(Bloomberg Opinion) -- It’s been a busy week for General Electric Co. On Tuesday, the company announced it would sell another chunk of its stake in its Baker Hughes oil and gas venture, ultimately raising about $3 billion. Two day later, it said it would buy back up to $5 billion of bonds. This activity gave CEO Larry Culp something concrete to point to on Thursday when he took the podium at a Morgan Stanley conference to update analysts and investors on the industrial conglomerate’s turnaround progress.

“We’re doing what we said we would do," Culp said. That means "tending to the balance sheet, making sure that we’re strengthening our overall financial position, and making sure that we’re in a position to run the businesses better."

GE’s efforts to reduce its bloated debt load are a positive; that’s what it’s supposed to be doing. Culp’s ability and willingness to be proactive is undoubtedly an improvement over former CEO John Flannery’s long stretches of paralysis. But the timing of this flurry of deleveraging steps strikes me as slightly curious.

Most companies wouldn’t go around buying back bonds when rates are so low; they would swap them out for new bonds at better terms. GE, however, has pledged not to add any new debt through 2021, and appears to be trying to signal its liquidity is such that it doesn’t need to. Yet Culp has also talked about running the company with a higher cash balance in order to reduce its reliance on commercial paper. And the $21.4 billion divestiture of GE’s biopharmaceutical business to Danaher Corp. – the linchpin in Culp’s debt reduction plan – hasn’t closed yet.

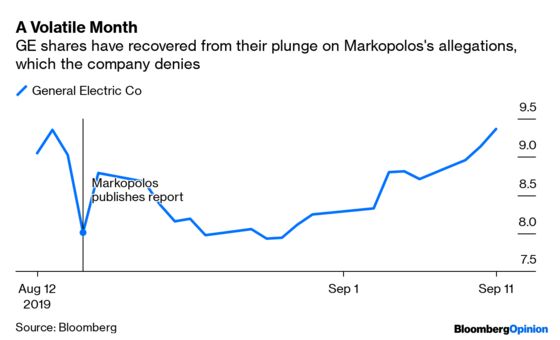

Perhaps the Baker Hughes stake sale and the bond buyback were planned well in advance; perhaps GE is just being opportunistic and taking advantage of recent trading conditions. I can’t help but notice, though, that GE’s actions this week appeared to hit at the heart of criticisms made by Bernie Madoff whistle-blower Harry Markopolos last month in a lengthy, explosive report.

Markopolos has an agreement with an undisclosed hedge fund that will give him a share of the profits from bets that GE shares will decline. GE has called his allegations “meritless.” His report claimed GE needed to immediately funnel $18.5 billion in cash into its troubled long-term care insurance business and accused the company of avoiding a writedown on its Baker Hughes stake. One way to read the debt buyback is that GE must not be too worried about a fresh cash shortfall at the insurance unit if it’s willing to plop down $5 billion to repurchase bonds on a voluntary basis. And GE’s stake sale this week will bring its holdings in Baker Hughes below 50%, which will prompt a charge that could be in the ballpark of $8 billion to $9 billion but also allow management to put one more inevitable writedown behind them.

There were a number of flaws in the Markopolos report, not least his liberal use of hyperbole, but it struck a nerve with investors who were already wary of more negative surprises at GE and the opaqueness of its underlying financials. Whether or not there’s any truth to his allegations, being on the hot seat like that appears to have shaken GE executives as well.

What’s most telling is the one Markopolos criticism that GE hasn’t yet moved to address, and that is the lack of detailed transparency in its financial statements and the seeming differences in its aviation unit’s accounting relative to engine partner Safran SA. Culp missed an opportunity when he became CEO to move away from GE’s historical tendency to rely on a myriad of adjustments and a micromanaging of Wall Street expectations to bolster the appearance of the company’s results. This week’s actions and Culp’s presentation were in a way a reminder that of all of Markopolos’s claims, questionable as the others may be, that one has the potential to stick.

Otherwise, the key takeaways from Culp’s Thursday presentation were that he expects the drop in interest rates to result in a “somewhere south” of $1.5 billion hit to its GAAP reserve assumptions for the long-term care insurance business, before accounting for any other adjustments as part of a third-quarter test. GE's projected pension benefit obligations, meanwhile, will also increase because of the drop in interest rates. Offsetting that is an improvement in returns, but GE is still looking at an impact in the $7 billion range, Culp said. Neither of those figures are disastrous, but serve as a reminder that it’s not just regular old debt that’s looming over GE. There are many other demands on its cash.

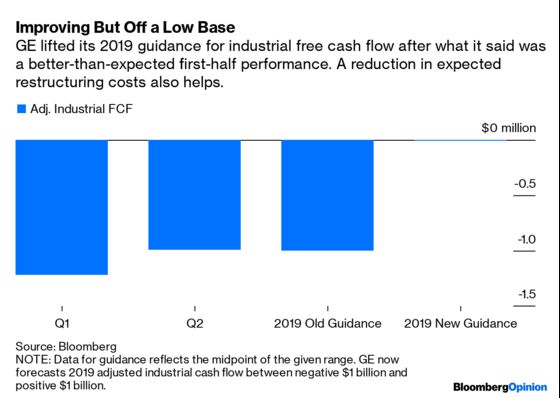

Culp gave no update to GE’s expectation for roughly zero dollars in industrial free cash flow this year. Interestingly, he did allude to the idea that the company’s forecasts for 25 to 30 gigawatts of gas turbine demand this year may prove overly dire; still, I remain skeptical of GE’s ability to drive a huge surge in free cash flow at the power unit over the next few years. Other challenges at the company include persistent questions about the true underlying free cash flow of the aviation unit, the loss of cash-flow contributions from divested assets and the need to backstop its huge underfunded pension balance with more cash. Culp didn't rule out additional contributions to the pension over the next few years.

Progress on the debt reduction front is good, but without a significant increase in free cash flow, it will be a while before GE can shift investors’ focus elsewhere.

GE said in July that deconsolidating Baker Hughes's results from its own would prompt a $7.4 billion writedown, based on the company's stock price at the time of $24.84. This week, it said every $1 change in Baker Hughes's stock price would increase or decrease that number by about $500 million. GE's share offering was priced at $21.50 and the stock was trading on Thursday for about $22.50.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.