German Fund Giant Captures the Investing Zeitgeist

(Bloomberg Opinion) -- It’s been almost three years since DWS Group GmbH made its stock market debut when Deutsche Bank AG sold about a fifth of its stake in the company. After a shaky start, with missed self-imposed asset growth targets and costs heading in the wrong direction, Germany’s biggest fund manager is reaping the benefits of being at the forefront of two big industry trends.

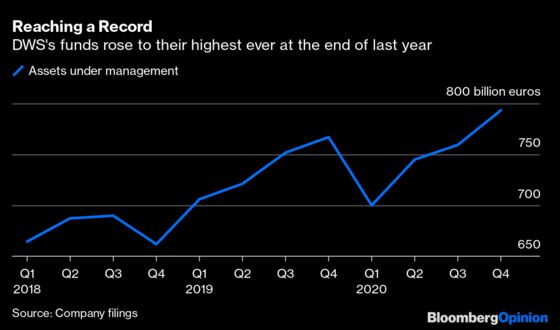

DWS grew its total assets under management to a record 793 billion euros ($951 billion) last year, attracting net inflows of more than 30 billion euros. More than half of that new money went into passive products, and more than a fifth of the cash it oversees is in index-tracking funds.

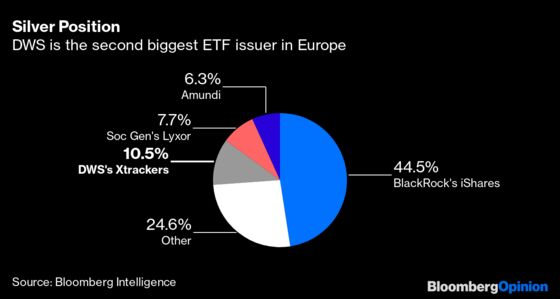

Europe’s exchange-traded funds market grew by more than a fifth last year to reach almost $1.2 trillion, according to data compiled by research company ETFGI. DWS’s ETF business, the second-biggest in Europe, gives it a useful bulwark against the years-long trend of investors abandoning active fund managers in favor of low-cost index tracking funds.

Moreover, a third of last year’s net inflows went into DWS funds that focus on environmental, social and governance concerns. Globally, investors allocated a record $13 billion to ETFs that only invest in climate-friendly companies in December alone, according to data compiled by BloombergNEF.

Starting this year, all new investment products that DWS offers will be ESG funds, Chief Executive Officer Asoka Woehrmann told Barron’s magazine earlier his month. That’s a bold move, but in step with the current zeitgeist.

The greater reliance on passive products, which typically charge clients less than for active management, saw the annual management fee achieved by DWS slip to 28.3 basis points from 29.6 basis points at the end of 2019. But it’s better to have a stronghold in a growing low-margin business than depend on a shrinking active sector where fees are also under pressure.

Costs are the one aspect of the business that fund management companies can control, and DWS has met its post-IPO target a year early. Its cost-income ratio, which was 76% at the end of 2017, dropped more than three percentage points last year to 64.5% as it slashed expenses by 11%. The firm has set itself a new goal of 60% by the end of 2024, which looks challenging but achievable provided it can grow the income side of the ledger.

As good as last year was for DWS, it can’t achieve the stated aim of its biggest shareholder for it to become a top 10 global asset manager through organic growth alone. Should Societe General SA finally decide to offload its Lyxor fund management arm, a sale which has been mooted for more than a year, DWS would surely be interested in Lyxor’s 150 billion euros of assets. But it would probably find itself in a takeover battle with bigger French rival Amundi SA.

Some of the trends that benefited DWS last year, including rising stock markets that boosted the value of assets under management and persuaded investors to allocate more capital to stock pickers, will also have helped its European rivals. But the German firm’s stellar 2020 performance shows it is at the sweet spot of the flows into passive strategies and the rise of environmentally conscious investing.

If the long-predicted redrawing of the European asset management landscape finally happens, DWS won’t want to be left behind.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2021 Bloomberg L.P.