Big Oil’s Next Merger Mania Has an Eye on Its Demise

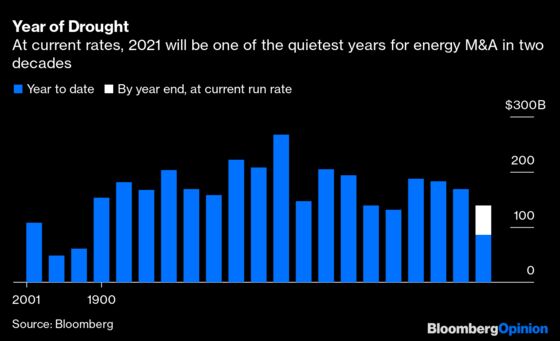

(Bloomberg Opinion) -- Is a barren year for oil industry deal activity finally coming to an end?

So far there’s been $86 billion of takeovers announced, pending or completed, according to data compiled by Bloomberg. If things continue at those rates through December, it will be one of the most lackluster years for energy deal-making in two decades.

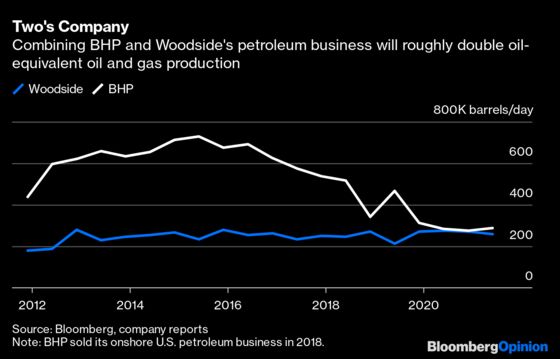

Hope is on the horizon. Saudi Arabian Oil Co. is finally growing close to an equity swap with Reliance Industries Ltd. after years of gestation, people with knowledge of the matter told Bloomberg this week. Meanwhile, BHP Group announced plans Tuesday to merge its oil and gas business with Woodside Petroleum Ltd. in a share-based deal that would see the mining company quit the petroleum sector and roughly double Woodside’s output. With the first valued at an estimated $20 billion to $25 billion and the latter worth about $15 billion at Woodside’s current share price, that would instantly increase the year’s tally by almost half.

Don’t take that for a sign that animal spirits are picking up in the industry. Although crude prices touched a three-year high last month and cash is once again flowing freely, this wave of deal activity doesn’t suggest an industry gearing up for a rally in demand.

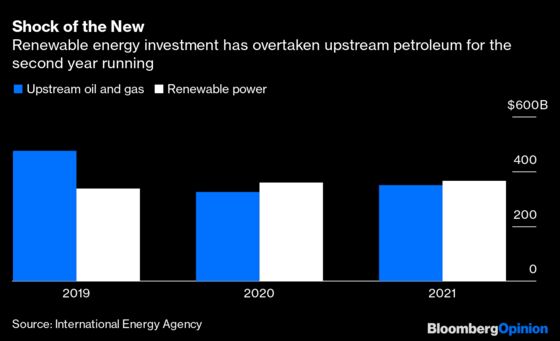

With the Intergovernmental Panel on Climate Change last week saying global warming is advancing faster than previously expected — likely exceeding the threshold of 2°C during the 21st century without deep emissions cuts — and the International Energy Agency forecasting that renewable power investment will exceed that in oil and gas production for the second year running, this merger boom has a distinctly end-of-an-era feel about it.

Take the Reliance-Aramco deal, which is expected to see the world’s largest oil company swap between 1% and 2% of its equity for a 20% share in the largest refinery. This is hardly the sort of transaction that Saudi Arabia might have made in the past, when it was able to reach into its bottomless cash pile to buy assets at a keen price from needy, low-margin refiners. Instead, Asia’s richest man, Mukesh Ambani, holds all the cards.

The estimated deal value would be double the $10 billion that Reliance reportedly expected for a 25% stake when it was first being offered around in 2019, although the balance-sheet value of the Jamnagar refinery and its earnings haven’t really improved since then. Meanwhile, a Saudi Inc. that was once so cash-rich that it thought little of splashing greenbacks on soccer teams and Leonardo da Vinci paintings is instead having to part with equity so precious that it wasn’t even offered to the kingdom’s own subjects until two years ago.

As a financial transaction, the deal does little for either party. Shares in Indian and Saudi companies aren’t much use as an alternative form of cash, since they’re locked up on illiquid local exchanges. Strategically, though, Aramco gets itself a seat at the table of a company that’s made no secret of its planned turn away from petroleum and toward renewables and a fast-growing telecoms unit. Jamnagar isn’t going to stop buying crude any time soon, but Aramco’s enthusiasm for a tie-up at any price suggests it’s keen to keep an eye on the situation before it starts to cause problems.

The BHP-Woodside deal isn’t happening on quite such a grand scale. While a combined company would have produced about 649,000 oil-equivalent barrels a day in 2019 — enough to put it in the top 30 listed oil producers by volume — Aramco pumps about that amount every hour.

It makes a different sort of sense for the players, though. Every company with assets less spectacular and owners less involved than Aramco has to care about the views of its shareholders and lenders. For BHP, that’s become a problem as the cost of capital for fossil fuel businesses rises and shareholders look to decarbonize their portfolios.

Arch-rival Rio Tinto Group quit its last fossil-fuel assets several years ago and Anglo American Plc sold out of its last thermal coal business in June. While the coking coal used in steelmaking is still a core business for BHP (not to mention iron ore, which can’t be turned into steel using existing commercial technology unless some coal-derived coke is thrown into the mix), selling out of a petroleum business that was always an odd fit for a mining company is a good way to project a cleaner image.

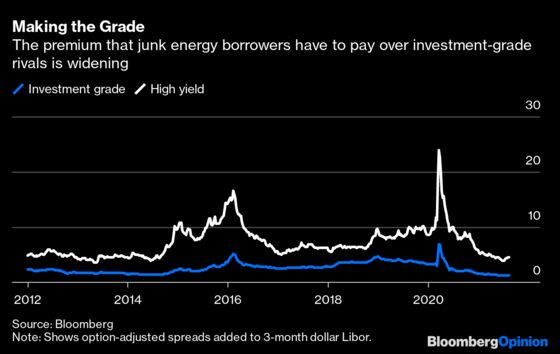

Woodside gets a different sort of benefit. At present it sits toward the lower end of investment grade at major ratings companies, an uncomfortable position at a time when the interest costs on junk energy debt are at a higher premium relative to higher quality bonds than they’ve been in years. By roughly doubling in size, it will get the cashflows and balance sheet to become more self-sufficient in its spending, an important consideration in a market where lenders are increasingly being asked to scrutinize the climate impact of their loan books.

For energy dealmakers looking to expand the fee pool, the signs of green shoots in the energy M&A market will be welcome after a year of drought. Just don’t mistake it for the start of a harvest. With its best years in the past, this field is looking more and more barren.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.