(Bloomberg Opinion) -- The U.S. stock market had one of its best months ever in November, with the S&P 500 Index surging almost 11%. Many are again questioning whether equities have become disconnected to reality as the Covid-19 pandemic rages anew. Lost in the debate is the potential for an explosive economy in 2021 given the magnitude of excess savings that households have accumulated, a sum that probably totals about $1.4 trillion.

Even the Federal Reserve is starting to realize just how beneficial this pot of money will be to the economy going forward. At the November Federal Open Market Committee meeting, Fed staff no longer assumed that another round of fiscal stimulus is coming. The lack of such support was offset in their forecast by household saving. From the minutes of the meeting:

Although this lack of additional fiscal support was expected to cause significant hardships for a number of households, the staff now assessed that the savings cushion accumulated by other households would be enough to allow total consumption to be largely maintained through year-end.

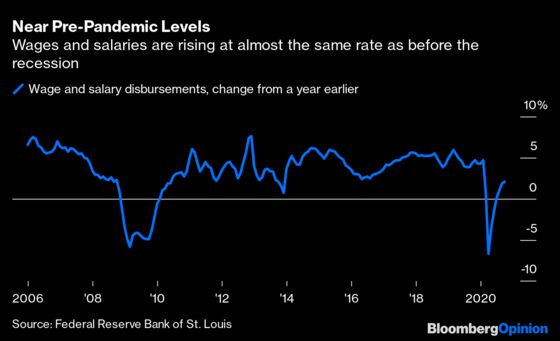

I have been focusing on excess saving for some time now, but my prediction it would replace fiscal stimulus as the economy’s primary measure of support was wrong. Savings did not cushion the economy after the first fiscal cliff this past July; wages and salaries were the cushion.

Lost in the concern about fading fiscal support has been the V-shaped recovery in wages and salaries, which are nearing their pre-pandemic levels and are even positive on a year-over-year basis.

The notion that fading fiscal support would crash household spending hinged on the assumption that there were no jobs available to compensate for the income lost from declining federal support. That was wrong, and will likely continue to be wrong in aggregate. The underappreciated Job Openings and Labor Turnover data indicate that job openings, while down from the peak, did not suffer a decline like in the last recession and now hover at 2017 levels.

Rising wages and salaries means that households can support spending without touching accumulated savings. Of course, this doesn’t hold true for all households, but micro stories are not the macroeconomy. In aggregate, savings rates have remained persistently high even after the economy moved through the first fiscal cliff at the end of July. Although the saving rate, at 13.6% in October, is down from the peak of 33.7% in April, it’s still much higher than pre-recession levels and the average of 7.5% in 2019.

With Covid-19 vaccinations about to commence, the economy will likely rebound quickly without the need for households to tap accumulated savings. (The median estimate of economists surveyed by Bloomberg is for the economy to expand 3.8% in 2021 after contracting 3.6% this year.) The primary factory restraining the economy is the services sector, as spending on goods is above the pre-pandemic trend. A vaccine will allow the services sector to come online fairly quickly and close the output gap, or the distance between where the economy is and where it would have been in the absence of the pandemic. Rough estimates of the output gap indicate the economy should be producing 5% more goods and services than were actually produced in the third quarter.

This is where we need to start thinking about the possibility that households tap their accumulated savings, pushing the savings rate below zero after the economy has largely normalize. Based on the same methodology I used in August, I estimate households have accumulated $1.4 trillion of excess savings, which is equivalent to about 6.6% of gross domestic product. This represents the remnants of the $2.2 trillion CARES Act passed by Congress in March. The hallmarks of that program included $1,200 payments for adults making up to $75,000 and $500 for their children, as well an extra $600 in weekly unemployment benefits. In addition, households save simply because their ability to consume services is constrained.

Policy makers and market participants have yet to fully appreciate the magnitude of accumulated savings because the numbers are so large and out of historical context that they are difficult to comprehend. Also, there seems to be a false impression that savings are already being drawn down. That’s just not happening on an aggregate level.

The thing to know is that these accumulated savings represent a massive amount of stimulus that is more than the current output gap and could spark an economy already set to normalize. I expect households will start spending their accumulated savings next year as confidence rebounds and very likely after the economy is already on its way to full recovery. It doesn’t take much imagination to see how that could supercharge an already vaccine-induced hot economy.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2020 Bloomberg L.P.