(Bloomberg Opinion) -- General Electric Co.'s turnaround is advancing to the next stage, but it still has a ways to go.

The industrial conglomerate on Wednesday said its chief financial officer Jamie Miller would be stepping down as soon as she transitions her responsibilities to a yet-to-be-identified replacement. Miller was one of the more visible legacies of an era that everyone associated with GE would like to forget. She was named to the CFO job in 2017 by then-CEO John Flannery after the total collapse in GE’s earnings and cash flow expectations made it impossible for former CFO Jeff Bornstein to continue in his role. Flannery was then ousted last year after a series of surprise writedowns added to investor frustrations over a turnaround that seemed to move too slowly.

I’ve always felt a bit bad for Flannery; his job was to expose and start to clean up GE’s deep-rooted flaws and there was never going to be any glory in that. But it bothers me that GE put Miller, its first female CFO by my count, into that kind of no-win situation. She wasn't a GE-lifer like Flannery was, but despite the company’s efforts to paint her as an outsider, she’d been with the company since 2008. Not that she didn’t make mistakes: An unfortunate run of forecasts that proved too optimistic did little to endear Miller to investors.

Many wondered why Flannery’s successor, Larry Culp, wasn’t doing more to clean house. The most logical explanation is that he needed to maintain some sense of continuity while he got his hands around the problems at GE. In the company’s second quarter earnings, also released on Wednesday, there was some evidence he is doing just that.

GE’s struggling power unit posted operating profit of $117 million in the second quarter, down significantly from a year earlier, but up slightly relative to the first quarter and better than some analysts had expected. Fixed costs for its gas turbine operations were down 10% from a year earlier, while orders were up 28%, excluding the impact of M&A and currency swings. After earlier estimating the cash burn in the power unit would worsen from $2.7 billion last year, GE now says there’s a possibility performance may be flat in 2019. That’s after taking into account a reallocation of its grid solutions business to the renewable energy unit, a move which resulted in a $744 million pre-tax goodwill writedown in the quarter.

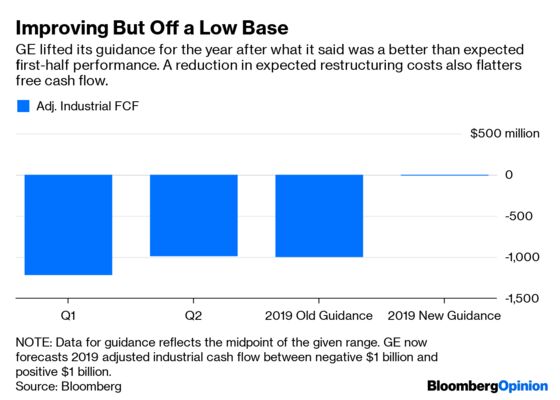

But there were also still remnants of the old GE, the company that turned managing Wall Street expectations into an art form. The company raised its forecast for industrial free cash flow this year, predicting at worst a $1 billion decline versus a previous call for as much as a $2 billion cash burn. GE now says there’s a possibility industrial free cash flow can even be positive for the year, to the tune of $1 billion. Some of that is a reflection of the apparent progress in turning around the power unit. But a fair chunk is tied to lower expectations for restructuring costs this year. GE spent just $382 million pre-tax on restructuring and other items in the second quarter, down nearly 40% from the same period a year ago. It now expects to spend around $1.5 billion on cash restructuring this year, compared with a previous estimate of more than $2 billion.

This is a bit weird. Recall that Flannery was pushed out in part because there was a perception that he lacked urgency in fixing GE’s power unit and that much more aggressive cost-cutting would be needed to right that business. GE says the lower estimate is due to a combination of timing, attrition and the execution of projects at a lower cost than projected. But most of the restructuring expense was meant to be weighted toward the second half of the year, per Miller’s guidance, so it’s unclear how GE would have that kind of visibility at this point. Risks to this improved guidance include the grounding of Boeing Co.'s 737 Max. GE, which provides the engine for the Max through its CFM joint venture with Safran SA, said Wednesday the grounding and Boeing's subsequent production cut had shaved $600 million off its cash flow from operating activities in the first six months of the year. The company expects a $400 million hit per quarter in the second half of the year, should the Max stay grounded.

More importantly, GE left its wishy-washy forecast for 2020 and 2021 intact, calling for positive industrial free cash flow next year and then further acceleration in 2021. Even with just $1 billion of cash burn in 2019, it’s tough to see how GE exceeds the $4.5 billion of free cash flow it generated last year (itself a depressed level) on an annual basis in that time frame. For what it’s worth, JPMorgan Chase & Co. analyst Steve Tusa is among the most bearish of Wall Street analysts on the company’s 2020 and 2021 free cash flow prospects and he’s been modeling a slightly positive number for this year. GE raising its free cash flow expectations is a win, but it’s worth asking if that forecast was ever really that realistic in the first place or if it was just another way of playing the game of earnings.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.