(Bloomberg Opinion) -- I have questions about Larry Culp’s $47 million payday at General Electric Co.

GE last week hit the share performance threshold that triggers the first tier of a one-time equity grant for Culp that could ultimately amount to as much as $230 million, according to a Bloomberg News analysis. The bonus was originally set up when Culp was named chief executive officer in 2018. It was meant to reward the former Danaher Corp. CEO for taking on the stewardship of a company whose best days looked to be behind it and to incentivize him to follow through on a turnaround job that at times has seemed impossible. One of those times was earlier this year, when the pandemic engulfed the crown jewel aviation unit that had been the company’s salvation through years of woes in the gas turbine and insurance businesses. With this unprecedented and unpredictable event upending the first tangible signs of stabilization at GE, it felt fair to give Culp some more time to steer the company into a better direction. So in August, the company rejiggered the terms of the pay package.

GE’s board extended Culp’s contract through at least 2024 with an option for a one-year extension, giving him a few extra years for his turnaround efforts to yield results; fine. But it made the curious decision to also lower the stock performance thresholds. The trigger for the lowest tier of Culp’s pay package dropped to about $10 from nearly $19. As long as Culp could keep GE’s stock price in the $10 range for a month, he would lock in a payout of at least $47 million. In August, GE’s stock price was hovering around $6, so getting to $10 required a significant rally. But as I wrote at the time, considering Culp had five years to hit that target and the stock traded higher than that when he took over, it hardly felt aspirational enough to warrant a $47 million payday. It turns out Culp only needed four months, not five years, to hit the target after a furious fourth-quarter rally on vaccine optimism and an improving outlook for free cash flow.

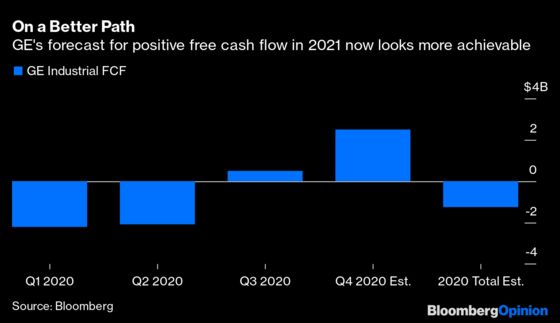

GE’s August decision to lower the bar for Culp felt like an admission that the company’s long-term prospects had dulled because of its near-term challenges. That's why it was so surprising when just one month later Culp told a Morgan Stanley conference that GE would generate positive free cash flow in the second half of 2020 — a prediction the CEO had been hesitant to make on the company’s earnings call in July despite repeated questions from analysts on this front. It was even more surprising when GE said in October that it had managed to generate positive free cash flow in the third quarter, compared with the average analyst expectation that it would burn through nearly $1 billion. The company has forecast “at least” $2.5 billion in cash flow for the fourth quarter and a positive number in 2021.

Why again did Culp need a lower bar? After bouncing around the $6 to $7 range for several months, GE’s rally took off in late September. With a week and a half left in 2020, GE shares are down only about 5% in a year that’s brought incredible disruption not just to the company but the world. It’s a serious feat, and there's no denying that Culp’s progress has been impressive. Through a combination of asset sales, cost cuts and internal overhauls, GE is a healthier and more transparent company than it was when he started. But while many (including me) have had their doubts at times, Culp has always been one of GE’s most prominent believers. It’s curious that this optimism didn’t extend into negotiations around his pay package.

To get the full $230 million, Culp has to push GE’s stock price to around $17, down from an initial goal of about $31. Again, this is a significant jump — but he’s still got until 2025, and if the recent trajectory of the company’s cash flow reboot is anything to go by, that feels doable. Meanwhile, back in the present, the company has eliminated 13,000 jobs in its aviation unit to adjust for the drop in demand amid the pandemic, and division chief John Slattery warned last month that more cuts are coming. Culp has indicated the bulk of these job reductions will be permanent, leading to a leaner and more profitable aviation division once travel recovers but an uncertain future for many former employees. Certainly less certain than Culp’s own future.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2020 Bloomberg L.P.