Will GE's Board Think Twice Next Time on $230 Million CEO Pay?

(Bloomberg Opinion) -- General Electric Co. investors love Chief Executive Officer Larry Culp. But they love themselves even more.

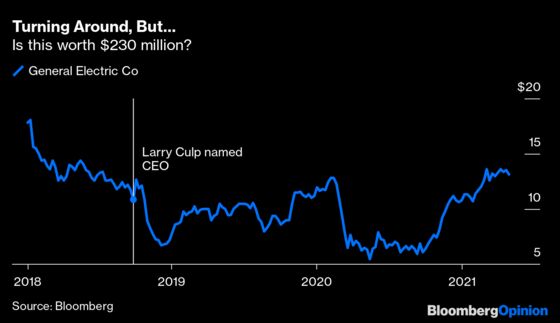

At the industrial conglomerate’s annual meeting on Tuesday, about 58% of voting shares opposed GE’s executive compensation arrangements. The vote was a striking — if ultimately just symbolic — protest against the board’s decision last year to recalibrate a one-time equity grant promised to Culp at his 2018 hiring to make it easier for him to access the full $230 million award. At the time, GE shares were drifting around $6 as investors fretted that the pandemic effects would derail a turnaround plan that had just started to bear fruit. So the board of directors decided that Culp only had to get the stock back into the $17 range to qualify for the top tier of the bonus, compared with $31 previously. If he could get the stock to around $13, he would get $124 million. A $10 range earned him $47 million.

There were a few problems with that. Because the rejiggered pay package also encompassed a contract extension, it gave Culp more time (up to five years) to hit the new lower target. In the month before GE announced that Culp was becoming CEO, shares of the company averaged about $12. That meant he could be handsomely rewarded even if the ultimate effect of his six-year-plus tenure was a lower stock price than the one he inherited, or one that was only modestly improved. No one would deny that the pandemic was disruptive and unprecedented, but for that kind of outcome, one would have to assume that the global economy was going to be dragging for a very long time. Or that GE would somehow be left out of any broader recovery.

Shareholders have a lot of reasons to cheer Culp. He has made significant strides in cleaning up the balance sheet and instilling more operational rigor in businesses that had lost their way. He’s also made incremental but steady improvements to the company’s legacy of confusing and labyrinthine financials. GE itself realizes its choice in CEO has a lot to do with the current share price. “Securing Larry’s continued leadership was one of the most important steps that we could take during a period of great uncertainty,” the company said in explanation of the bonus. But GE also has a long history of paying executives dizzying sums even as its shareholders lose money, and that practice has persisted in the Culp era. It seems investors’ patience with the practice — even if the recipient is GE’s purported savior — has finally grown thin.

It doesn’t help that GE has never been able to offer up a reasonable explanation for why such a lower bar on the pay deal was necessary. Thanks to the interventions of the Federal Reserve and the U.S. government as well as the miracles of modern vaccine science, the stock market has already bounced back. And so has GE. The stock has averaged about $13.28 over the last month, putting Culp well on his way to locking in the second $124 million tier of the bonus a mere nine months after the board changed the terms of the deal. Under the initial arrangement, at these prices, he would not have locked up any portion of the payout yet. The Covid recovery may have been difficult to foresee in August, when the new terms were announced, but this is evidence enough that the new stock-price milestones were nowhere near ambitious enough for a five-year time horizon.

The shareholder rebuke of Culp’s pay package is a win for champions of good governance. It’s ultimately nonbinding and it’s highly unlikely that GE would rejigger Culp’s compensation at this point — not least of all because he is successfully steering the company through a turnaround. But maybe, just maybe, when the next compensation decision comes along, the board will think twice.

Apart from Culp’s pay package, GE also paid former Vice Chairman John Rice a $2 million salary to come out ofretirement and work a part-time job.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2021 Bloomberg L.P.