that have so far largely failed — that is, cutting interest rates even lower or, in some cases, further below zero. While such measures may have prevented a much more painful slowdown, they have done little to actually boost growth.

The policies have mostly resulted in flat and inverted yield curves in most major economies, providing little incentive for banks to extend credit. “I always thought it was going to be a bout of higher inflation that was going to end the central bank monetary madness, but maybe it’s just the realization that you need a functioning banking system in order to have a growing economy,” Bleakley Financial Group Chief Investment Officer Peter Boockvar wrote in a note to clients on Tuesday.

The Bank of Japan has been one of the primary offenders of zero-interest-rate policies, but it decided this week to try the opposite approach. It indicated Monday that it would try to steepen its yield curve by not buying debt with maturities of more than 25 years. The result a day later was the country’s worst auction of 10-year government bonds since 2016, sending its debt market reeling and pushing the gap between two- and 10-year yields to 11.5 basis points, the widest since April. That’s still extremely flat, but it’s moving in the right direction. The sell-off spilled over into European debt and Treasuries, though U.S. bonds reversed course after a weak report on manufacturing.

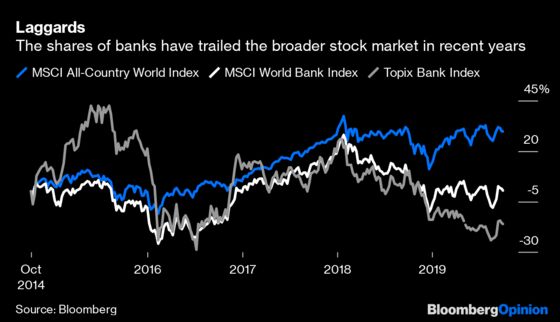

It’s generally accepted that one of the keys to a healthy economy is a robust banking system. But for some reason, central banks have only made it as difficult as possible for banks around the world to thrive. After all, banks make a big chunk of their money by borrowing at low short-term rates and lending that money out for longer periods at higher rates. While the broad MSCI All-Country World Index has gained 26.5% over the past five years, the MSCI World Bank Index has dropped 1.8% in the same period. The Bank of Japan was one of the early adopters of a zero-interest-rate policy and a flat yield curve. As a result, the country’s banks have been hit particularly hard, with the Tokyo Stock Exchange Banks Index tumbling 21% over the past five years.

There’s another side effect of low or even negative rates, which is that economists are starting to believe they have the unintended consequence of boosting savings rates as consumers sock away even more of their earnings to make up for lost interest income. At a recent 8.1%, the personal savings rate in the U.S. is double what it was heading into the financial crisis, when the target federal funds rate was 5.25%. That can also be seen in the amount of excess liquidity at U.S. banks, defined as deposits minus loans, which Fed data show has surged to $3 trillion from about $250 billion in 2008.

The banking industry doesn’t engender a lot of sympathy, nor does it deserve any for its role in fostering the abuses and excesses that led to the financial crisis. And nobody is saying that central banks should promote policies that nurture risky behavior. But there’s something to be said for setting monetary policy in a manner that promotes a healthy banking industry rather than hinders its growth.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.