GAM Turns a Corner. But Will It Head off the Public Highway?

(Bloomberg Opinion) -- Beleaguered Swiss fund manager GAM Holding AG finally has some good news to report that should allow it to draw a line under a terrible year. That could be the catalyst for a buyer deciding the brand is salvageable – while there’s still enough of the business left to buy.

On Tuesday, GAM said it had reached a truce with Tim Haywood, the star fund manager it suspended a year ago and subsequently accused of gross misconduct. Each has agreed that “neither party will pursue the other,” with the caveat that the truce is “based on current facts.” Even though Haywood countered by saying he dropped his suit for unfair dismissal because the cost of pursuing it would outstrip any damages, the accord should remove the threat of future litigation and any dirty linen being aired in a courtroom.

Customers who were trapped in Haywood’s Absolute Return Bond Funds when GAM froze them a year ago are receiving the last of their money back. On average, they will get 100.5% of the net asset value of their holdings compared with their valuation when GAM halted withdrawals and began liquidating the fund. That should deter the regulators, who have been silent on the matter, from punishing the firm for any lack of oversight. Apart from the eight-month delay between a whistle-blower informing on Haywood and his suspension, GAM appears to have done all it could to safeguard the money entrusted to it.

Finally, the eight-month search for a new permanent leader is over with the appointment of BlackRock Inc. veteran Peter Sanderson as chief executive officer. He will start in September, with interim CEO David Jacob taking the role of chairman a month later.

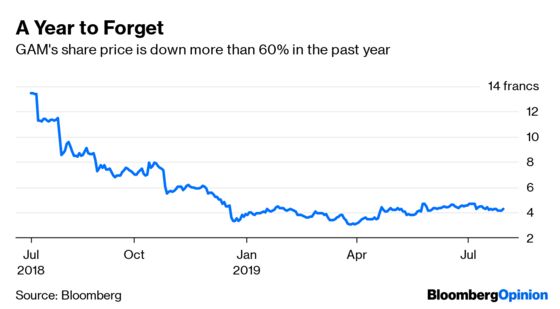

So that’s the good news. The bad news is that the business is still in intensive care after a disastrous year. Tuesday’s bump in the share price still leaves it down more than 60% in the past year.

Profitability is as underwhelming, with underlying pretax income dropping to 2.1 million Swiss francs ($2.1 million) in the first half of 2019 from 91.3 million francs in the first six months of last year.

Net outflows of 7.6 billion francs in the first half overshadowed 3.6 billion francs of market gains, cutting the assets overseen by the investment management division to 52.1 billion francs from 56.1 billion francs at the end of last year. That in turn trashed net fee and commission income, which dwindled to 171.1 million francs from 287.7 million francs in the year-earlier period.

To be fair, GAM isn’t alone in struggling to hang on to cash. Jupiter Fund Management Plc announced its sixth consecutive quarter of net outflows on Tuesday, while Man Group Plc saw customers pulling money out in the first three months of the year.

But the Swiss firm reckons it saw an “improving flow trend” in June and July with net inflows. That should give shareholders some hope that the worst is now behind it. Moreover, GAM has managed to defend its management fee margin, keeping it almost unchanged from December at just below 54 basis points.

In the absence of a buyer, the new CEO is left with the same to-do list facing the head of every other medium-sized asset manager: Cutting costs where possible, trying to halt the erosion in fees, and praying that the market environment remains friendly enough to bolster performance and bring in performance fees and client cash.

But as I suggested earlier this month, GAM’s best future may lie in finding a private equity buyer to take it off the market and let it rehabilitate its credibility with customers away from the glare of quarterly public reporting. Sanderson may have other plans; but unless he can do more for the stock price than Tuesday’s pop of about 4% by late morning, shareholders may be better served by him dressing up the company for a sale.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.