GlaxoSmithKline Needs More Cash to Catch Up on the Science

(Bloomberg Opinion) -- When a company faces shareholder activism, the temptation is to find quick rewards for investors at the expense of the business. But GlaxoSmithKline Plc — now a target for Elliott Management Corp. — is in a bind because its heavy dividend commitments have already long constrained its ability to invest in new medicines.

The U.K. drugmaker should use the forthcoming separation into two distinct businesses — consumer health care and pharmaceuticals — to break with the past, rebuild its finances and accelerate its scientific ambition.

With a market value of 67 billion pounds ($95 billion), Glaxo has 21 billion pounds of net debt and a high dividend to service. While the announced split will involve a cut to the annual payout, its ability to alleviate the company’s strain is an open question.

Glaxo must decide how best to decouple the consumer side, a joint venture with Pfizer Inc. that’s behind brands including Aquafresh and Nicorette. The seemingly shareholder-friendly approach would be to spin off its majority stake to investors and let them decide what to do with the new shares. This would create a fully independent company free to set its own destiny. Analysts at Jefferies value the consumer business at 45 billion pounds, implying Glaxo’s stake is worth around 30 billion pounds.

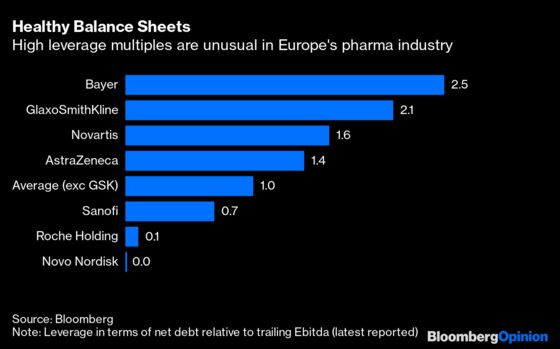

But a straight demerger would still leave the main pharma business at a relative disadvantage financially. True, Glaxo is planning to load the consumer arm with high borrowings disproportionate to its profit contribution. That would leave the pharma business less stretched, with net debt at 1.7-1.8 times profit on the Ebitda measure, according to Jefferies estimates. Yet this is still above most of Glaxo’s European rivals which, except for German peer Bayer AG, are at 0 to 1.6 times.

A single cash acquisition could push Glaxo’s borrowings to an uncomfortable level. This matters because Glaxo needs to be capable of opportunistic deal-making — its pipeline won’t start delivering profits until the second half of this decade.

At the other extreme, Glaxo could turn the consumer business into a listed piggybank by doing an initial public offering followed by sales of chunks of the remaining holding to raise funds as needed. But in this scenario, Glaxo investors would still see a conglomerate that merits a valuation discount. Investors in the consumer business would fear the next share sale. The consumer shares may trade weakly and become a double drag on the parent.

Luckily, this isn’t an either-or choice. A middle way would be to do an IPO and a demerger in tandem, bringing in enough cash from selling shares in consumer health care to put the pharma business on a stronger footing, but no more. Raising around 2 to 3 billion pounds this way could help bring the pharma business’s leverage more in line with peers. Spinning off the rest of the consumer stake would achieve the benefit of giving the unit full independence.

Then there’s the wild card Glaxo can’t control — a pre-emptive bid for the whole consumer business, either from another health-care company or one of the consumer-products giants. Glaxo ought to be open to any such approach. If a deal could be done, most of the proceeds could be returned to investors via a special dividend, with a portion used to cut leverage in the pharma business.

Glaxo has been dogged for too long by questions of whether it can afford its dividend, let alone large-scale M&A. There’s no point going through all this rigmarole and not fully eliminating such doubts. Chief Executive Officer Emma Walmsley delivers a major strategy update later this month. Using the separation to raise capital without a specific plan for the proceeds might be unpopular. But giving “new Glaxo” genuine financial freedom is reason enough to do it.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2021 Bloomberg L.P.