(Bloomberg Opinion) -- Has it only been a year?

Tuesday marks the one-year anniversary of General Electric Co.’s ouster of CEO John Flannery in favor of board member Larry Culp, an outsider respected for his operational prowess and dealmaking as the former head of Danaher Corp. It was an abrupt change for a company that usually moves at a glacial pace, but the prospect of a steep quarterly operating loss in GE’s struggling power unit and a $22 billion goodwill writedown on the disastrous acquisition of Alstom SA’s energy assets convinced the board that Flannery wasn’t moving nearly fast enough to save the company.

It feels like much more time has passed since that fateful management switch, and that’s partly to Culp’s credit: He’s been much more aggressive and decisive than his predecessor about divesting assets to shore up GE’s financial position, and he has worked systematically to refashion the board and instill a new operating ethos in the industrial businesses. Culp cut GE’s dividend, started unwinding its stake in the Baker Hughes energy business and agreed to sell its biopharma operations to Danaher for $21.4 billion. Thus far, he’s managed to avoid the kind of massive surprise writedowns that marred Flannery’s tenure.

Culp’s furious pace of activity has helped stabilize GE, which is no small feat when you think back on the mess he inherited. But the stock is still lower than when he started and has stalled out at about $9 or $10. And at this point, most of the big, obvious buttons for change have been pushed. The company could sell its remaining health-care assets, although the fact that it’s scheduled an investor day focused on the business for December suggests it wants to keep that in the fold for now. A divestiture of its aircraft-lessor arm Gecas has been bandied about but is highly difficult to execute in practice. And GE’s biggest demons – including weak underlying cash-flow capabilities and risky black holes at GE Capital that despite Culp’s best efforts have at best turned a shade of mud-brown – have no quick fix.

There’s not much for Culp to do now other than grind it out on cost cuts and operational rigor, and cross his fingers that the industrial weakness that's emerged around the globe won’t get any worse. GE's pension and insurance liabilities are at risk of ballooning from the slump in interest rates. As such, Culp’s second year seems likely to be lighter on big announcements and highly dependent on the whims of the broader marketplace. A stock rally from here depends on investors taking the long view.

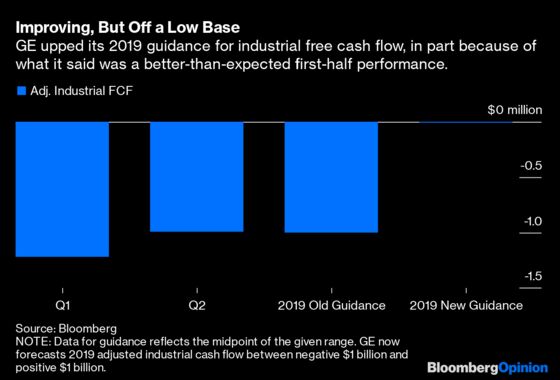

So far, they’ve been willing to accept any scrap of marginal good news as a sign of changing tides. Culp has somehow even managed to make the prospect of zero free cash flow from the industrial businesses this year feel like a win. But the path to a significant improvement in cash flow in 2020 and 2021 remains highly murky in the best of times, and an outright fantasy in a recession environment. One of the more fascinating aspects of GE’s challenges is that they emerged at a time when other manufacturers were doing well. That’s changing: The Institute for Supply Management's gauge of U.S. manufacturing activity fell deeper into a contraction in the month of September in the weakest reading since 2009. Meanwhile, a slowdown in the Chinese economy risks threatening even GE’s crown-jewel aviation unit.

One thing that Culp does have control over is the company’s messaging. The biggest mistake of his tenure so far, in my opinion, has been his failure to do away with the myriad of opaque adjustments that have cluttered GE’s financial statements and presentations. For all Culp’s talk about 2019 being a “reset year,” this is the one thing he hasn’t been willing to reset and it has cost the company some credibility. Culp hasn’t ignored investors’ calls for more transparency: The company hosted a so-called “teach-in” to educate investors on the vagaries of its long-term-care insurance business, for example, and gave cash-flow numbers for its operating units on an annual basis. But the disclosures tend to be piecemeal, and when they do come are presented in a way that flatters the company or relies on overly optimistic assumptions. My Bloomberg Opinion colleague Matt Levine recently flagged a paper that concluded at least some investors are misled by non-GAAP expense exclusions. He finds this theory frustrating for reasons you can read here, but in the case of GE, it’s not hard for me to believe that it’s true.

GE is now on the hunt for a new chief financial officer, having announced in July that Jamie Miller would be stepping down from the job. Investors are focused on who the new hire could be and the prevailing thought is that Culp has to get someone with a big name and a respected background. Perhaps. But what he really needs someone who’s willing to reverse GE’s culture of carefully engineered earnings guidance and tell it straight to investors. A candidate concerned about guarding his or her hard-earned reputation might not be willing to do that, but it’s the kind of reckoning GE still needs.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.